A nation requires certain tools and governance to achieve its?macroeconomic?objectives. Two such tools, rather policies to give a push to the economy in recession?and restrain it when it is overheating are the monetary policy and fiscal policy.

Both these policies impact an economy and have similar goals, as their implementation by the nation?s supreme authority is meant to reduce the cyclical fluctuations in the economy. Government and Central Banks use a mix of both based on prudent analysis of several factors, depending on the issue to deal with which may include high levels of unemployment, alarming inflation levels (inflated/deflated), slower economic growth, currency appreciation/ depreciation, etc.

In today?s article, we would understand the difference between the two widely recognized tools and acquaint ourselves with the post-LIBOR world in Australia. But before this, let us understand the two policies in discussion:

Monetary Policy

Adopted by nation?s monetary authority Involving changing the interest rate and influencing the money supply

The process of preparing, declaring, and executing the plan of actions to be taken by an economy?s central bank/ concerned monetary authority constitutes monetary policy. In a nutshell, it is the central bank?s actions and communications?that manage the money supply (credit,?cash, checks,?and money market?mutual funds) in the economy.

The main three objectives of a monetary policy are:

- to manage?inflation;

- to reduce?unemployment;

- to promote moderate long-term?interest rates.

The utilisation of this policy toolx` can be of two types- expansionary (to lower unemployment and avoid?recession by increasing liquidity and giving banks more money to lend) or contractionary (to?reduce inflation by shunning the money supply and restricting the amount of money banks can lend).

Aimed at achieving the macroeconomic objectives, the monetary policy increases liquidity to create economic growth and reduces it to prevent inflation. Liquidity can be increased via reducing discount rate, undertaking Open Market Operations and reducing the reserve requirements by the nation?s apex bank.Common monetary policy instruments include:

- Discount Rate - rate at which commercial banks undertake borrowings from the apex bank

- Reserve Requirement- certain fixed portion of bank?s deposits to be kept as reserves with Central Bank

- Open Market Operations (OMO) ? buying/selling securities in the open market

Fiscal Policy

Involves the government changing tax rates and levels of government spending to influence aggregate demand in the economy

Fiscal adjustment pans out to be another way in which an economy?s government adjusts its spending levels and?tax rates?to supervise and influence a nation's economy.

The main objective of a sound fiscal policy is to ensure?healthy economic growth and influence the overall economic productivity.

Fiscal policy can be of two types- expansionary (which is used to combat recession and stimulate economic growth, wherein the government either spends more,?cuts taxes, or both to put more money into consumer pockets) and contractionary (to slow economic growth and stamp out?inflation).

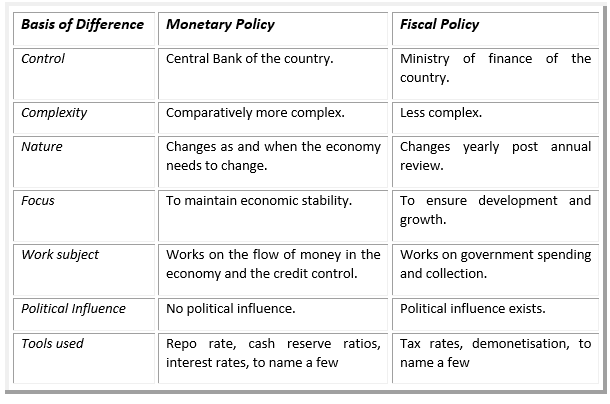

How Does Monetary Policy Differ From Fiscal Policy?

In an ideal scenario, macroeconomists believe that monetary policy should work in close collusion with the national government's?fiscal policy.?Let us understand the differences between these macroeconomic concepts:

Even though the policies are functionally non-similar and are utilised at different situations, both the policies aim at creating a more stable economy illustrated by low inflation and encouraging economic growth. Moreover, they are an attempt to shun down economic fluctuations and soften the economic cycle.

Now that we understand two significant policies, which are addressed in almost every economy of the world, let us concentrate closer to home and look at the post-LIBOR world in Australia:

The LIBOR Concept

A uniform measure which has undergone several changes over the years, and often referred to as the benchmark interest rate for financial contracts worldwide, the London Interbank Offered Rate?(LIBOR) is one of the most globally significant numbers in finance.

It is the average interest rate at which the key global banks lend money to each other for short-term loans in the international interbank market. It is thus the borrowing cost between banks, wherein the rate is calculated and circulated on a daily basis (each business day) by the Intercontinental Exchange (ICE).

The ICE checks with the key banks on the amount that they would charge other banks for short-term loans, takes out the highest and lowest figures and calculates the average (trimmed average), which is posted each morning as the daily rate, making it a non-static figure.

Besides being the borrowing costs between banks, LIBOR affects consumers as much as it does the financial institutions, as it is the basis for consumer loans in economies across the globe (the rate aids in calculating the borrowing between banks and consumers).

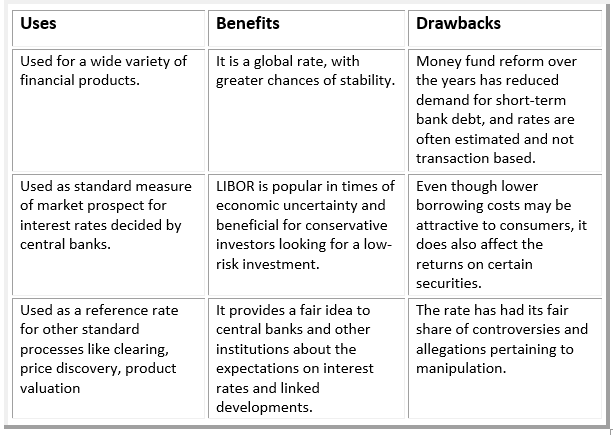

Uses, Pros and Cons of LIBOR

Let us look at the uses, advantages and disadvantages of LIBOR, before we understand its stance in Australia:

The post-LIBOR world in Australia

The LIBOR is due to be phased out/ decommissioned by the end of 2021. Post the 2008-2009 global financial crisis, authorities in the US and UK found that traders had been manipulating LIBOR to make a profit, implying billions of dollars in fines for many banks.

Discussions of its discontinuation began thereafter, and it has been noticeably accepted that replacing it and transitioning to several alternative reference rates would be both challenging and expensive.

In the 2019 ISDA Annual Australia Conference in Sydney, Assistant Governor (Financial Markets), Reserve Bank of Australia, Christopher Kent stated that the discontinuation of LIBOR is not a threat to the Australian financial system, but depicts a lack of preparedness for the phases to come, which could potentially create mayhem in the country.

A shift of new contract to different reference rates, sounds fallback provisions into existing arrangements has been the need of the hour, and instiutions who have not adhered to it would face challenges.

LIBOR impacts the financial system on the whole and Australian financial institutions are exposed significantly to contracts that reference LIBOR.? Even though Australian banks have been making positive changes in the Royal Commission era, however, the country does not seem to be fully prepped, especially the smaller institutions.

With the phasing out period just around the corner and to ease the situation, the central bank (RBA) has been thriving to strengthen alternative benchmarks, like the Bank Bill Swap Rate (BBSW) to provide ample liquidity.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.