Wall Street has a short memory. Just a couple of years ago, SPACs were synonymous with hype, lawsuits, and bankruptcies.

Investors lost billions as early-stage companies rushed onto public markets through these blank-check vehicles, only to collapse within months.

But in 2025, SPACs are staging a comeback. New listings are rising fast, big names are returning, and retail chatter is picking up again.

This time, the cast of characters is slightly different, but the pitch is the same: a fast-track to the public markets with less red tape and more upside.

The recent SPAC resurgence has a reason behind it and investors are wondering if they should be preparing for another rodeo.

What actually happened last time?

SPACs are “Special Purpose Acquisition Companies.” These are essentially shell companies that raise money through an IPO and then look for a promising private company to acquire or merge with.

These vehicles had their breakout moment during the Covid-19 bull market. In 2020 and 2021 alone, 860 SPACs went public in the US, raising more than $250 billion.

That was 62% of all IPOs during that period.

The structure appealed to private companies as a quicker, cheaper alternative to traditional IPOs. But the boom spiraled out of control.

Retail investors piled into pre-revenue electric vehicle startups, space companies, and speculative tech plays. Forecasts were exaggerated. Valuations were inflated. And due diligence was rushed.

The result was a bloodbath. By late 2023, more than 21 SPAC-backed companies had gone bankrupt, wiping out over $46 billion in equity value.

High-profile failures like Lordstown Motors, Proterra, WeWork, and Bird Global turned investor excitement into skepticism.

