The S&P/ASX 200 Index settled in the green zone on 27 August 2019 after moving upward by 0.48% to settle at 6,471.2. The following ASX-listed companies from the communication services sector have reported financial results for the year ended 30 June 2019. Letâs take a glance at how these companies performed during the year.

Amaysim Australia Limited

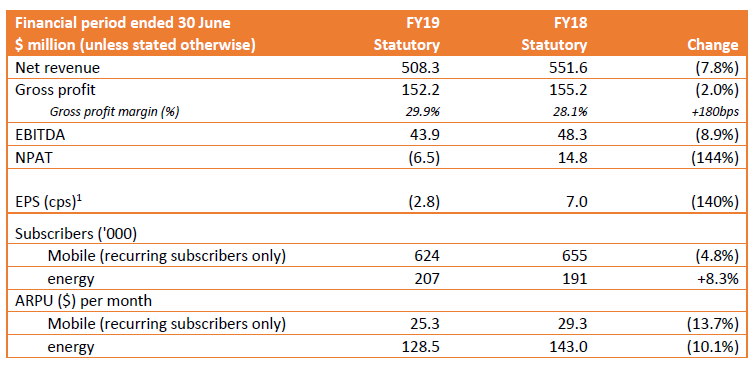

Amaysim Australia Limited (ASX:AYS), an Australia-based provider of mobile services, reported a net loss after tax (continuing operations) of $ 6.53 million in FY19 ended 30 June 2019, while reporting a 7.8% decline in statutory net revenue to $ 508.3 million in the financial year 2019. The companyâs performance during the period was impacted by a challenging environment in the energy market and a cutthroat competition in the mobile market.

FY19 Financial Performance (Source: Company Reports)

On a comparable basis, the company posted a 15.8% fall in mobile net revenue to $ 203.4 million in FY19. Its mobile revenue got affected on the back of a fall in the number of subscribers and lower ARPU that got impacted due to competition and lower value plans. On a comparable basis, the company posted a 1.7% fall in energy net revenue to $ 304.84 million in FY19, even though the companyâs subscribers increased. The decline in the energy top line was driven by lower ARPU, on the back of low consumption across the market.

Further, on a comparable basis, the company witnessed a 33.3% decline in underlying EBITDA to $ 36.1 million in FY19. There has been a 56.5% fall in the mobile underlying EBITDA to $ 13.6 million and a fall of 1.7% in energy underlying EBITDA to $ 22.5 million in the reported year. On a comparable basis, gross profit of the company remained stable at $153.7 million in FY19 compared to $ 155.2 million in the same period a year ago, while gross margin expanded by 194 basis points to 30.1%, on the back of strong margins in the energy segment and also due to the strength of the companyâs mobile wholesale agreement. AYS registered a 16.2% rise in energy gross profit to 85.4m due to disciplined management of margin. However, on a comparable basis, there has been a 16.4% decline in mobile gross profit to $ 68.3 million in FY19, though the segmentâs gross margin remained strong at 33.6%.

Overall at the end of FY19, the companyâs cash and cash equivalents increased by $ 20.9 million to $ 30.7 million due to the increase in funds after a capital raise of $ 50.6 million in the month of February 2019.

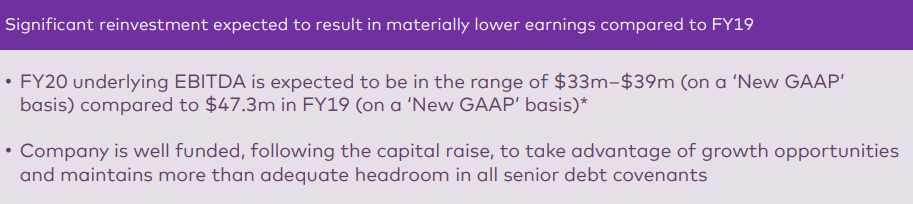

FY2020 Outlook:

Amaysim Australia is hopeful for medium to long term outlook, despite the challenges in mobile and energy. Meanwhile, for fiscal 2020, the company expects underlying EBITDA to fall versus FY19 and is projected to be in the range of $ 33 million to $ 39 million compared to $ 47.3 million in FY19 (on a New GAAP basis). The company anticipates that unprecedented changes in the regulations in the energy sector would put pressure on the retail energy margins. It is expected that lower energy consumption would continue. The energy segment earnings for fiscal 2020 would be impacted.

FY20 Guidance (Companyâs Report)

Stock Performance:

With a market cap of approximately $ 151.98 million and nearly 295.11 million outstanding shares, the stock of AYS closed the dayâs trading at $ 0.465 on 27 August 2019, down 9.709% from its previous close. The stock has given negative returns of 25.26% and 37.20% in the last three months and six months, respectively.

