Options:

Options are derivatives and trading instruments for people who either hedge their investments or leverage their speculations. In Option trading, there is a wide range of strategies followed in different market scenarios with the limited/unlimited risk/reward potential.

Option Strategy in Bullish Markets:

Investors/traders follow bullish strategies such as Long Call, Bull Spread, protected covered write or collar, Ratio Call Spread, and Protected Put.

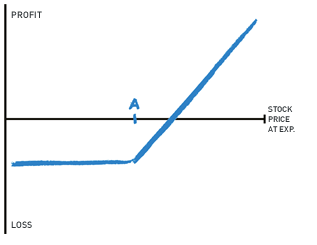

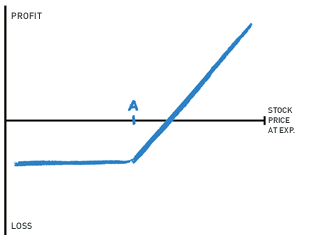

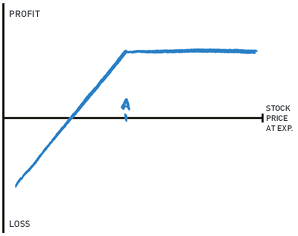

Long Call:

This strategy can be deployed when an investor expects market to move up. This is a single leg strategy which can provide leveraged exposure to the price rise.

Buy call of an underlying security at a strike price (ITM/OTM/ATM) based on the option price and risk appetite. One can exit the position based on risk to reward ratio or exercise the option on expiry. [ITM, OTM, and ATM denotes In-The-Money, Out-of-The-Money, and At-The-Money, respectively.]

Â

Â

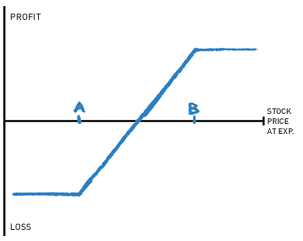

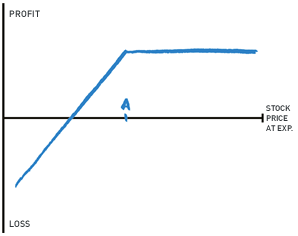

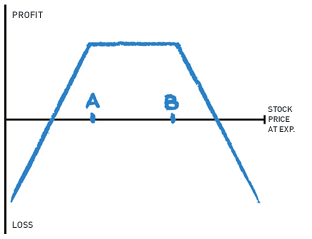

Bull Call Spread:

This strategy can be deployed when an investor is not so bullish about the market but expects moderate price rise. It is comparatively cheaper than single leg buy call.

Buy Call of lower strike price,and sell call of the higher strike price. Consider the strategy when you expect a limited rise in the price of the stock. At time of booking profit or loss, generally it is recommended to take off both the legs at the same time because one remaining sell option will be expose to unlimited risk and one remaining buy option will be exposed to theta decay but unlimited profit. This is only a guideline and trader can always make adjustments based on his capability. Before entering any trade, the trader should look at a good risk to reward ratio.

Â

Â

Protected covered write or collar:

This strategy can be used when share prices are expected to rise moderately. It eliminates the risk of a larger potential loss on stock.

Buy stock, short Call of high strike price, and buy Put of the small strike price. One must ensure that the premium received is adequate, given the possibility that the options will be exercised. This is fairly complex strategy as no. of equity shares has a lot of impact on the overall P&L of the strategy. No. of shares should be adequate enough so that it can withstand the loss of sell call in case ITM expiry but should also be less enough to take minimum loss on the downside. The recommended size should be equal to the lot size of the derivative.

| Maximum Profit at Expiry | Difference between stock price (Entry) and strike price of call, plus net premium received |

| Maximum Loss at Expiry | Difference between stock price (Entry) and strike price of put, less net premium received |

| Breakeven at expiry | Stock price (Entry) less net premium |

| Theta (Time decay) | Better at strike price of call |

| Vega (Volatility) | Steady |

Ratio call spread:

This is a right strategy for the investors who is expecting a slight rise in the market with little bullish biasness.

