Adelaide Brighton, Reliance Worldwide Corporation, Nufarm and Blackmores have performed decently in terms of revenue generation, with revenues in the first half reporting an increase as compared to pcp while Costa Group witnessed a slight decline in revenue during the period but generated good receipts from the international segments. Pilbara Minerals also performed well with an increase in production from its 100%-owned Pilgangoora Lithium-Tantalum Project.

Looking at the returns on the stock over a period of one year, there has been a downward movement in the prices with the largest decline witnessed by Nufarm Ltd. Nufarm Ltdâs stock has generated a negative return of 48.72%. The decline in the case of Costa Group was almost similar at a rate of 47.25%, followed by Pilbara Minerals that witnessed a downfall of 46.15%. Adelaide Brighton, Blackmores Limited and Reliance Worldwide Corporation experienced a decrease of 37.29%, 33.86% and 33.45%, respectively.

Adelaide Brighton Limited (ASX:ABC)

Adelaide Brighton Limited (ASX:ABC) engages in the manufacturing and distribution of cement, premixed concrete, aggregates, lime, sand and concrete products. As per the recent announcement related to June 2019 Quarterly Rebalance by S&P Dow Jones Indices, Adelaide Brighton Limited was removed from the S&P/ASX 100 Index, effective at the open on June 24, 2019.

In May 2019, the company signed a contract with OZ Minerals Limited for the continuation of cement supply to the OZ Minerals Prominent Hill Operation for a term of five years. The company will also supply aggregate and sand from its Sellicks Hill Quarry as a part of the contract.

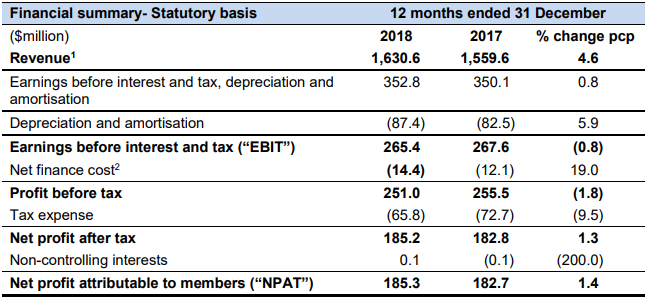

During the full year ended 31st December 2018, the company generated revenues amounting to $1,630.6 million, up 4.6% on the prior year. The growth in revenue was attributable to the benefits from demand across the residential and non-residential sectors, acquisitions made in 2017 and stable lime demand. NPAT during the period amounted to $185.3 million, up 1.4% on the previous year. EBIT for the period stood at $265.4 million, depicting a decrease of 0.8% as compared to 2017. The companyâs balance sheet remained strong with net debt to equity gearing of 34.1% at the end of the year and leverage ratio of 1.2x.

Yearly Results Summary (Source: Company Reports)

The stock at market close was trading at a price of $4.340, up 1.402%, with a market cap of $2.79 billion on 05th July 2019.

Reliance Worldwide Corporation Limited (ASX:RWC)

Reliance Worldwide Corporation Limited (ASX:RWC) is a supplier of premium water flow and control products for the plumbing industry. The company recently updated on the change in substantial shareholding of AustralianSuper Pty Ltd, wherein the voting power has increased from 5.22% to 6.63%.

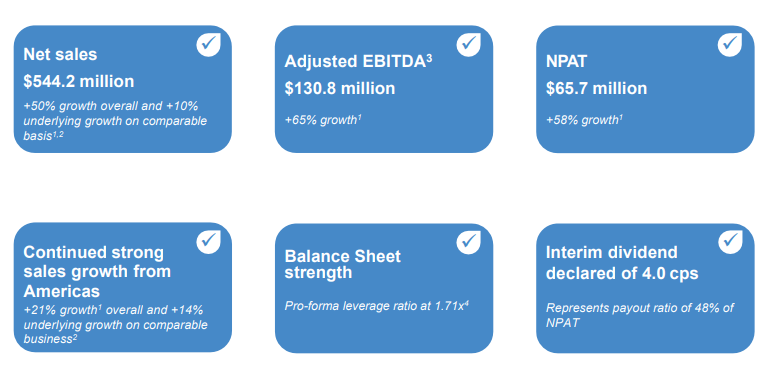

During the half year ended 31st December 2018, the company generated net sales of $544.2 million, reporting 50% overall growth and 10% underlying growth on a comparable basis. Adjusted EBITDA for the period stood at $130.8 million, depicting a growth of 65% on pcp. NPAT for the period was reported at $65.7 million, up 58% on the prior corresponding period. During the period, the company witnessed continued strong sales growth from the Americas. The Board also declared an interim dividend of 4.0 cents per share, representing a payout ratio of 48% on NPAT.