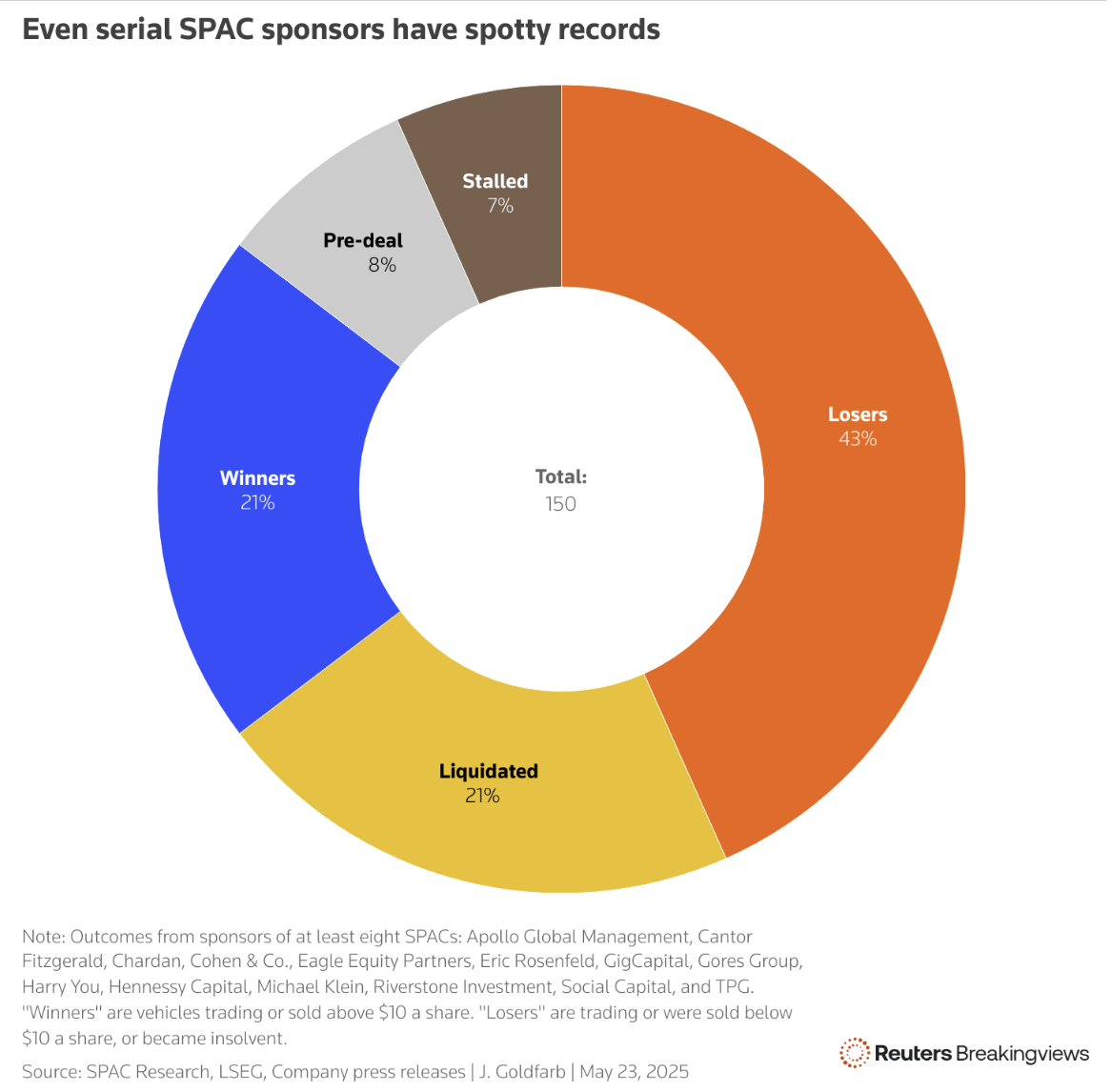

According to Bloomberg data, over 90% of SPACs that completed mergers and remained listed by 2024 were trading below the $10 IPO price. Many fell more than 75%.

Even sponsors lost money. Each failed SPAC cost backers about $8 million in underwriter and legal fees.

Estimates from finance professor Jay Ritter placed the total losses for sponsors between $4 and $5 billion.

More than half of all SPACs launched during the boom failed to find a target and had to return capital to shareholders.

Why are SPACs back now?

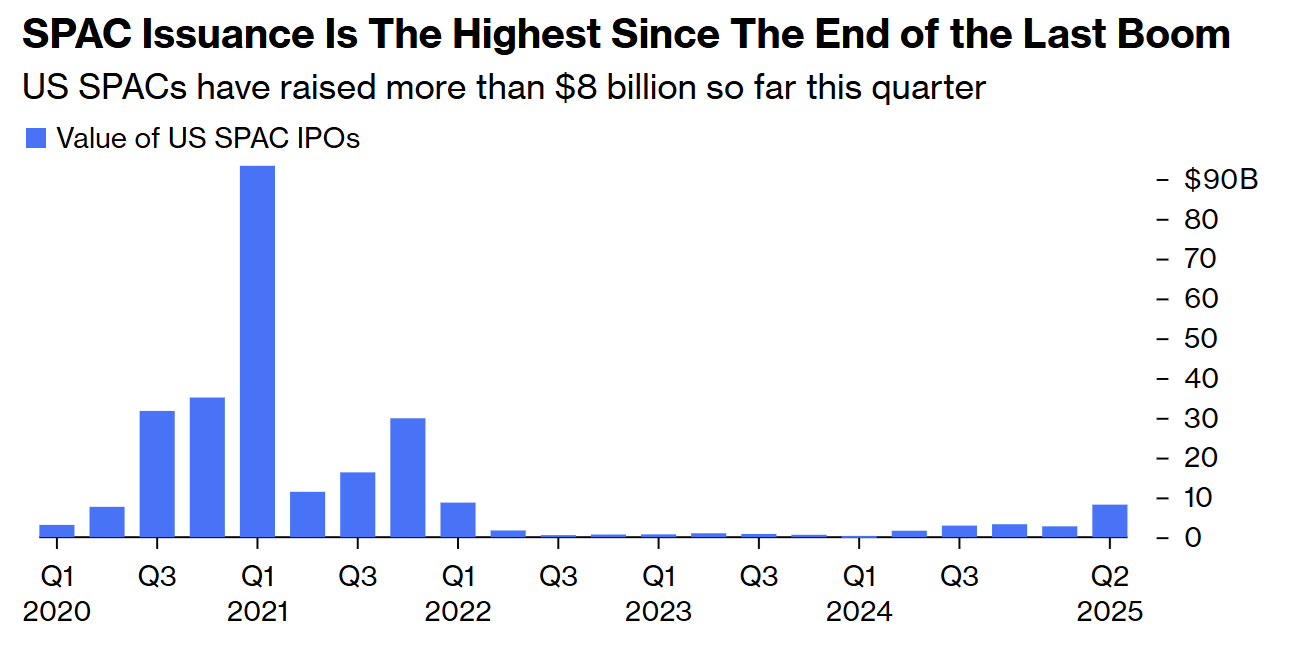

In 2025, the SPAC market is heating up again. Through mid-year, US SPACs have raised $11 billion, compared to just $2 billion during the same period in 2024.

So far, SPACs make up about 65% of all IPO volume this year and more than 40% of total proceeds, according to SPAC Analytics.

Part of the resurgence is political. With Donald Trump back in the White House, regulatory pressure has softened.

