Unilever PLC (ULVR) is a London based multinational producer and marketer of fast-moving consumer goods (FMCGs) such as food, beverages, home care, health and wellbeing products. The company operates through more than 400 brands - including Knorr, Hellmann's, Lipton, Wall's, Lux, Dove, Rexona, Surf Excel, Comfort, Sunsilk, Pureit, Suave and Axe - across the Americas, Europe, Asia-Pacific, Africa and the Middle East region. Its distribution channels include supermarkets, hypermarkets, wholesalers, cash and carry, small convenience stores, e-commerce, out-of-home and direct consumer channels. The company has pledged to reduce its carbon footprint extensively by 2030 and was ranked number one in its sector as per Dow Jones Sustainability Index 2017.

The company has differentiated its operations in three operating segments: Beauty & Personal Care, Home Care and, Foods & Refreshment. The company also provide additional information based on geographies: The Americas, Europe, and Asia/AMET/RUB, which includes Asia, Africa, Middle East, Turkey, Russia, Ukraine and Belarus. The company employs 161,000 personnel. It has two home countries: the Netherlands and the United Kingdom. In January 2019, Alan Jope was appointed as Chief Executive Officer of the group.

Amid various challenges faced by the company, its chief executive Alan Jope, in his first interview since taking the top job, offered hope that the company will next year escape a period of stagnant sales and will be successful in reversing four years of slowing sales growth. The maker of Dove soaps and Magnum ice creams, which is one of the world's largest consumer goods groups, has faced challenges ranging from millennials ditching well-established brands to the growing popularity of new trends such as veganism. The 54-year-old Scot, who succeeded Paul Polman for the top job at the £140 billion Anglo-Dutch group, signalled that the company would shift its focus to the higher-margin beauty and personal care market from food.

While analysts are expecting Unilever's underlying sales growth to pick up to 3.4 per cent this year from 2.9 per cent in 2018, the CEO sounded optimistic and set the guidance in the 3 to 4 per cent range, hoping to edge up from next year onwards. He also said that he doesn't feel a sense of pressure externally, though he was working with a sense of urgency. Mr Jope is a veteran employee and faces an uphill battle to deliver on his promise to accelerate growth. He is one new leader who has been handed the task of reviving a major consumer goods company, and his past stints include running operations in India and China. In a bid to reignite growth, management in many companies has been overhauled, including Colgate-Palmolive, PepsiCo, Kraft-Heinz. From the 6-8 per cent growth which the companies enjoyed a decade ago, annual sales growth has fallen to just 2-3 per cent across much of the industry.

Alan Jope said that as a rapidly growing population and an emerging middle class rapidly consume the company's household good products, countries like Vietnam, Bangladesh, Pakistan and Myanmar will be the top growth markets for consumer goods giant over the next few years. Emerging markets including China, India and Brazil already account for 58 per cent of its sales and the company is investing heavily in other growth stars over the next few years.

Since 2015, the Unilever has focused its acquisitions on skincare and cosmetics products, while disposing off assets in slower-growing categories of food such as spreads and margarines. Over the periods, the company has sold â¬8 billion of assets, mainly in the food category, and almost three-quarter of the â¬11 billion it has spent on 30 deals were focused on beauty and personal care division. Mr Hope said that the company would continue to dispose of assets that are intrinsically slower growth and would emphasise on acquiring in beauty and personal care, without disposing much. Unilever has been snapping up niche labels under the new Chief Executive Officer.

Though start-ups producing plant-based meats, such as Beyond Meat, have fascinated the stock market this year, Mr Jope was clear that the elusive recovery in sales growth would not come from investing much in start-ups. While he admitted that plant-eating had become a megatrend, the company should stay away from acquisitions, especially when crazy valuations are involved, and should stay put on its strategy. He reported that the company was playing more selectively on food assets and very aggressively on high-quality, fast-growing beauty and personal care assets. Last year, in what Mr Jope described as an "experimental foray", the company bought a small Dutch brand called Vegetarian Butcher.

