Mergers and Acquisitions (M&A) and Takeovers are means of consolidation of companies with an objective of wealth maximisation, they have long been a part of the business world and can be termed as an important phenomenon for the competitive and effective functioning of the business. They result in the achievement of efficiencies, a decline of rivalry in the market and diversification of risks and portfolios, and make sure that the firms are on track to achieve their objectives.

Mergers and Acquisitions is basically an alliance or amalgamation of companies or assets via a financial transaction. Here we are going to discuss two companies, Coca Cola HBC AG and Charles Taylor PLC, who are in mid of some Mergers and Acquisition or Takeover deals.

Coca Cola HBC AG

Switzerland based Coca Cola HBC AG (CCH) is engaged in the business of production and distribution of non-alcoholic beverages. The company is a bottler of Coca Cola products. The company distributes Coca-Cola, Coca-Cola Zero, Coca-Cola Light, Fanta, and Sprite as well as water, energy drinks and juice.

On 13th November 2019, the company will announce the Q3 FY19 trading update.

Recent News

On 18th September 2019, the company entered into an arrangement for the acquisition of Acque Minerali S.r.l, also known as Lurisia or Acque Minerali, it is a privately held adult sparkling beverages and natural mineral water business in Italy. This acquisition is made with the Coca-Cola HBC's with the fully owned subsidiary, Coca-Cola HBC Italia S.r.l. This acquisition is in-line with the principle of similar acquisitions that were done earlier, and it is being made in conjunction with the company (Coca Cola). The selling stockholders are the private equity fund, IDeA Taste of Italy, operated by Eataly Distribuzione S.r.l and DeA Capital Alternative Funds SGR S.r.l. â¬88 million is the enterprise value to be paid by the Coca-Cola group and Coca-Cola HBC. The feat of this acquisition is subject to specific conditions and is anticipated by the end of the year. As through the course of transaction, both Alessandro Invernizzi and Piero Bagnasco, as a CEO of Lurisia will continue as directors on the board. This acquisition of Lurisia harmonizes the current Coca-Cola HBC beverage portfolio in Italy, and it is a solid fit for the group's twenty-four by seven total beverage partner plan. It also endorses the group's push to additional preimmunise its portfolio and well-positioned Italian origins and present customers a genuine Italian brand with a robust legacy.

On 28th August 2019, the company announced, in accordance with stockholder consent it obtained consent at the AGM (Annual General Meeting) of CCH held on 18th June 2019 for the cancellation of treasury shares.

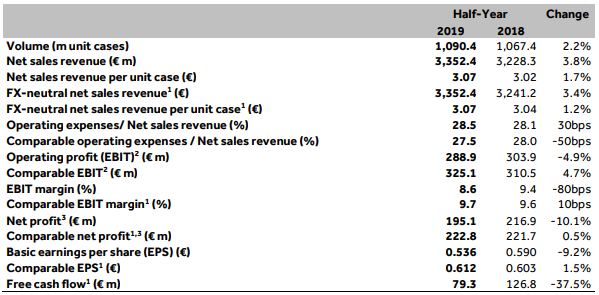

Financial Highlights (H1 FY2019, ⬠million)

(Source: Interim Report, Company Website)

During H1 FY19, net revenue surged by 3.8% (actual basis) to â¬3,352.4 million and by 3.4% on a constant currency basis. The revenue increased because of the favourable currency movements in the Nigerian Naira and Swiss Franc. The company reported volume growth of 2.2% with improvement in all the segments led by Sparkling beverages. Comparable EBIT for H1 FY19 surged by 4.7% to â¬325.1 million and comparable EBIT margin improved marginally by 10 bps to 9.7%, driven by decent volume and revenue growth and 30 bps cut in the operating expenses as a percentage of revenue. Comparable Net profit surged by 0.5% to â¬222.8 million. In H1 FY19, Comparable reported earnings per share stood at â¬0.612 and posted an increase of 1.5% as compared with the corresponding period of the previous year.

In the first half of 2019, free cash flow reduced by 37.5% to â¬79.3 million against the same period in 2018, due to reduced cash from operating activities and with increased capital expenditure. The Board has approved a dividend per share of â¬0.54 cents in H1 FY2019.

The shareholders of the company approved a dividend per share distribution of â¬0.57 cents, as well as a special dividend per share of â¬2 at the AGM (Annual General Meeting) held on 18th June 2019.

Outlook

In the H2 FY2019 period, revenue growth will expand as expected by the group against the H1 FY19 in all three divisions and particularly in Emerging markets. The company expect this increase in revenue, due to the quicker volume growth in all segments, while an increase in revenue per case on a CER basis is projected to remain at the pace of the H1 FY2019. Considering the present favourable spot rates and the hedged positions, the company believe that the adverse effect from FX movements on the P&L in the FY2019 will be around â¬20 million. This is lower by â¬30 million from the prior spot-rate determined guidance. Input costs have proceeded in line with the companyâs prospects. The company have contracts in place for most of the raw materials that they use and will assume low-single-digit growth in currency-neutral input cost per case for the FY2019. For the FY2019, the company hopes the currency-neutral basis revenue growth to be in the range of 5% to 6% and to provide one more year of margin growth.

Zoran Bogdanovic, Chief Executive Officer (CEO) of the company, said that the company had well-positioned itself in the first half of 2019. The company increased volume and revenue over all three divisions of the business and provided an additional increase in comparable margins. Revenue progress management and innovation remained firm in delivering results. Innovation drove volume rise of 4.5pp in the first half of 2019. The company is making progress in some of the most crucial categories containing Water, Energy, and Sparkling. By the year 2020, the company is progressing with the plans to introduce Costa Coffee in 10 of its markets.

