_07_03_2026_03_50_21_133108.jpg)

Nowadays, every listed company is providing earnings guidance, which is nothing but a management update about what is expected from the company in the future. The management also sets up its long-term or short-term goals in the guidance. The earnings guidance cannot be considered reliable source to make a buy or sell call, as it is a subjective view of company’s future performance, which is exposed to many risks and uncertainties.

Let’s have a look at the two companies that have provided their earnings guidance of late.

AUB Group Reaffirms its Earning Guidance

AUB Group Limited (ASX: AUB) is Australasia’s major equity-based insurance broker network running approximately $3.2 billion GWP throughout its network of 93 businesses, servicing more than 550,000 clients and over one million policies in more than 600 locations.

On 28 January 2020, the company notified that it is anticipates delivering toward the top of its earlier announced guidance range of 8-10% growth in adjusted NPAT in FY20. This guidance is centred on primary, unaudited 1H20 financial performance. It is reliant on the presumptions made in the company’s FY19 results, as well as anticipations of trading for the rest of the financial year.

The guidance includes smaller acquisitions and removals of shareholdings in Partner businesses. The company is thrilled to report strong business performance in the first half of FY20. It has made great improvement with its strategic initiatives, and in improving the underlying performance of the company. 1HFY20 results are expected to be released on 25 February 2020.

Expiry of Conditional Sale Agreement to Acquire Coverforce

The company has ceased its conditional agreement with Pemba Capital Partners to purchase Pemba Capital’s stake in Coverforce. The conditional sale agreement was uncertain upon, among other things, transfer of due diligence materials to the company as at the date agreed between AUB and Pemba Capital. Delivery of due diligence materials to AUB has not happened, and AUB has not surrendered its right to due diligence.

In effect, and as the parties have not been able to attain an agreement on a revised date for distribution of due diligence materials, the Conditional Sale Agreement has ceased. AUB will continue to apply its methodical approach to its M&A strategy to purchase businesses that hasten scale and growth, leverage and expand its expertise in key insurance risk areas and market segments, while adding to its core capabilities.

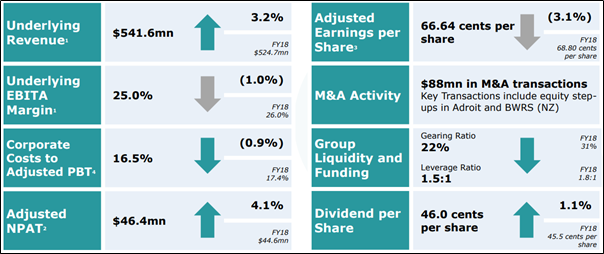

Financial Performance in FY19

In FY19, the company delivered a 4.1% increase in Adjusted Net Profit After Tax of $46.4 million, while maintaining a strong capital position and balance sheet. The company’s core insurance broking and underwriting agency business in Australia and New Zealand operated well, delivering double-digit growth. It continues to have substantial scale and footprint and an excellent market status.

The company’s Underwriting Agencies, Australian and New Zealand Broking businesses all worked well in FY19 with the Adjusted NPAT growing by 10% YoY excluding the result of the Canberra fraud. Growth is anticipated to persist in FY20 period. The adjusted EPS decreased by 3.1% due to the impact of the capital raised in November and will continue to have an impact in FY20 due to the full number of shares issued in FY19 taking effect for calculation purposes.

The company declared a final fully franked dividend of 32.5 cents per share. This, together with the interim dividend of 13.5 cents, results in a full-year dividend of 46 cents, being a payout ratio of 72.9%.

FY19 Performance Snapshot (Source: Company’s Report)

Financial Position of the Company

The company remains to be cautious in managing capital, with the group gearing ratio reducing to 22% in FY19. The business has a robust ongoing cash flow generation, while the corporate entity has access to cash and long-term corporate debt facilities to fund future acquisition and organic growth initiatives. The company’s leverage ratio compiled on a look-through basis has ranged historically between 1- and 2-times net debt to EBITDA and is currently at 1.5 times. The Group’s Interest cover ratio was noted at 11:1.

Stock Performance

The stock of AUB was trading at $12.280 per share on 29 January 2020, down by 0.888% (at AEDT 1:56 PM). The company has a market capitalisation of $914.34 million, as on 29 January 2020. The total outstanding shares of the company stood at 73.8 million, and its 52-week low and high is $10.150 and $13.940, respectively. The company has given a total return of 4.65% and 10.43% in the time period of 3 months and 6 months, respectively.

Credit Corp Reports Double-Digit Growth in First Half

Australia’s biggest debt buyer and collector, Credit Corp Group Limited (ASX: CCP) is dedicated to offer sustainable financial solutions. On 28 January 2020, CCP reported its first-half results for the fiscal year 2020. The key highlights of the same are as follows:

- 15% increase in Net Profit after Tax (NPAT) to $38.6 million;

- 13% growth in the consumer loan book to $230 million;

- Baycorp acquisition on track for full-year NPAT of $6m and integration ahead of schedule.

All segments grew profits robustly, with the US debt buying and consumer lending businesses each growing first half NPAT by more than 20%. The US debt buying division continues to be on course for full-year profit increase of 45 percent to 65 percent.

The Australian/New Zealand debt buying segment generated record collections and NPAT, with solid results from the existing business accompanied by the performance of the acquired Baycorp assets. The company raised PDL or purchased debt ledger market share late in the first half period, creating the pipeline of contracted Australian/New Zealand buying within the preceding full-year guidance range.

The Baycorp acquisition is on track to achieve business case outcomes. The integration is ahead of schedule, with actions taken to date realising $13 million in annualised cost savings and ensuring that the agency businesses in both Australia and New Zealand are operating profitably.

Consumer lending has had a strong start, with the loan book up by 13% over the same point in the prior year. The company tracked previous year’s surprisingly solid growth in new consumer volume with another 8 percent new consumer volume increase. Wallet Wizard is currently well-recognised as the most workable product in its division, and the lack of any continuing fees suggests that it can be less expensive than many major credit card subscriptions.

Credit Corp’s focus in the US has been on expanding production capacity to match investment growth over a prolonged period. Expanded capacity helped deliver collections growth of 57% over the same period in the prior year. The commencement of the second facility in Washington State will ensure that productive capacity continues to grow to meet the US market opportunity.

Credit Corp continued to achieve operating metrics comparable to those achieved by the long-established publicly traded debt buyers. The company has recruited rapidly over the past 8 months, and operating metrics remain in line with those of competitors.

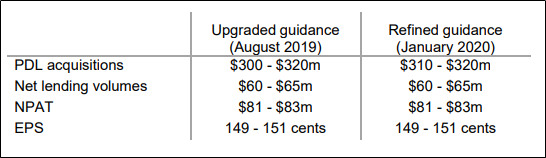

Guidance for 2020

The company provided upgraded guidance with the acquisition of Baycorp in August 2019 and now confirms 15% to 18% growth in NPAT for fiscal 2020. The acquisition and all business segments have performed strongly over the first half and remain on track. With an expanded PDL investment pipeline in Australia/New Zealand and the US as well, the PDL investment guidance range has been tightened between $310 to $320 million.

(Source: Company’s Report)

Stock Performance

The stock of CCP was trading at $34.840 per share on 29 January 2020, up by 6.22% (at AEDT 1:55 PM). The company has a market capitalisation of $1.8 billion, as on 29 January 2020. The total outstanding shares of the company stood at 54.92 million, and its 52-week low and high is $20.410 and $33.740, respectively. The company has given a total return of 5.70% and 32.26% in the time period of 3 months and 6 months, respectively.