The Fast Food Industry entails businesses that involve production, packaging and distribution of fresh food, prepared foods and packaged foods.

Changes in consumer preferences are shaping the fast food industry in Australia.

The demand for the fast food industry in Australia has been significantly impacted over the past few years with a rise in consumer health awareness. The consumer is now much more concerned about the nutritional content of the food and tends to choose healthier options. As a result, the companies in the industry have made significant efforts to fit in with the rising demand for more nutrition than taste by incorporating consumer concerns and bringing in healthier, premium choices with less fat, sugar and salt content.

Therefore, it can be said that the threats and opportunities in the fast food industry are predominantly characterised by the following:

- Consumer awareness of the food they are eating and the health implications thereon.

- Consumer preference for healthier and premium quality food, which, in turn, can act as a growth driver for the businesses that have a consumer-friendly approach and take into consideration the changing behaviour.

- Last but not least, there lies an opportunity for businesses in the industry to introduce new and healthier choices in order to tap the market demand.

Some of the fast food franchises operating in Australia are Subway, KFC, McDonaldâs, Hungry Jaclokâs, Dominoâs and Pizza Hut.

Let us look at 2 stocks in the fast food industry-

Collins Foods Limited (ASX:CKF)

Collins Foods Limited (ASX:CKF) is primarily engaged in the operation, management and administration of restaurants in Australia, Europe and Asia. The company operates through three restaurant brands, namely KFC, Taco Bell and Sizzler.

The company released a new announcement to the exchange regarding the planned succession of Graham Maxwell, the companyâs Managing Director & CEO. His retirement is due on 1st July 2020 and the company intends to appoint Drew OâMalley as the new Chief Executive Officer. Drew is currently serving as the companyâs Chief Operating Officer in Australia and is responsible for the day-to-day operations of the companyâs expanding network of restaurants in Australia. He has extensive experience in the restaurant industry with a proven track record of growing businesses. Prior to Collins Foods, he worked with AmRest and held various positions, including COO for Central Europe, Managing Director of Starbucks CEE and Brand President of KFC in Poland and the Czech Republic.

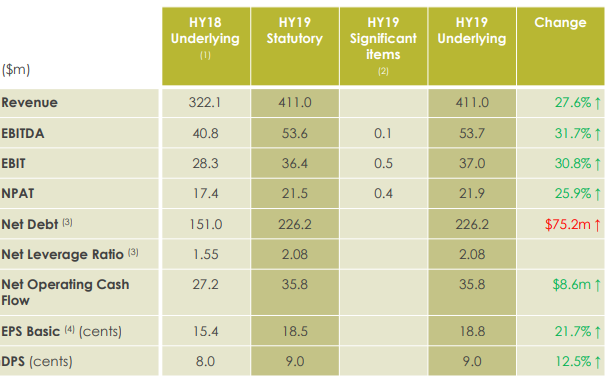

Financial Highlights: For the half-year ended 14th October 2018, the company reported revenues of $411 million, witnessing an increase of 27.6% on the prior corresponding period revenues of $322.1 million. Statutory EBITDA during the period stood at $53.6 million, reporting an increase of 42.9% on HY18 statutory EBITDA of $37.5 million. Underlying EBITDA for the period amounted to $53.7 million, up 31.7% on the pcp value of $40.8 million. Statutory NPAT for H1 FY19 totalled $21.5 million as compared to HY18 statutory NPAT of $12.7 million, reporting an increase of 69.3%. Underlying NPAT amounted to $21.9 million, up 25.9% on the pcp value of $17.4 million.

During the period, the operating cash flow for the company amounted to $35.8 million, up 31.6% compared to the HY18 operating cash flow of $27.2 million. A fully franked dividend of 9 cents per ordinary share was declared, up by 12.5% on HY18âs dividend of 8 cents per share.

Key Financial Metrics for 1HFY19 (Source: Company Presentation)

KFC Australia: For the six month period, KFC Australia witnessed strong growth with a national footprint of 228 KFC restaurants. The segment reported strong financial results with EBITDA rising by 23.5% to $56.1 million in the current period as compared to the prior corresponding period. EBITDA margins also increased to 17% as compared to an HY18 EBITDA margin of 16.8%. H1 FY19 period marked a focus on operational efficiencies and margin management across the network, which helped the company to achieve a remarkable performance in the segment. The company completed the acquisition of three restaurants from Yum! and has a target to establish 40 to 45 new KFC restaurants in Australia over the next five years.

KFC Europe: This segment covers its operations through 17 restaurants in Germany and 18 in the Netherlands. The revenue from the segment grew by 121.5% to $56.9 million as compared to the pcp. The company is still in its infancy and provides an opportunity to drive long term growth for the business in Europe. The company is planning to build four new restaurants in Germany and the Netherlands in the second half of FY19.

