The Australian health system is tagged amongst the best in the world and focusses on providing safe and affordable health care for all the Australians. The federal, state and local government jointly run the system to ensure its adherence. As per the latest statistics provided by the Australian Bureau of Statistics, in 2017-18, 56.4 percent Australian citizens who were 15 years old or above regarded themselves to be in great health.

Let us quickly browse through the latest developments that took place in Australiaâs healthcare sector, as announced by the Department of Health in August 2019:

- The Australian Governmentâs Medical Research Future Fund Frontiers granted $1 million dollar to a team of Melbourne researchers to develop, test and implement portable brain imaging tools in air and road ambulances.

- The Government pledged an additional $19 million towards funding, for a range of initiatives, pertaining to free the Pacific region from the diseases.

- The Aussie Government would support the global efforts to eradicate TB in South East Asia and Pacific area and announced a $13 million commitment for the same.

- The Australian Breastfeeding Strategy: 2019 and Beyond was launched in the World Breastfeeding Week, on 5 August 2019, and was backed by a $10 million investment to support the cause.

The above facts and events prove that Australia has a robust health care structure. Let us now look into the performances of five healthcare stocks, listed and trading on ASX and understand their stance in the Australian share market:

Althea Group Holdings Limited (ASX: AGH)

Company Profile: Engaged in the production and supply of pharmaceutical grade medicinal cannabis both domestically and internationally, AGH is based in Melbourne. The Group contains various licenses and permits for the importation, cultivation and more of the medicinal cannabis in the Australian region. AGH was listed on the ASX in September, last year.

Stock Performance: After the close of business on 16 August 2019, AGHâs stock was valued at A$0.745, down by 9.697 per cent, with a market cap of A$192.31 million and ~233.1 million outstanding shares. Also, the YTD return of the stock is 211.32 per cent. In the last one, three and six months, it has delivered returns of -32.65per cent, +42.24per cent and +114.29per cent, respectively.

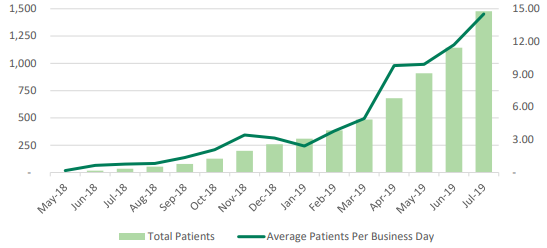

Record Breaking July 2019 and Tetra Agreement: On 7 August 2019, the company pleasingly notified that 334 patients were added in July, which was the largest number of new patients prescribed with AGHâs products in a single month to date. This took the patient count to 1,523 in Australia. As an icing on the cake, 245 Healthcare Professionals prescribed the medicinal cannabis. The rapid uptake of AGHâs products is triggered by the strategy of Althea Concierge, the proprietary technology platform that greatly reduces application times for the professionals to consider prescriptions.

Patient growth over the past year (Source: AGHâs Report)

Further, the company informed that it had entered into agreement with Tetra Health, a patient support services provider of medicinal cannabis, who would assist AGH as a non-exclusive education and distribution partner of the companyâs products in the country.

Mayne Pharma Group Limited (ASX: MYX)

Company Profile: A tech-savvy pharma player aimed at applying its drug delivery expertise to commercialise branded and generic pharmaceuticals, MYX provides contract development and production services to over 100 clients across the globe. Mayne Pharma was listed on the ASX in the year 2007.

Stock Performance: After the close of business on 09 August 2019, MYXâs stock was valued at A$0.44, down by 4.348 per cent, with a market cap of A$728.15 million and ~1.58 million outstanding shares. With a P/E ratio of 15.65x, the YTD return of the stock is negative 38.26 per cent. In the last one, three and six months, it has delivered returns of -8.91per cent, -17.12per cent and -44.91per cent, respectively.

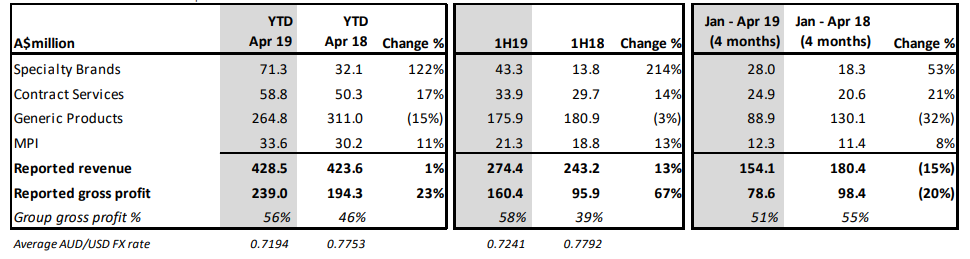

Market Update: On 14 May 2019, MYX released an unaudited trading update for the 10 months ended 30 April 2019, stating that the business witnessed a challenging start to CY2019, given the competitive pressure on its key products including liothyronine and dofetilide, besides wholesaler destocking in the retail channel, failure-to-supply penalties and shelf stock adjustments. Amid these challenges, the Specialty Brands increased by 53 percent, Metrics Contract Services rose by 21 percent and Mayne Pharma International grew by 8 percent, on pcp.

