The materials sector is vital to an economy’s overall growth as they supply the constituents that build the economy. In the contemporary world, the materials sector is not merely limited to supplying raw materials for construction purposes but encompasses a wide range of commodity-related manufacturing industries. These include chemicals, glass, paper, forest and linked packaging goods along with minerals, metals and mining firms.

The Australian materials sector is world-class and is subject to constant development and innovation. They garner the attention of both businesses and investors domestically as well as globally.

Talking about the stance of the materials sector as an investment option, industry experts opine that the sector has rallied fiercely since the second half of 2019, partly due to improvement in the Australian housing down turn, a bright outlook for the residential property along with positive momentum in US housing and market share gains.

Consequently, valuations remain relatively attractive, with the average forward PE being much better than the industry average.

In this backdrop, we have cherry-picked three ASX-listed materials companies that have been making headlines with their latest results that have been reported in this earnings season-

Amcor Plc (ASX:AMC)- Good 1H Results, Improved Outlook for FY20

The global leader in consumer packaging, Amcor leverages from powerful competitive advantages- differentiated commercial and innovation capabilities, unparalleled scale and a global footprint. This positions the Company uniquely to serve customers and develop sustainable and economically viable packaging solutions.

In January 2018, AMC vouched to develop its entire packaging as recyclable/ reusable by 2025.

The Company recently reported its results for the six months ended 31 December 2019, with the below highlights-

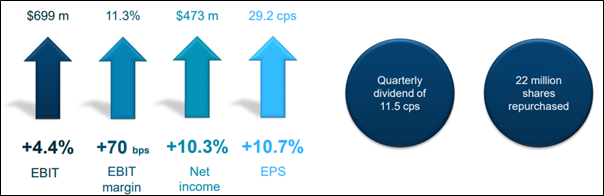

- GAAP net income of USD 252 million and EPS (diluted US cents) of 15.5 cps

- Quarterly dividend of 11.5 cps declared, to be paid on 24 March 2020

- Total cash returns to shareholders of over USD 600 million, including the repurchase of 21.9 million shares

- The integration of the Bemis business is progressing well, with ~ USD 30 million of pre-tax synergy benefits delivered in the 1H FY20

1H adjusted financial results (Source: AMC’s Report)

AMC also intimated about its outlook for FY20, wherein the outlook for adjusted EPS growth in constant currency terms has improved to 7-10% (which was previously 5-10%)-

- Bemis business integration related pre-tax synergy benefits have increased to $80 million for FY20. The Company remains on track to deliver $180 million of total pre-tax synergy benefits over three years

- The USD 500 million buy-back program likely to be completed by FY20

- Constant currency EPS range of 62 – 64 US cps

- AMC expects over USD 1 billion of annual free cash flow before ~ USD 100 million of cash integration costs

- Corporate expenses before synergies likely to be USD 160 – USD 170 million in constant currency terms

- Net interest costs of USD 210 – USD 230 million in constant currency terms

- Adjusted effective tax rate of 21% - 23%.

Orora Limited (ASX:ORA)- Challenging 1H Results, Tough Outlook

Offering its customers with an extensive range of tailored packaging solutions and displays, ORA has its presence in 7 countries. The Company reported its challenging first half result, driven primarily by the subdued economic conditions across geographies that impacted earnings.

Even the positive first half in North America and Australasia demonstrated lower earnings relative to the previous corresponding period (pcp), driven by the persistent tough trading conditions. Below are a few highlights from the results report-

- Statutory NPAT was $76.6 million, down by 13.3% compared to pcp

- Statutory EPS was 6.4 cps, down 11.1% on pcp

- Sales revenue amounted to $1,835.2 million, up by 13.3% on pcp

- EBIT was $133.1 million, down 4.1% on pcp

- The return on average funds employed was 19.2%, down from 21.9% at pcp

- Net debt was $996 million (at 31 December), up from $872 million at pcp

- The Company declared Interim ordinary dividend of 6.5 cps (30% franked and 70% sourced from the conduit foreign income account), to be paid on 9 April 2020

1H20 Financial Summary (Source: ORA’s Report)

ORA also disclosed its outlook, which were consistent with the previously announced one (October 2019). The Company still expects difficult market conditions to continue for the rest of FY20. Moreover, the financial impact of the G2 rebuild in the second half along with the time for the North American improvement initiatives to be fully realised might result in a lower operating EBIT for the continuing operations in FY20.

However, the Company remains committed to invest in efficiency, growth and innovation, while it assimilates its recent acquisitions (Texas based Pollock acquisition) and finalises the sale of the Fibre business.

Besides the business results, ORA also announced that its Chairman, Mr Chris Roberts will retire from the Board, and Mr Rob Sindel will succeed him, effective 12 February 2020. Mr John Pizzey, a Director from its Board will retire, effective 31 May 2020.

James Hardie Industries Plc (ASX:JHX)- Third Consecutive Quarter of Strong Results

A world leader in the manufacture of fiber cement siding and backerboard, James Hardie caught the investors eye as soon as its securities were placed in a trading halt on 11 February 2020, pending the release of its announcement regarding its earnings.

The Company soon after declared the results for the third quarter of FY20 and the nine months period ended 31 December 2019, registering the third consecutive quarter of strong financial results and continued profitable growth momentum. This demonstrates that JHX’s teams, across the globe, are well executing its strategic plan, which is also reflected in its results. Some of the highlights from the same are as follows:

- Group adjusted NOPAT was USD 77.4 million for the quarter and USD 266.2 million for the nine months, both up by 17% on pcp

- Group Adjusted EBIT was USD 107.2 million for the quarter and USD 365.8 million for the nine months, up by 18% and 20% respectively, on pcp

- Group net sales of USD 616.7 million for the quarter and USD 1,933.6 million for the nine months, up by 5% and 3%, respectively, on pcp

- Comparable Adjusted net operating profit for FY19 was USD 300.5 million

Driven by the continued profitable growth momentum, JHX has raised its full year Adjusted NOPAT guidance range, to between USD 350 million and USD 370 million. Other aspects of JHX’s outlook, as per its highlights are as under-

- The analysts’ forecasts suggest that net operating profit (excl. asbestos) will be between USD 356 million and USD 380 million, for FY20

- Full year adjusted net operating profit will be between USD 350 million and USD 370 million

- The North America Fiber Cement segment EBIT margin will range between 25% and 27% for FY20

- New construction starts to be ~1.3 million in FY20

- Volume from Australian business will continue to grow above the market

- In Europe, the Company expects its addressable underlying market in FY20 to decrease slightly compared to FY19

- JHX will continue to invest in the long-term growth with a focus on delivering more value to customers via improved demand creation, stable product quality, timely delivery, and customer-driven innovations

Stock Performance

Let us look at the stock performance of the discussed stocks after the close of the market on 12 February 2020-