Base metals prices took a jab as global economic conditions loomed over the United States stance to rely on the higher tariff. In a recent tweet, the United States President mentioned that the United States would impose a higher tariff to stabilise the domestic economic conditions.

The increased stance of the United States concerned the market participants over the global economic conditions, which in turn, exerted the pressure on base metal prices.

The falling dollar further contributed to the fall in base metal prices as metals are dollar-denominated in the international market. The Dollar Index, which tracks the dollar performance dropped from the level of 97.77 (Dayâs high on 18th June 2019) to the present low of 95.90 (as on 25th June 2019 2:03 PM).

Apart from the global cues and the depreciating dollar, the weak manufacturing indication in the United States exerted pressure on the base metal prices. As per the data, the Flash Manufacturing PMI released recently stood at 50.1 against the market expectation and previous level of 50.5. The decline in the manufacturing exerted pressure along with the factor mentioned above.

Though, the manufacturing PMI value remained above its mean value of 50, but the manufacturing index marked a third consecutive monthly drop. The Flash Manufacturing PMI which stood at 52.5 in March 2019 declined to the present level of 50.1.

LME Copper:

LME Price:

Copper Futures (CFD Derived) dropped from the level of US$6026.25 (Dayâs high on 20th June 2019) to the present low of US$5915.25 (Dayâs low on 24th June), which in turn, marked a decline of more than 1.84 per cent in two trading sessions.

The falling demand and growing inventory across the LME registered warehouses exerted pressure on copper prices. As per the data, the inventory stocks along the LME registered warehouses grew from the level of 187700 (as on 23rd May 2019) to the level of 246050 (as on 25th June), which in turn, marked a gain of more than 31 per cent in just 30-days.

The sharp increase in the inventory level exerted pressure on copper prices, and the prices dropped on the London Metal Exchange and in the international market as well.

On the demand front, the geopolitical tensions between the United States and Iran are creating a possibility of war, which, in turn, is generating pessimism among the global investors and exerting pressure on copper prices.

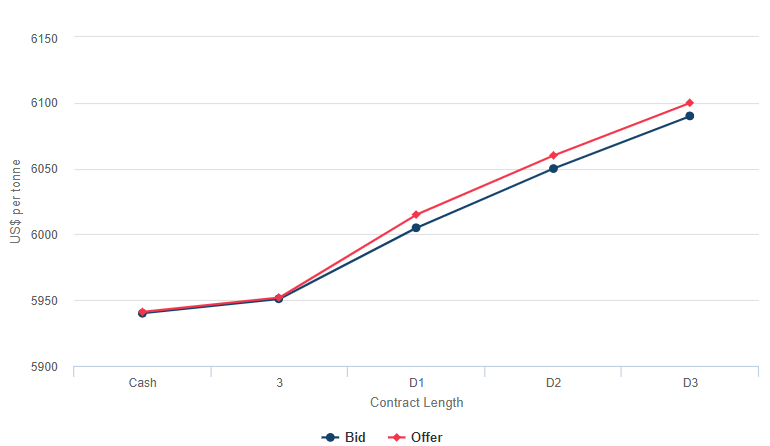

LME Forward Price:

Source : LME

Source : LME

On the forward curve, the copper prices are showing an upward curve for now, with a Bid-to-Ask Spread of US$10, which in turn, further suggests that the copper supply is still dominating the market.

Copper Production Trend :

The world Mine production of copper in February 2019 declined by more than 9 per cent as compared to the previous month, as suggested by the data from the International Copper Study Group. As per the data, the World Mine Production of copper in February 2019 stood at 1,515 thousand metric tonnes as compared to 1,672 thousand metric tonnes in January 2019.

The World Mine Capacity also declined from the level of 2,073K metric tonnes in January 2019 to 1,879K metric tonnes in February 2019.

The Mine Capacity Utilization rate also declined from 80.7 per cent in January 2019 to 80.6 per cent in February 2019. The overall world refined production stood at 1,832K metric tonnes in February 2019, down by more than 9 per cent, as compared to the world refined production of 2,021K metric tonnes in February 2019.

However, despite the overall decrease in production metrics, the world Refined Copper usage declined by more than 14 per cent in February 2019, and the world refined usage in February 2019 stood at 1,758K metric tonnes, down from the usage of 2,054K metric tonnes in January 2019.

The lower consumption indemnified the production decline, which in turn, increased the copper inventories across LME registered and non-registered warehouses.

LME Aluminium :

The Aluminium Futures (CFD Derived) rose despite the global uncertainties amid supply shortfall; the prices of Aluminium Futures surged from the level of US$1749.75 (Dayâs low on 21st June 2019) to the present high of US$1803.25 (as on 25th June 2019 2:10 PM AEST).

The Aluminium stockpiles across the LME registered warehouse noticed a steep decline in the last 30-days. As per the data, the LME registered warehouses marked a fall of aluminium from the level of 1222625 (as on 23rd May 2019) to the level of 1031626 (as on 24th June), which in turn, marks a drop of more than 15 per cent in 30-days.

Apart from the decline on the London Metal Exchange-registered warehouses, Aluminum inventory declined in China as well. As per the data, the social primary aluminium across eight significant consumption regions in China dropped by 20,000 metric tonnes to stand at 1.061 million metric tonnes on 24th June 2019 from 20th June 2019.

The decline in aluminium stockpiles is supporting the aluminium prices in the international market.

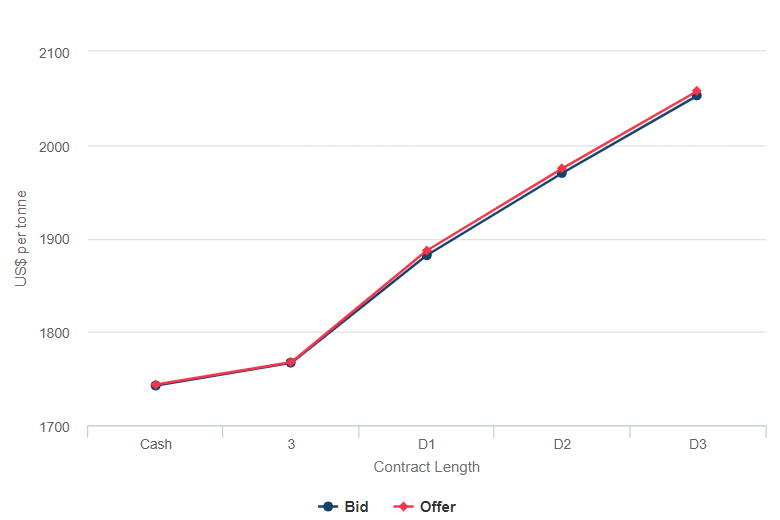

LME Forward Price:

Source : LME

Source : LME

The future closing price curve of aluminium on the London Metal Exchange is upward sloping with a very slight gap between the bid and the ask price, which in turn, signifies that the demand of the commodity is high.

Aluminum Demand Projections:

China is gradually shifting its automobile industry towards the light-weight materials to meet the stringent emission norms, which in turn, is expected (by the market participants) to support the Aluminium prices. As per the data, the automobile industry in China consumed 3.9 million tonnes of aluminium in 2017, up by 8 per cent as compared to the previous year and is further forecasted by many aluminium study groups to inch up over the long-term.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.