Buy a Call at the lower strike price, and short 2 Calls at the higher strike price (same strike).

This strategy works well when a small market movement is there on the upside. In case of a high price jump, an exit must be considered or adjustment to the strategy based on oneâs risk to reward ratio.

| Maximum Profit at Expiry | Difference between strike prices less cost of spread |

| Maximum Loss at Expiry | Unlimited on upside; cost of spread on downside |

| Breakeven at expiry | Higher strike price less maximum profit of spread; Higher strike price plus maximum profit of spread |

| Theta (Time decay) | Better at higher strike price |

| Vega (Volatility) | Steady |

Protected put:

This strategy can be deployed when an investor has bought a stock and expects market to enter bearish phase. Protected put counteracts any major loss from the stock price decline.

Buy a put to protect your stock from any temporary downfall expectations. One should use the hedge ratio to provide the required coverage to the stock position.

Â

Â

| Maximum Profit at Expiry | Unlimited |

| Maximum Loss at Expiry | Stock Price â Strike Price + Premium Paid |

| Breakeven at expiry | Stock Purchase Price + Premium Paid |

| Theta (Time decay) | Negative Impact |

| Vega (Volatility) | - |

Â

Option Strategy in Bearish Markets:

Investors/traders mainly follow bearish strategies such as Long Put and Bear Spread, among so many available bearish option strategies.

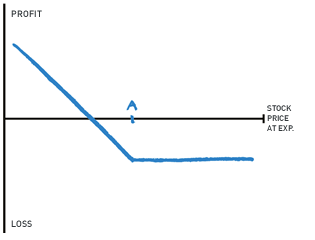

Long Put:

Deploy this strategy when market is expected to decline. This is a single leg strategy; hence maximum loss would be the premium paid.

Buy put of an underlying security at a strike price (ITM/OTM/ATM) based on the option price and risk appetite. One can exit the position based on risk to reward ratio or exercise the option on expiry.

Â

Â

| Maximum Profit at Expiry | Strike Price â Premium Paid |

| Maximum Loss at Expiry | Premium Paid |

| Breakeven at expiry | Strike Price â Premium Paid |

| Theta (Time decay) | Negative Impact |

| Vega (Volatility) | Increasing Vega has positive impact |

Â

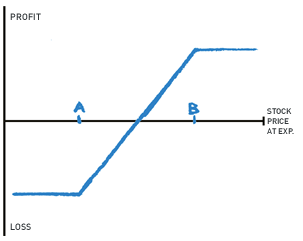

Bear Put Spread:

An investor uses this strategy when he/she expects a moderate fall in the market. This is a double leg strategy where risk and reward is already defined.

Buy Put of higher strike price, and Short Put of the lower strike price. Consider the strategy when you expect a limited fall in the price of the stock. In case stock price falls sharply, exit the strategy at the lower strike price. At time of booking profit or loss, generally it is recommended to take off both the legs at the same time because one remaining sell option will be expose to unlimited risk and one remaining buy option will be exposed to theta decay but unlimited profit. This is only a guideline and trader can always make adjustments based on his capability. Make sure that the potential reward justifies the cost of the spread.

| Maximum Profit at Expiry | Difference Between strikes less cost of spread |

| Maximum Loss at Expiry | Net premium paid |

| Breakeven at expiry | Upper strike less cost of spread |

| Theta (Time decay) | Better at lower strike price |

| Vega (Volatility) | Steady to increasing |

Â

Option Strategy in Neutral Markets:

Investors/traders follow neutral strategies such covered write, short put, short strangle, long butterfly and calendar spread. These strategies may harm the position adversely if the market moves significantly in one direction.

Covered Write:

An investor uses this strategy if he/she has bought a stock expects market to either remain flat or a moderate fall. On major fall, this strategy may lead to major loss.