Sizzler: Sizzler continued to generate earnings with Sizzler Asia royalty revenues up by 19% due to new restaurant openings as well as an increase in the same-store sales. Overall, Sizzler revenue reported a decline of 7.6% at $22.2 million in H1 FY19.

Taco Bell: The company continued the expansion by opening its second Taco Bell restaurant in Robina, Queensland and is planning to open two more restaurants before the end of CY2019. The company entered into a development agreement with Taco Bell, a subsidiary of Yum! Brands Inc. to build 50 restaurants over the next three calendar years.

On the outlook front, the company is focused on growth strategy through the opening of new restaurants in Australia and Europe by the end of the financial year. The company also aims to increase the size of its home delivery footprint in the next six months.

The stock of the company generated positive returns of 21.62% and 30.23% over a period of three months and six months, respectively. It is currently trading at a market price of $7.620, down 5.926% on 21st June 2019, with a market capitalisation of $943.74 million.

Dominoâs Pizza Enterprises Limited (ASX:DMP)

Dominoâs Pizza Enterprises Limited (ASX:DMP) is engaged in the operation of retail food outlets and the operation of franchise services. The company recently updated the investors on the speculation in the UK media that Andrew Rennie, CEO Europe, will be replacing the outgoing Managing Director of Dominoâs Pizza Group, plc. The company mentioned that the speculations were insubstantial, and Andrew will continue his current role as CEO of Europe.

In the month of April, the company entered into an asset sale agreement. The agreement entails the acquisition of corporate store assets, rights and entitlements in relation to the franchise operations in Denmark, formerly owned by Dominoâs Pizza Scandinavia A/S. The company made the acquisition for a consideration of EUR 2.5 million. The company also revised the guidance for the future store count in Europe. It changed the previous guidance of 2,700 stores to 2,850 stores as a result of the acquisition. The acquisition will serve as an additional growth platform for the European operations of the company, as Denmark has a large population and a good market potential to accelerate the growth.

Financial Highlights: For H1 FY19, the company reported global sales of $1.43 billion, up +14.6% on the pcp. EBIT for the period amounted to $108.3 million, up +12.1% on pcp. Network sales for Australia/New Zealand were reported at $592.5 million, up +6.2% on pcp. Network sales in Europe and Japan grew at a rate of +17.4% and +9%, respectively. The company expanded its network of stores with 13 new openings in Australia/New Zealand, 33 in Europe and 31 in Japan.

During H1 FY19, the company depicted a strong underlying operating cash flow up 26.2% with remarkable cash conversion rate. The market for pizza and fast food categories grew tremendously in New Zealand. The overseas market in Europe and Japan accounted for a majority of the share in both revenue and EBITDA. The market contributed to more than 70% of the revenue and more than half of the EBITDA, with a value of $71 million. With a much larger population in the current overseas markets than that of Australia, the companyâs global business provides a pathway for future growth.

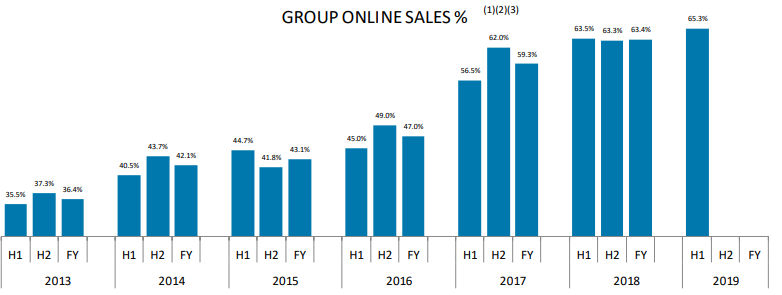

The company reported a remarkable online performance with a total of 32.4 million orders processed in the half year. Online sales for the period increased +16.5% on the prior corresponding period. The global network sales during the period witnessed an increase of +3.3% on a same-store sales basis. Benelux, Germany, Japan and New Zealand depicted strong results with softer performance in Australia. The performance in France was lower than the expected level.

Group Online Sales (Source: Company Presentation)

FY19 Guidance: The company provided an EBIT guidance to be at the bottom end of the range of $227 million to $247 million. The same-store sales for the entire year are expected to be at the mid to lower end of 3% to 6%. The companyâs anticipated store openings in the range of +200 to +215 organic new stores will lead to a growth outlook of +7% to 9%. Net CapEx is expected to be within the ambit of $60 million to $70 million.

The stock of the company is currently trading at a market price of $37.660, down 1.825% on 21st June 2019, with a market capitalisation of $3.28 billion and a PE ratio of 28.350x.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.