Trading Update (Source: MYXâs Report)

Further, 4QFY19 period is expected to generate better results driven by a rebound in Generic Products and ongoing growth in other company segments. Moreover, of late specialty brand launches of TOLSURA and LEXETTE would boost the FY20 results. Besides, initiatives at the Greenville site, growth of the generic and proprietary dermatology, improved retail generic performance and womenâs health portfolios would support the outlook. Further, 2020 would be the year of launch for generic NUVARING®.

Paradigm Biopharmaceuticals Limited (ASX: PAR)

Company Profile: A Bio-pharmaceutical entity, PAR concentrates on repurposing the medicine, pentosan polysulphate sodium - an FDA approved drug, for the lead clinical indication of bone marrow edema and cure from inflammation. Paradigm Biopharmaceuticals was listed on the Australian Securities Exchange in the year 2015.

Stock Performance: After the close of business on 16 August 2019, PARâs stock was valued at A$1.390, down by 1.418 per cent, with a market cap of A$271.01 million and ~192.21 million outstanding shares. The YTD return of the stock is 42.24 per cent. In the last one, three and six months, it has delivered returns of -17.06 per cent, -6 per cent and -26.09 per cent, respectively.

First IND submission to the US FDA: On 7 August 2019, the company notified that it would file a number of submissions to Global Regulatory Authorities to enhance commercialisation of Zilosul® (iPPS).

Further, the company notified that it had filed its first IND submission to the US FDA, wherein 10 Americans would be treated with Zilosul® (iPPS). The Clinical and Regulatory Teams would work towards the submissions to the US FDA for the Stage 2/3 Clinical Trial for MPS and the Stage 3 Clinical Trial in Osteoarthritis and the Australian Therapeutic Goods Administration for the Provisional Approval of Zilosul® (iPPS) to treat Osteoarthritis.

The company has already completed the Pain reduction MoA of iPPS and has sent the manuscript for review and publication.

Starpharma Holdings Limited (ASX: SPL)

Company Profile: A Biotechnology player, SPL concentrates on the advancement of dendrimer technology for pharma, life science and further applications, SPL was listed on the ASX in 2000 and has its registered office in Melbourne. The company focusses on value creation via commercialisation of its proprietary produces formed on dendrimer nanotechnology.

Stock Performance: After the close of business on 16 August 2019, SPLâs stock was valued at A$1.2, down by 3.226 per cent, with a market cap of A$460.93 million and ~371.72 million outstanding shares. The YTD return of the stock is negative 16.98 per cent. In the last one, three and six months, it has delivered returns of -7.46 per cent, -3.13 per cent and -15.89 per cent, respectively.

Commencement of phase 1/2 DEP® irinotecan trial: On 8 August 2019, the company intimated that it had received the necessary regulatory and ethics approvals to start the phase 1/2 clinical trial for DEP® irinotecan, the third DEP® product to enter the clinic, to analyse the safety, tolerability and pharmacokinetics of DEP® irinotecan. UK cancer centres would conduct the trial with approximately 40-45 patients, scheduled to be enrolled.

Three UK hospitals amid the many to conduct the trial (Source: SPLâs Report)

Besides this, the company is looking forward to AstraZeneca âs first DEP® product, AZD0466 to begin trial later this year.

Medical Developments International Limited (ASX: MVP)

Company Profile: A player from the pharmaceutical drug business, medical and veterinary equipment business, MVP was listed on the ASX in 2003. The company has a range of products in the areas of pain management, asthma and resuscitation along with veterinary equipment.

Stock Performance: After the close of business on 16 August 2019, MVPâs stock was valued at A$4.78, down by 1.24 per cent, with a market cap of A$317.1 million and ~65.52 million outstanding shares. The YTD return of the stock is negative 13.62 per cent. In the last one, three and six months, it has delivered returns of -21.43per cent, -4.91per cent and 23.79 per cent, respectively.

Meeting with the FDA: On 19 July 2019, the company notified that it had a meeting with FDA in June to discuss the IND clinical hold letter issued in August 2018.

MVP anticipates that it would be able to address an entire, all the clinically held problems during Q120 period. As per CEO, Mr. John Sharman, the company was clear of the requisites and was confident that the safety data for Penthrox® required by the FDA would be satisfying. Further, the FDA had given a nod for an animal study to forecast idiosyncratic liver reaction to Penthrox® would not be needed to carry on. Instead, the company would conduct an animal study that replicates the human dosing regimen for the same and would take six months to accomplish this.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.