The SEC’s new chair, Paul Atkins, is widely expected to be more business-friendly than his predecessor, Gary Gensler.

During Gensler’s tenure, the SEC imposed new rules on forward-looking statements and disclosures.

While those reforms remain in place, enforcement has slowed and market participants feel the tone has shifted.

Another factor is Wall Street’s appetite for alternatives. The IPO pipeline remains thin. M&A is sluggish. And investors are sitting on record levels of dry powder.

In that vacuum, SPACs offer an appealing mix of flexibility and potential upside. Sponsors are again pitching themselves as agile dealmakers who can take advantage of public market inefficiencies.

Big names are coming back too. Michael Klein has filed for a new Churchill Capital SPAC.

Alec Gores and Betsy Cohen have re-entered the scene. Cantor Fitzgerald, now chaired by Howard Lutnick’s son, is underwriting deals again.

Chamath Palihapitiya is considering a return despite many of his earlier SPACs imploding. Thankfully, his own followers are against the idea.

Who’s actually driving this revival?

The new wave is being led by smaller players. Boutique banks like Cohen & Co, D Boral Capital, Clear Street, and Maxim Group have taken over from the big firms that dominated in 2021.

With giants like Citigroup and Credit Suisse stepping away after regulatory crackdowns, these lesser-known firms have filled the vacuum.

Cohen & Co now leads the market in both SPAC IPOs and completed mergers. D Boral Capital, formerly EF Hutton, handled the SPAC that took Trump’s Truth Social public.

Meanwhile, Cantor Fitzgerald has led a dozen SPAC IPOs this year, making it the most active bookrunner in the space.

Sponsors are again betting on hype-heavy sectors. In 2021, it was EVs and space. In 2025, it’s crypto, autonomous vehicles, quantum computing, and AI infrastructure.

Cantor-backed Cantor Equity Partners merged with Bitcoin fund Twenty One Capital and its shares tripled.

Crypto influencer Anthony Pompliano is also preparing to go public via SPAC with a Bitcoin-focused fund.

One particularly striking deal involves Colombier Acquisition Corp II, an “anti-woke” SPAC backed by Omeed Malik. It’s merging with online gun retailer GrabAGun, whose revenue shrank last year.

Donald Trump Jr. has joined the board. The sponsor paid a little over $5 million and is set to receive equity and warrants worth around $76 million. Shares are now trading 35% above trust value.

Have the incentives changed?

Not really. While some sponsors are offering better terms, the core structure still rewards insiders regardless of long-term performance.

Sponsors typically receive 20% of the equity (“the promote”) at a steep discount. In most cases, they profit even when investors lose money.

Redemptions are still sky-high. According to Bloomberg, around 95% of the capital raised in SPACs this year has been redeemed before deals close.

That forces sponsors to secure PIPE financing or restructure terms. Some deals succeed, but many are left scrambling to plug funding gaps.

There are signs of improvement. Sponsors are being more cautious about financial forecasts. Banker fees are trending lower. And PIPE investments are slowly returning.

But these are marginal shifts. The fundamental issues such as misaligned incentives, speculative dealmaking, and weak post-merger performance, are all still there.

Is this revival built to last?

Right now, the SPAC market is running on lower expectations and selective success stories. There’s less frenzy than 2021, and fewer participants chasing deals.

The smaller field has reduced competition, giving experienced sponsors more leverage. Investors are buying into the idea that this time might be different.

But the numbers suggest otherwise. Of the roughly 20 companies that have gone public via SPAC this year, Bloomberg calculates the median performance to be down about 75% from the $10 IPO price.

And most are still pre-revenue or highly speculative.

Sponsors need excitement to get deals done. They’re chasing sectors like crypto and AI not because they’re proven, but because they’re marketable.

Historically, SPACs can also be seen as bad and not worthwhile investments. In fact, since 2022, the SPAC index has gained 14.4%, while the broad S&P 500 index rose 40.7% within that timeframe.

Read next: Why the economy and stock market feel strong, weak, and broken all at once

As long as redemptions remain high and public company fundamentals stay weak, the core flaw of the model hasn’t been addressed.

If SPACs start targeting mature, cash-generating businesses, this cycle might deliver better outcomes.

But for now, SPACs remain a structural loophole, not a product that’s truly fixed. I

t seems eerily similar to a situation where persons of influence and wide audience use creative ways to make money off their followers.

Right now, most signs point to a more polished version of the last boom, not a reinvention. The structure still favors sponsors, while the risk still falls on the public.

The post Why are SPACs suddenly hot again and should investors buy into the hype? appeared first on Invezz