Short Call and buy the stock. Deploy the strategy in case of neutral or slight dip expectation in the market. This strategy is also used to hedge the investments from slight downfall.

| Maximum Profit at Expiry | Time value of the option premium + Difference between strike price if option is Out-of-the-money when written |

| Maximum Loss at Expiry | Share price at the time of writing option less premium received |

| Breakeven at expiry | Upper strike less cost of spread |

| Theta (Time decay) | Helps |

| Vega (Volatility) | Steady to falling |

Â

Short put:

This strategy is used when market is expected to remain flat with mild bullishness. This is a single leg strategy, hence cost of acquisition (margin requirement) would be more. Short a Put option on expectation of steady market movement. Exit the position if the stock price falls sharply.

| Maximum Profit at Expiry | Premium received |

| Maximum Loss at Expiry | Strike price less premium received |

| Breakeven at expiry | Strike price less premium received |

| Theta (Time decay) | Helps |

| Vega (Volatility) | Falling |

Short Strangle:

This strategy is deployed when option premiums are overpriced, and investors expects stock to remain flat for some time. This strategy has lower potential of profits as compare to Short Straddle, but on comparison of risk adjusted return, this is considered a better strategy.

Short Call at the higher strike price, and Short Put at the lower strike price. Deploy the strategy in the steady market and for the near month to get the maximum benefit. Exit the position when there is any sharp market movement.

| Maximum Profit at Expiry | Premium received |

| Maximum Loss at Expiry | Unlimited |

| Breakeven at expiry | Higher Strike + Net Premium Received Lower Strike â Net Premium Received |

| Theta (Time decay) | Helps |

| Vega (Volatility) | Falling |

Â

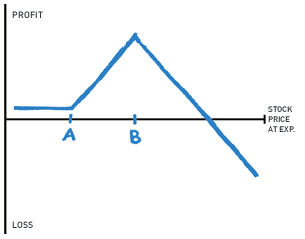

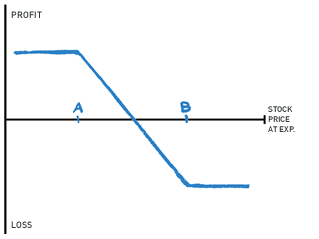

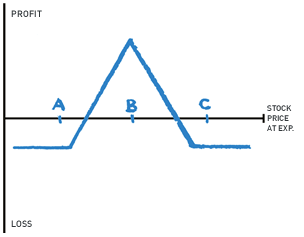

Long Butterfly:

This strategy is used by most of the investors/traders to get best possible reward over risk taken. Here both legs are protected, hence very limited risk even in case of major downfall.

Buy 2 Calls at A & C (strike price), and Short 2 Calls at B(strike price). Deploy the strategy in the near month market and when the market is expected to be steady. If the market falls sharply, then option positions can be exited.

Â

Â

| Maximum Profit at Expiry | Central strike - lower strike - cost of spread |

| Maximum Loss at Expiry | Cost of Long butterfly |

| Breakeven at expiry | A + cost of strategy & C- cost of strategy |

| Theta (Time decay) | Better at central strike price |

| Vega (Volatility) | Falling |

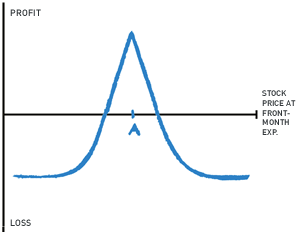

Calendar Spread:

This strategy can be deployed when the market has little expectation to be steady or move a bit downward till near month expiry and a sharp rise in the next or far away month.

Short Call at strike price A (near term expiry) and Buy Call at same strike price A (far term expiry). An early exit in the short Call can be considered if the market shows a sharp rise in the near month expiry.

| Maximum Profit at Expiry | Difficult to estimate |

| Maximum Loss at Expiry | Limited to cost of spread |

| Breakeven at expiry | Difficult to estimate |

| Theta (Time decay) | Helps |

| Vega (Volatility) | Steady till first expiry |

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.