The political and war tensions between Iran and US, ongoing trade conflicts between US-China and devastating bushfire in Australia has created a sense of tension among Australian investors. Investors are mostly worried about earning returns in this uncertain environment.

Dividend stocks could be the solution to their problems. As interest rates in Australia are already at record low levels, dividend stocks are already viewed by some as the most attractive investment opportunity in the current uncertain scenario.

Analysts generally analyze dividends yields to know the best performing dividend stocks on the exchange. We have noticed that for quite some time, Alumina Limited (ASX: AWC) has been sitting at the top of the list of highest dividend yield stocks. As per ASX, the stock of this metal and mining giant currently has an annual dividend yield of 11.71%, calculated on the closing market price of 28 January 2020 i.e. $2.230.

Alumina Limited is the closest thing in the world to a listed, pure play alumina company. Compared to its industry peers, it is almost fully focused on refining the intermediate alumina product in the aluminium supply chain. The company has a market cap of $6.42 billion and outstanding shares of 2.88 billion.

The company invests in world-wide in bauxite mining, alumina refining and selected aluminium smelting operations through its 40 per cent ownership of Alcoa World Alumina & Chemicals (AWAC) which is a leading global bauxite and alumina business in Australia which owns and operates long-life, low cost bauxite and alumina assets.

The Board’s policy on dividends is that it intends on an annual basis to distribute net cash from operations, after capital contributions back into the AWAC joint venture, after debt servicing and after corporate cost commitments have been met. In terms of dividends, the year 2018 was a record year for shareholders. The outstanding operating result over the period enabled dividends to increase by 68 percent. The Company paid a total dividend of 22.7 cents per share for 2018. Later for six months ended 30 June 2019, the company paid a dividend of 4.4 US CPS which was 100% franked. The company has not yet disclosed the dividend amounts for the latter half.

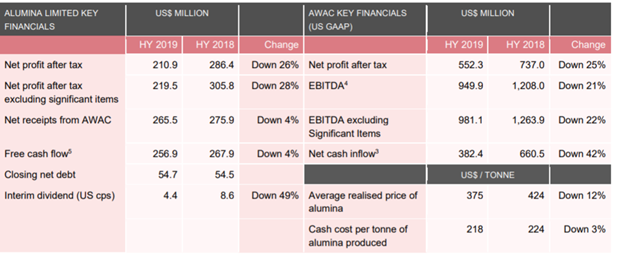

For the first half of 2019, the company reported a statutory net profit after tax of US$210.9 mn and EBITDA of US$949.9 mn.

H1 2019 Financials (Source: Company Reports)

Alumina’s key strategy is, through Alcoa World Alumina and Chemicals (AWAC):

- to invest in and own and operate long-life, low cost bauxite and alumina assets, preferably large and able to be expanded and;

- for AWAC’s alumina to be priced off alumina’s fundamentals, in terms of supply and demand and construction and operating costs of alumina.

The AWAC joint venture was formed to align the interests of Alcoa of Australia and Alcoa Inc’s non-Australian global upstream portfolio. This Joint venture produces more than 12 million tons of alumina per year, or about 10% of global smelter-grade alumina production and 21% of Western world production. The core Wester Australia assets comprise 2 bauxite mines, and 3 alumina refineries which produce over 9 million tons of alumina per year. Nearly 60 years after they commenced operations, these remain outstanding, low cost, long life assets with decades of contribution ahead of them. Other assets that AWAC operates are:

- the long-life Juruti bauxite mine and the Alumar refinery in Brazil, which was expanded in the mid-2000s and AWAC’s share of alumina production is now 1.5mtpa

- the San Ciprian refinery in Spain which produces 1.6mtpa of smelter grade and chemical grade alumina and

- the Portland smelter in Victoria, which has an agreement in place to operate until at least the middle of 2021. Going forward, Portland requires a lower cost and reliable energy solution.

For some years, the Company’s role was to play the good soldier. It has contributed to the growth of AWAC when required to do so,and has provided a highly efficient platform for its shareholders to benefit directly from the quality of the AWAC portfolio.

At the time of the release of its Q4 2019 earnings, CEO, Mike Ferraro, commented that Year on year AWAC has improved performance in areas which it can control; both mining and refining annual production is 4% higher than 2018 and the average annual cost of alumina production is 7% lower over the same period; he also told that these factors have contributed to fourth quarter 2019 net distributions from AWAC being similar to the previous quarter despite the average alumina price falling further.

Few Other high Dividend Yield Stocks

In terms of dividend yield, behind Alumina Limited, we have Whitehaven Coal Ltd (ASX: WHC) on the list, a leading Australian producer of premium-quality coal, which has annual dividend yield of 11.62%. During the last financial year, the Whitehaven Coal delivered record returns to shareholders with a final dividend of 30 cents, taking full year dividends to 50 cents per share. WHC is currently trading at a price of $2.520 with a market cap of $2.6 billion.

In Australia, Real Estate Investment Trusts (REITs) are very popular among investors as they provide consistent distributions mainly derived from the rental income earned on the trust’s properties. National Storage REIT (ASX: NSR), ASX-listed company which owns and operates self-storage centres, is one of the popular REITs among retirees. During its last financial year, NSR delivered distributions in line with guidance at 9.6 cents per stapled security. This includes, a final distribution of 5.1 cents per stapled security for the 6 months to 30 June 2019, paid on 5 September 2019 and an interim distribution of 4.5 cents per stapled security for the period 1 July 2018 to 31 December 2018, paid on 1 March 2019.

Although dividend yield analysis is one of the most common and simplest methods of identifying good dividend stocks, it should not be the only criterion for selecting a stock as many times, dividend yields are inflated or deflated due to sudden increase or decrease of the share price.