Share Price Performance

Daily Chart as at September-19-19, before the market close (Source: Thomson Reuters)

On September 19, 2019, at the time of writing (before the market close, at 3:30 PM GMT), Coca Cola HBC AG shares were trading at GBX 2,691, up by 0.75 per cent against the previous day closing price. Stock's 52 weeks High and Low are GBX 2,950/GBX 2,094.19. Stockâs average traded volume for 5 days was 660,125.00; 30 days â 580,824.60 and 90 days â 760,032.54. The average traded volume for 5 days was up by 13.65 per cent as compared to 30 days average traded volume. The companyâs stock beta was 0.75, reflecting the lower volatility as compared to the benchmark index. The outstanding market capitalisation was around £9.72 billion, with a dividend yield of 1.91%.

Charles Taylor PLC

Charles Taylor PLC (CTR) offers insurance management services to mutual insurance associations and captive insurance companies. The operations of the group are differentiated in four operating divisions: adjusting services business, owned insurance companyâs business, management services business, and insurance support services business. The companyâs services are spread in more than 30 countries in the Americas, the UK, the Middle East, Asia Pacific, Europe, and Africa. The groupâs subsidiaries comprise Charles Taylor (China) Limited and Charles Taylor (Dallas) Limited.

Recent News (as on 19th September 2019)

The company had agreed to a takeover of £261 million by a firm supported by private equity company, Lovell Minnick Partners. The company (Lovell Minnick), had proposed a cash per share of 315 pence.

Charles Taylor PLC directors said the proposal, which signifies a premium of 34 per cent to the groupâs share close on 18th September 2019, is âreasonable and fairâ.

Charles Taylor PLC Chairman, Edward Creasy expressed the boardâs confidence in the longstanding opportunities and quality of the group and said that the proposal considers these factors and represents a decent prospect for stockholders to comprehend value for their investment at a tempting premium. With the support of Lovell Minnick's, the Chairman believes that the company will keep on adding on the prospects in its markets and can assure the upcoming success of Charles Taylor PLC for partners, customers and employees.

The companyâs stockholders will receive an earlier declared interim 2019 dividend per share of 3.65 pence to be paid on 8th November 2019.

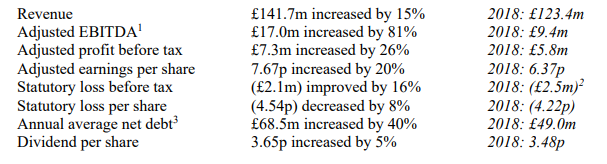

Financial Highlights (H1 FY2019, £ million)

(Source: Interim Report, Company Website)

In the first half of 2019, the companyâs revenue increased by 15 per cent to £141.7 million as compared with the first-half 2018 of £123.4 million. Adjusted EBITDA stood at £17 million, an increase of 81 per cent against the same period in 2018. The robust growth in adjusted profits before tax to £7.3 million against the £5.8 million in H1 FY18, was not reflected in the statutory profits before tax, which unfortunately shows a loss of £2.1 million. Adjusted earnings per share rose by 20 per cent to 7.67 pence as compared with the first half of 2018 of 6.37 pence. Statutory loss per share stood at 4.54 pence, a decrease from the statutory loss per share of 4.22 pence in H1 FY18. The Board proposed an interim dividend per share of 3.65 pence, an increase of 5 per cent against the 3.48 pence in H1 FY2018. Annual average net debt, which best reflects the companyâs borrowing levels stood at £68.5 million as compared to £39.5 million in H1 FY18.

Outlook

The company extended its claims services with acquired and organic development in loss adapting together with bringing the groupâs claims managing activities into a joined-up enterprise, which is adding new business. The company is persistently delivering sustainable and reliable insurance management revenues from main long-term customers. The company also completed the planned review of the group managing agency resultant in the sale of the firm, subject to regulatory approval. The company is achieving scale for the company insureTech across an increased international footprint. The company gained additional business from customers in Latin America and Europe and improved its recurring revenues. The business result was very near to break-even. The company also made excellent advancement on integrating prior acquisitions.

In the coming time, the business operations of the company might get impacted due to the challenging economic environment and macro-economic uncertainty due to Brexit. The companyâs performance was in line with market expectations. The claim services provide further growth in the loss adjusting capability and the potential for growth from new claims programme management contracts. In the short-term, the company anticipate a small moderation in current margin progress, due to the integration of FGR. The companyâs Insurance Management segment has longstanding, mutually beneficial customer relationships and the potential for stable growth. The company InsureTech business had won a major contract. This business provides the potential for robust revenue growth, due to the Inworx acquisition flow through and the benefits of the recent contract win.

Share Price Performance

Daily Chart as at September-19-19, before the market close (Source: Thomson Reuters)

On September 19, 2019, at the time of writing (before the market close, at 3:30 PM GMT), Charles Taylor PLC shares were trading at GBX 325.26, up by 38.41 per cent against the previous day closing price. Stock's has touched its fresh 52 weeks High, and its 52 weeks Low was GBX 184.25. Stockâs average traded volume for 5 days was 16,525.40; 30 days â 27,310.30 and 90 days â 35,120.48. The average traded volume for 5 days was down by 39.49 per cent as compared to 30 days average traded volume. The companyâs stock beta was 1.03, reflecting almost the same volatility as compared to the benchmark index. The outstanding market capitalisation was around £183.57 million, with a dividend yield of 4.99%.

Â