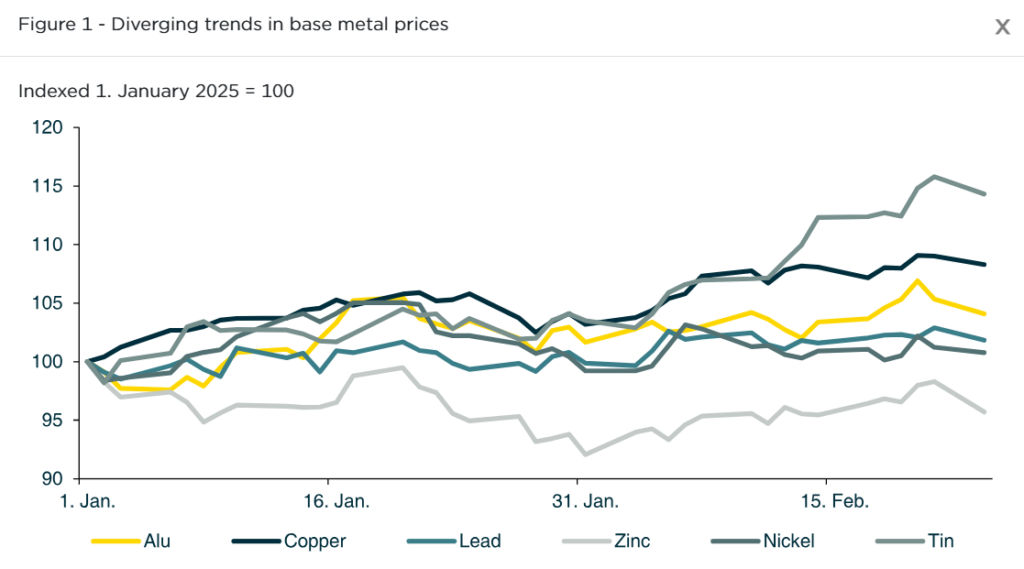

Despite the setback of the last two trading days, the London Metal Exchange (LMEX) index is trading 6.5% higher than at the start of the year, even though the base metals markets are not performing exceptionally well.

However, the stark difference in metal prices is noteworthy.

Zinc, the biggest loser in the LME complex, is currently trading 4.8% lower than at the start of the year.

Meanwhile, tin prices have increased by 13.5% in the first few weeks of the year, making it the biggest winner.

Copper market in 2025

The copper market experienced a notable surplus in 2024.

This oversupply was attributed to increased production from major copper-producing countries, a slowdown in global economic growth, and weaker-than-expected demand from key consuming sectors such as construction and manufacturing.

The resulting glut of copper in the market led to a decline in copper prices, which negatively impacted the profitability of copper mining companies and other stakeholders in the copper supply chain.

A good 300,000 tons more copper were produced than consumed.

The International Copper Study Group’s autumn forecast had predicted a higher oversupply.

The ICSG’s late-September forecast indicated a surplus of just under 470,000 tons.

The 2.9% increase in global demand was a welcome surprise, exceeding the initial forecast of 2.2%.

Barbara Lambrecht, commodity analyst at Commerzbank AG, said:

The main reason for this was stronger demand from China.

On the supply side, copper refining grew as expected at 4.2%, but mine production surprised at 2.3%, 0.5% higher than the ICSG September forecast.

The supply of refined copper is under threat due to mine production, which has put downward pressure on processing fees in copper smelters, according to Commerzbank.

“Against this backdrop, the ICSG expects weaker growth in copper production this year, which should reduce the supply surplus on the market. This should support the copper price,” Lambrecht said.

Undersupply in zinc market

According to an International Lead and Zinc Study Group’s (ILZS) report, the zinc market supply deficit was 62,000 tons last year, 100,000 tons lower than expected in autumn.

The global refined zinc supply decreased by 2.6% due to a 2.8% fall in global mine supply and the resulting lower supply of zinc concentrate.

China’s zinc production decreased by 3.4%, corresponding to a 13% fall in zinc concentrate imports, according to ILZS figures.

China is responsible for half of the global refined zinc production.

The market moved into a deficit despite stagnant demand. However, the ILZSG anticipates an oversupply this year.

Lambrecht added:

Against this backdrop, the zinc price, which recorded the second strongest rise among the LME metals last year after tin with an increase of 12%, is likely to remain the worst performer in terms of the expected price trends this year.

Lead market

In contrast, the lead market experienced a minor oversupply due to a substantial increase in mine production.

This increase, just under 2%, was fueled by significantly higher supply in the US, Australia, Peru, and Mexico.

“Nevertheless, lead output declined due to major production losses in China and Canada,” Lambrecht said.

“It should be noted that secondary production (recycling) now accounts for 67.5% of total production, meaning that the development of mine supply is of lesser importance for the lead market.”

The surplus supply in the market was recorded at 36,000 tons, significantly lower than the 153,000 tons surplus of the previous year.

This occurred as global demand for lead saw a slight decline, mirroring the trend seen in 2023, according to Commerzbank.

The post LME market shows mixed signals as copper and lead surpluses narrow appeared first on Invezz