1HFY19 Financial Highlights (Source: Company Presentation)

The company recently revised the FY19 EBITDA guidance, which was earlier expected to be in the range of $280 million to $290 million. The updated guidance was in the range of $260 million to $270 million, owing majorly due to market-specific factors negatively impacting performance and results.

The stock at market close was trading at a price of $3.720 million, up 1.639%, with a market cap of $2.89 billion on 5th July 2019.

Costa Group Holdings Limited (ASX:CGC)

Costa Group Holdings Limited (ASX:CGC) is the largest fresh produce supplier to the major Australian food retailers. The company recently updated the exchange that Pendal Group Limited became a substantial shareholder with a voting power of 5.05%.

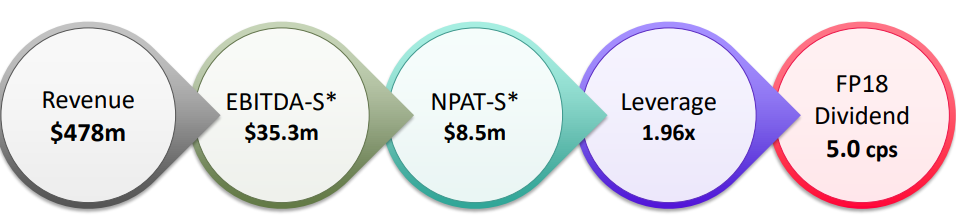

On the financial front, the company generated $478 million in revenue for the financial period ended 31st December 2018, down 2.4% on pcp. EBITDA-S was reported at $35.3 million, down 42% on the prior corresponding period. The companyâs net profit after tax before SGARA, material items and amortisation stood at $8.5 million. A fully franked dividend of 5.0 cents per share was also declared during the year. With harvests in Morocco and China and licensing income from fruit sales occurring predominantly in the first half, the receipts from the international segment were heavily attributable to calendar H1. During the first half, International revenues were $6.6 million as compared to the prior corresponding period revenues of $3.6 million.

Financial Highlights (Source: Company Presentation)

Under its growth program during the period, the company completed the acquisition of NCF Citrus and Grape Farm in Sunraysia in December. The company also conducted berry expansion programs across Australia, Morocco and China. In addition, the period also saw the approval of new tomato glasshouse expansion.

At market close, the stock was trading at $4.090, down 0.969%, with a market cap of $1.32 billion on 5th July 2019.

Nufarm Ltd (NUF)

Nufarm Ltd (ASX:NUF) manufactures and sells crop protection products. The company recently announced the appointment of Fiona Smith as the Company Secretary in place of retiring CS, Rod Heath.

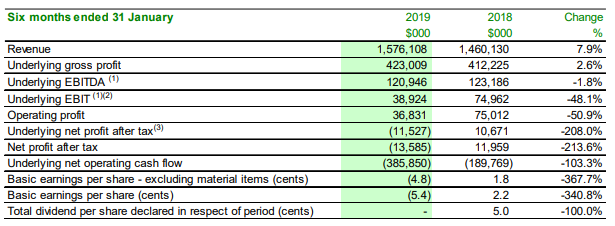

During the half year ended 31 January 2019, the company generated revenues amounting to $1,576 million as compared to $1,460 million in HY18. Underlying EBITDA for the period was $120.9 million, down 2% on pcp value of $123.2 million. Due to the expansion of market share for key products and higher soy plantings, the company witnessed continued sales growth of 18% in the Latin America region. The period saw sales getting impacted in Europe due to a slow start to the season with dry weather in Central and Northern Europe and a delay in purchases due to high channel inventories.

