During the Year to date period in 2019, the ASX 200 index has risen 16.78%, according to trading on a contract for difference (CFD). CFD tracks the benchmark index from Australia. The Australiaâs S&P/ASX 200 Stock Market Index had reached an all-time high of 6875.50 in July 2019.

On 8 August 2019, the Australian benchmark S&P/ASX200 was trading at 6543.8, up by 24.3 points (at AEST 2:19 PM)

Macquarie Group Ltd

Profit to slightly fall in fiscal 2020

Macquarie Group Ltd (ASX: MQG) has given a negative return of 1.76% in one year as on August 7th, 2019.

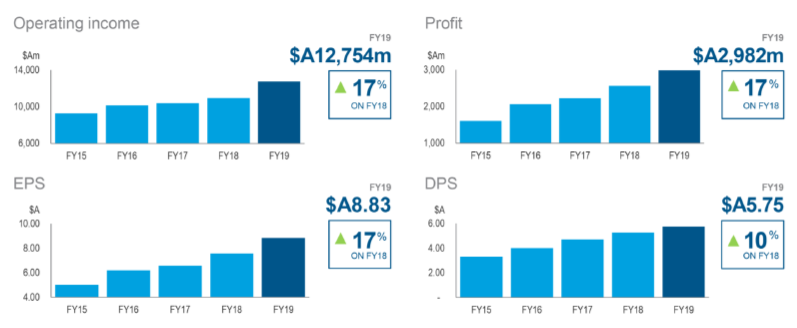

As reported on 25 July 2019, for the first quarter of fiscal 2020 period, MQG has delivered the operating profit broadly in line with the first quarter of 2019 but is slightly lower than the operating profit of fourth quarter 2019. Further, compared to the prior corresponding period, MQGâs annuity-style businesses declined, Macquarie Asset Management (MAM) also declined on the back of the timing of performance fees and higher operating expenses after the acquisitions of recent platform, Corporate and Asset Finance (CAF) declined on the back of the reduced loan volumes and realisations in CAF Principal Finance and the companyâs Banking and Financial Services (BFS) was mostly in line. The company currently expects its profit to slightly fall in fiscal 2020 compared to FY 19.

As per the market reports, MQG is expected to deliver earnings of A$2.96 billion for fiscal 2020. The company had reported the earnings of A$2.98 billion in FY 19.

FY 19 Financial Performance (source: Companyâs Report)

FY 19 Financial Performance (source: Companyâs Report)

Meanwhile, MQGâs stock was trading at A$122.140, up by 1.201 percent (on 8 August 2019, at AEST 2:48 PM) with a P/E ratio of 13.660x.

Whitehaven Coal Ltd

Price of Coal subdued in the June 2019 Quarter

Whitehaven Coal Ltd (ASX: WHC) stock has provided with negative return of 34.56% in last one year period as on August 7th, 2019.

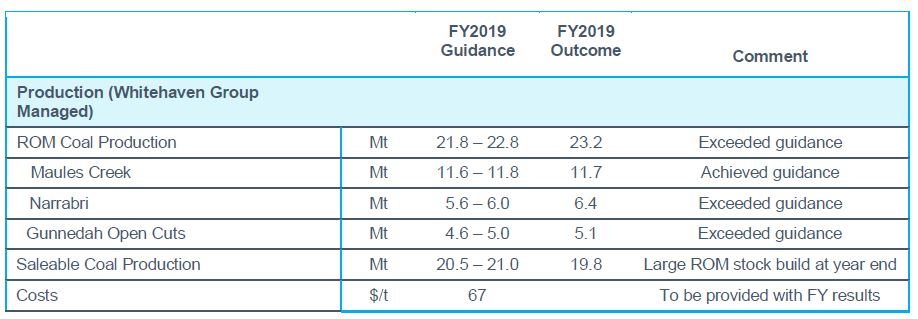

As reported on 11 July 2019, in the WHCâs June Quarter Production Report, there was a decline in the globalCoal Newcastle Index (gC Newc) thermal coal price in the June 2019 quarter at an average of US$79.86/t compared with the average price for FY19 of US$99.41/t.

WHC had achieved the thermal coal sales price of US$84/t, which is 5% more than the average gC Newc price for the quarter. However, the benchmark price of prime hard coking coal was of US$208/t and for SSCC it was US$129/t and for Low Vol PCI coal it was approximately US$141/t in the June 2019 quarter. WHC had achieved the average price of US$107/t for its metallurgical coal sales (SSCC and PCI coal) in the June quarter. Further, for the June 2019 quarter, there was 25% increase in the production of ROM coal to 7.3Mt, 9% increase in the saleable coal production of 5.2Mt and 12% rise in the coal sales (including purchased coal) to 5.3Mt compared to the previous corresponding period (pcp). For full year 2019, the production of ROM coal was of 23.2Mt, which has exceeded the companyâs guidance for full year.