Vocus Group Limited

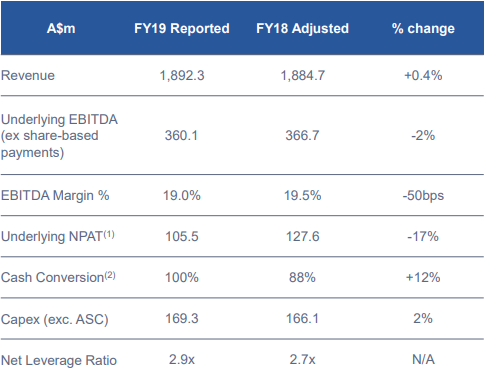

Victoria-based vertically integrated telecommunications provider, Vocus Group Limited (ASX:VOC) released its full-year results for FY19 on 22 August 2019, reporting a 17% fall in underlying NPAT to $ 105.5 million. Meanwhile, the company posted a 2% decline in underlying EBITDA (excluding share-based payments) to $ 360.1 million for FY19, on the back of VNS growth at lower margin driven by one off project revenue and wholesale NBN.

In FY19, the company reported a 0.4% rise in statutory revenue, driven by growth in Vocus Networks Services and New Zealand, which has offset the fall in retail. Strong reduction in cost in the retail segment had improved EBITDA margin, although the revenue declined. The company has been investing in people and capability. In FY19, the company reported a 0.4% rise in statutory revenue, driven by growth in Vocus Networks Services and New Zealand, which has offset the fall in retail. In FY19, recurring revenue grew 5% year-on-year, backed by growth in NBN revenue as well as its data networks segment.

Group Financial Summary (Source: Companyâs Report)

FY20 Guidance:

Additionally, Vocus has reaffirmed the guidance for the fiscal year 2020. For fiscal 2020, the company expects underlying EBITDA to be in the range of $ 359 million - $ 379 million compared to the previous expectation of underlying EBITDA to be in the range of $ 350 million to $ 370 million. The EBITDA of Vocus Network Services is expected to grow in the range of $ 20 million to $ 30 million in FY20 which would offset the decline in retail. For fiscal 2020, the capex is expected to be in the range of $ 200 million - $ 210 million and cash conversion to be between 90% and 95%

Stock Performance:

With a market cap of approximately $ 1.99 billion and nearly 622.26 million outstanding shares, the stock of VOC closed the dayâs trading at $ 3.180 on 27 August 2019, down 0.313% from its previous close. The stock has given negative returns of 29.89% and 9.12% in the last three months and six months, respectively.

Telstra Corporation Limited

Telstra Corporation Limited (ASX: TLS), a communication services sector player, on 16 August 2019 announced that the companyâs total value of assets monetised as part of T22 stands at approximately $ 1 billion, on the back of recent changes to Telstra Ventures, sale of the Edison Exchange building in Brisbane, and other smaller transactions and the agreement signed for part sale of an unlisted property trust for owning 37 of Telstraâs existing exchange properties. The company has a goal of monetising up to $2 billion of assets by the end of fiscal 2020 for strengthening the balance sheet.

Meanwhile, TLS announced in a release of full-year results on 15 August 2019 that since FY16, the company has reached a cost reduction of $ 1.17 billion and expects to achieve the net cost reduction target of $ 2.5 billion by FY22.

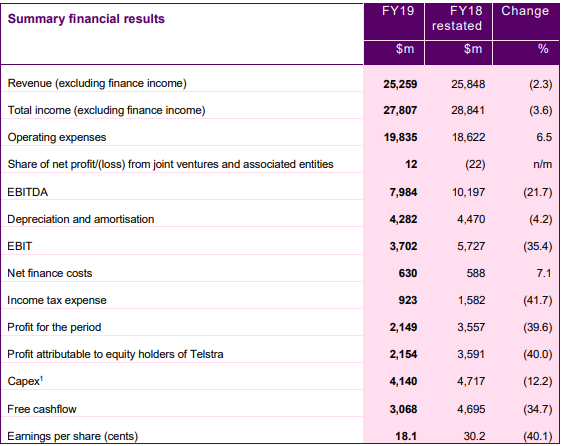

Moreover, for FY19, on a reported basis, there was a 3.6% fall in total income to $ 27.8 billion, 21.7% decrease in EBITDA to $ 8 billion and a 39.6% decline in NPAT to $ 2.1 billion. On a guidance basis, for FY19, the company posted a 2.6% fall in total income to $ 27.8 billion and an 11.4% fall in EBITDA (excluding restructuring costs) to $ 9.4 billion. During FY19, the company reported an 11.2% fall in underlying EBITDA to $ 7.8 billion.

Source: Companyâs Report

FY20 Guidance:

Additionally, for fiscal 2020, the company expects total income to be in the range of $ 25.7 billion to $27.7 billion, underlying EBITDA is expected to be in the range of $ 7.3 billion to $7.8 billion, restructuring costs to be of approximately $ 300 million, and capital expenditure to be in the range of $ 2.9 billion to $3.3 billion. Moreover, free cash flow after operating lease payments is expected to be in the range of $ 3.4 billion to $3.9 billion. Telstra also anticipates fiscal 2020 to have the biggest in-year nbn headwind to date and the recurring impact of nbn is expected to be between $ 800 million and $ 1 billion. The fiscal 2020 underlying EBITDA of the company is projected to grow by up to $ 500 million (excluding the recurring in-year headwind of the nbn).

Stock Performance:

With a market cap of approximately $ 44.01 billion and nearly 11.89 billion outstanding shares, the stock of TLS closed the dayâs trading at $ 3.740 on 27 August 2019, up 1.081% from its previous close. The stock has given positive returns of 4.82% and 17.83% in the last three months and six months, respectively.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.