Financial Summary (Source: Company Presentation)

As per the guidance provided, FY19 EBITDA is expected to be in the range of $440 million to $470 million. The year-end leverage ratio for the period is expected to be below 3x, along with a medium term leverage target of 2x. Average net working capital to sales are anticipated to be between 43% to 44%.

The stock at market close was trading at a price of $4.600, up 3.604%, with a market cap of $1.69 billion 5th July 2019.

Blackmores Limited (ASX:BKL)

Blackmores Limited (ASX: BKL) develops and sells natural health products for humans and animals, including vitamins and mineral nutritional supplements. The company recently updated that it has issued 695 fully paid ordinary shares for the purpose of staff share acquisition plan. In another update, the company announced that Alastair Symington was appointed as the new Managing Director and Chief Executive Officer. His term as the CEO & MD will begin from 1st October 2019.

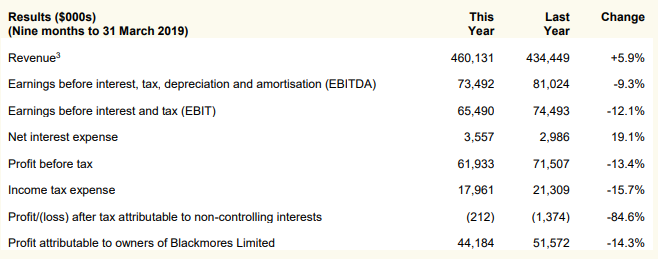

During the third quarter of the financial year 2019, net profit after tax amounted to $10 million, down 43% on pcp. Profit for the nine month period amounted to $44 million, reporting a decline of 14% as compared to Q3 FY18. Revenues during the period stood at $460 million, up 6% on pcp. The company retained its position as the No. 1 brand in Australia with 14.9% of domestic market share. Sales from China segment went up 19%, owing to increased in-country and export sales.

Nine Months Financials (Source: Company Reports)

Outlook: The management expects modest full-year revenue growth. The performance in the second half is not expected to be ahead of the first half. The company is targeting savings of $60 million over the next three years and progressing with its plan to streamline the business.

The stock of the company at market close was trading at a price of $93.850, up 2%, with a market cap of $1.6 billion on 5th July 2019.

Pilbara Minerals Limited (ASX:PLS)

Pilbara Minerals Limited (ASX:PLS) is engaged in the exploration and development of mineral resources, primarily the Pilgangoora Project.

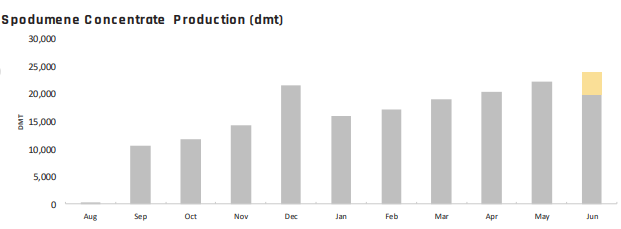

In a recent update on the production, operations and sale of spodumene concentrate, the company reported production of 22,375 dry metric tonnes of spodumene concentrate in the month of May with production forecast in the range of ~20 to 24 kt for the month of June. The concentrate is generated from the companyâs fully-owned Pilgangoora Lithium-Tantalum Project in Western Australia. In addition, the period saw continuous negotiations with POSCO, for the proposed joint venture chemical conversion plant in South Korea.

Spodumene Concentrate Production (Source: Company Reports)

During the quarter ending March 2019, the company reported production of 52,196 dry metric tonnes of spodumene concentrate as compared to 47,859 dmt in the December quarter. Sales for the quarter were reported at 38.562 dmt as compared to 46,598 dmt in the December quarter, impacted by the delay of one shipment.

During the quarter, the company received $50 million from Jiangxi Ganfeng Lithium Co. Ltd, owing to an Equity Subscription Agreement announced earlier. As at 31st March 2019, the company had a cash balance of $103.9 million.

The companyâs stock at market close was trading at a price of $0.500, up 2.041%, with a market cap of $907.2 million on 5th July 2019.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.