Meanwhile, on 8 August 2019, WHCâs stock was trading at A$3.46, up by 3.284 percent (at AEST 2:48 PM), with a P/E ratio of 5.770x.

FY 19 Production Guidance Commentary (Source: Companyâs Report)

FY 19 Production Guidance Commentary (Source: Companyâs Report)

Reliance Worldwide Corporation Ltd

Lowered the FY 19 EBITDA Guidance

Reliance Worldwide Corporation Ltd (ASX:RWC) stock has fallen 46.05% in one year as on August 8th, 2019.

As per the release, on 13 May 2019, the company revised FY19 EBITDA guidance downwards. The company now expects 2019 EBITDA to be in the range of $260 million to $270 million, which is lower than the previous 2019 EBITDA guidance range expected to be $280 million to $290 million. This is on back of complete absence of modest freeze event, which has led to decline in net sales in the range of $12 million to $15 million in FY19. The Company had previously projected that the absence of a modest freeze event could impact FY19 EBITDA in the range of 1.5% to 3.0%.

On 8 August 2019, RWCâs stock was trading at A$3.2, down by 0.312 percent (at AEST 3:05 PM), with a P/E ratio of 25.28x.

CYBG PLC

Lowered FY19 NIM Guidance

CYBG PLC (ASX: CYB) stock has given a negative return of 55.52% in one year period, as on August 7th, 2019.

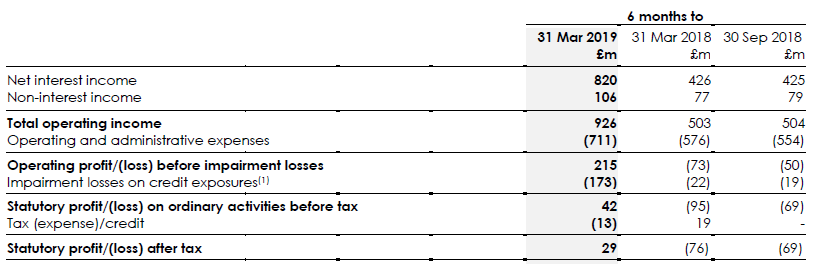

On 30 July 2019, updated on the third quarter of FY19 period, wherein CYB for FY 19 expects NIM to be at the lower end of its 165-170bps guidance range on the back of tough competition in mortgage lending and the pressure of Brexit.

CYB has confirmed that it is performing in line with the companyâs expectations and continues to make good progress continues to be make with the Virgin Money integration programme. Meanwhile CYB has secured all the regulatory approvals, the Investments & Pensions JV with Aberdeen Standard Investments was anticipated to be completed on 31 July 2019.

On the outlook front, in the fourth quarter 2019, CYB will book the gain on sale of c.£35m after selling of c.50% of its interest in Virgin Money Unit Trust Managers Limited. The company is progressing well with c.£45m of annual run-rate cost synergies and is on track for FSMA Part VII completion in October. Moreover, the companyâs CET1 ratio has expanded slightly to 14.6% at 30 June 2019.

On 15 May 2019, the company for the first half of 2019 for the period ended 31 March 2019, has reported 5% fall in the pro forma underlying profit before tax to £286m driven by rise in the impairments. However, it rose by 2% from the second half of 2018. The company for 1H 2019 period has delivered total underlying income of £843m, which is in line with both H1 18 and H2 18. During 1H 2019, there has been 1% fall in the net interest income to H1 18.

1H FY 19 Financial Performance (Source: Companyâs Report)

1H FY 19 Financial Performance (Source: Companyâs Report)

On 8 August 2019, CYBâs stock was trading at A$2.76, up by 0.73 percent (at AEST 3:26 PM).

Sims Metal Management Ltd

Strategic Goals

Sims Metal Management Ltd (ASX:SGM), is a leading company in the recycling business,. The companyâs stock has given a negative return of 43.27 percent in the last year duration.

On 9 April 2019, the company updated the market on the plans to double the recycling of non-ferrous metal business and to expand the ferrous metal recycling business by 40% in the United States in next six years. The company intends to expand e-recycling services and to become the leader in the e-recycler of data storage centers (the cloud). For this the company has set the target to recycle 10% of the cloud over the next six years. SGM intends to be the original equipment manufacturer supplier of choice for recycled plastic. SGM by 2025, plans to get additional large city municipal recycling contracts. Moreover, the company plans to generate electricity through the non-metallic residue. SGM has plans the acquisition of or building of a minimum of 50 Megawatts of sites in the next six years.

On 8 August 2019, SGMâs stock was trading at A$9.6, up by 0.84 percent (at AEST 3:37 PM), with a P/E ratio of 10.240x.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.