Macquarie Group Limited (ASX:MQG) is a popular name in the financial space with presence across 27 countries. The investment management group has expertise in areas such as agriculture, resources, Â commodities, and energy and infrastructure. However, the interesting part is that this global major started a with just 3 staff members; and this was way back in December 1969. The whole idea was to set a group based on international standards and capable enough to offer advisory and investment banking services across the Australian market with penetration extending across the globe in a set time frame. The Macquarie Group operates under two verticals Annuity-style businesses forming around 70 % of the business and Capital markets facing businesses forming about 30% of the business.

Annuity-style businesses have three main segments that include,

Macquarie Asset Management (MAM) â This business is considered to be among the leading 50 global asset managers. The segment helps clients to access a varied set products and services in the areas dealing in infrastructure, equities, real assets, fixed income, liquid alternatives, and multiple asset investment management solutions. Currently, the business has an AUM of $A545.9bn.

Corporate and Asset Finance (CAF) â A provider of solutions in asset finance and management space, CAF is known for dealing in areas such as technology, aircraft, healthcare, industrial, energy, mining equipment and rail. The current assets and loan under the book are $A33.7bn.

Banking and Financial Services (BFS) â This business comes under Macquarie's retail banking and financial services business with a $A40.6 bn Australian loan portfolio, funds on a platform of $A82.5bn and total BFS deposits of $A45.7 bn. Better known to provide personal banking, and wealth management related solutions, the segment offers a varied range of banking products and services to brokers, and retail and business clients. Currently, this business has over 1 million Australian clients.

Capital markets facing businesses: There are two businesses under this vertical-

Commodities and Global Markets (CGM): This business provides clients with risk and capital solutions across physical and financial markets. The business has a diverse platform covering more than 25 market segments, with more than 160 products.

Macquarie Capital (MacCap): This business is known for catering to capital market and provides requisite offerings across many areas including real estate, infrastructure, telecommunications, and so forth.

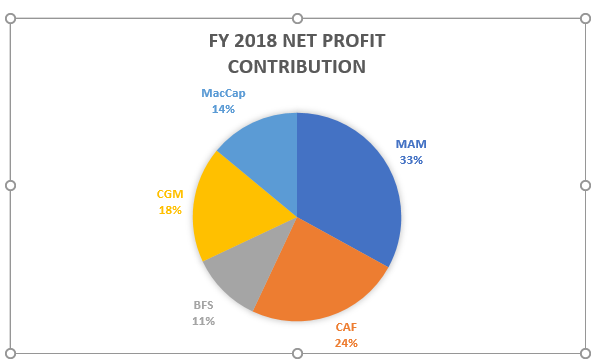

The Net profit contribution for FY2018 of the various business are as shown in the chart (a), This clearly shows that the business derived more than 50% of its net profit from MAM and CAF business alone.

FY2018 Net Profit Contribution (Source: Company Reports)

From the analysis standpoint, Over the past few years, the efficiency ratio of the company has improved and reported at 73.9% in 1HFY19 showing that the companyâs financial health is improving. Further, the company is generating better returns for its shareholders than its peers as it reported a pre-tax ROE of 10.4% in 1HFY19 above the industry median of 4.5%. Return on Equity (RoE) is one of the most important ratios as it measures the profitability of the equity holder. The Pre-tax ROE of MQG for the Year 2018 was 21.7% vs. 20.2% in the year 2017. The Pre-Tax ROE has been on an upward trend for MQG for the past 5 years. The company has been able to maintain its asset quality, the loan loss provisioning (% of Average loans) was at 0.08% in the year 2018 vs. 0.35% in the year 2017. This ratio indicates that the company has made less provision and hence a better quality of lending being followed. This is further validated by the Nonperforming Loans (as % of Total Loans) which came in at 0.49% in 2018 vs. 0.74% in 2017.

The improvement in profit matrices is reflecting on the valuation metric of MQG. It reported a marginally higher P/BV and P/E multiples of 2.6x and 16.65x respectively against the industry median of 1.1x and 13.5x respectively. Further, the EV/EBITDA multiple provides a view from a potential acquirer of the business. The company is trading at an EV/EBITDA of 10.6x vs industry average of 13.4x.

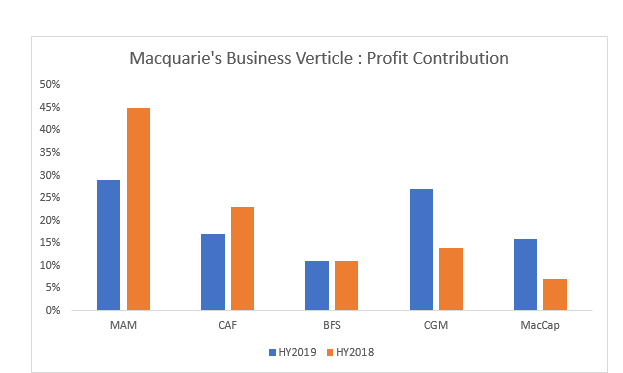

While studying the half-yearly results of Macquarie, one notices that the profit contribution mix is changing over the year 2018 as compared to 2017. The below chart is capturing the change.

Profit Contribution from individual business vertical (Source: Company Report)

Profit Contribution from individual business vertical (Source: Company Report)

The net profit after tax contribution from the commodities business and capital market business is steadily increasing and considering the cyclical nature of the commodities and capital markets the market does not seem to give Macquarie the previously enjoyed higher valuation multiples.

The contribution from its annuity business is currently undergoing a down phase. The company had guided for 10% increase its FY2019 profitability. In the meantime, the share price of the company has risen 9.88% in the past three months as at March 01, 2019 and trading close to 52-week higher level. However, by looking at its decent fundamentals and aforesaid facts, the stock looks good in the medium to long-term period.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.