Mr Jope's message on sales growth is likely to be welcomed by investors and he is treading a fine line as he seeks to speed up growth. He continues to retain his predecessor Paul Polman's ambitious operating margin target of 20 per cent by 2020, which was made after the aborted Kraft-Heinz takeover bid in 2017, causing Unilever to embark on deep cost cuts. Investors have questioned his decision to stick with the target, as dropping it would give Unilever more room to invest in the business. While Mr Jope insisted that its push for faster sales growth would not be sacrificed for the 20 per cent margin goal, many chiefs at big consumer companies have introduced so-called margin resets in recent months as they seek to invest in flagging brands. Along with the cannily tweaked message to emphasise how having purpose-led brands that stand for ideals, defending the margin goal is one of several signs that the new tenure of Mr Jope has begun with a strategy in line with the Polman era.

Instead of a bigger transformative acquisition, the company's strategy of doing lots of relatively small deals had so far served it well, but any large spin-offs or acquisitions using stock would be harder due to the complex structure of the group. With a UK-listed plc and Dutch-listed NV corporate entity, Mr Jope may have to return to the thorny issue of simplifying the corporate structure of the group. He said that moving to a single corporate entity with one stock listing would make such moves easier and the company is actively working on multiple scenarios and looking at the legal, financial, and reputational implications of each of them.

In the latest first-quarter update, the company reported underlying Sales Growth of 3.1%, driven by the emerging market's underlying sales growth, which climbed by 5%. Volume/mix was ahead 1.2%, and pricing was ahead 1.9%. The company characterised the quarter as a 'solid' start, with accelerating growth and expects to be on track for full-year expectations.

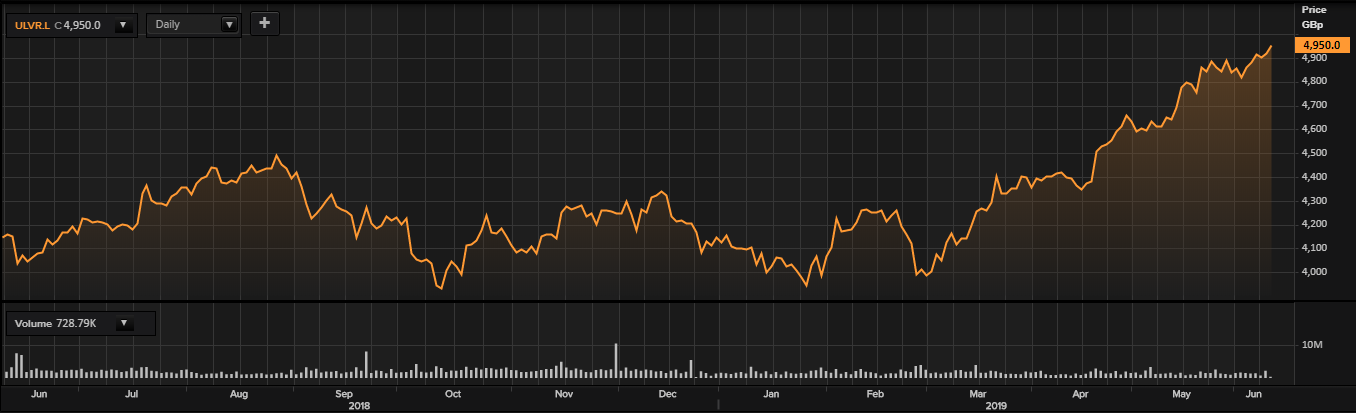

Share Price Commentary

Daily Chart as at June-12-19, before the market closed (Source: Thomson Reuters)

Â

On June 12, 2019, at the time of writing (before the market closed, at 02:15 pm GMT), ULVR shares were trading at GBX 4,950, up by 0.65 per cent against the previous day closing price. Stock's 52 weeks High and Low is GBX 4,983.00/GBX 3,904.94. On the valuation front, the stock was trading at a trailing twelve months PE multiple of 23.0x, against the industry's median of 10.8x. The company's stock beta was 0.88, reflecting less volatility as compared to the benchmark index. The outstanding market capitalisation was around £139.97 billion, with a dividend yield of 2.79 per cent.