US Markets: American equities bounced back on Monday, 29 November, partly recovering from the Black Friday’s slump as investors seemingly overturned the fears of Omicron variant of Covid-19 (SARS-CoV-2) virus. All the three Wall Street indices started on a positive footing with the tech leader Nasdaq Composite advancing the most as technology shares led the recovery.

Shares of microblogging and social networking giant Twitter surged a little more than 11% on Monday amid reports of CEO Jack Dorsey stepping down from the position of CEO. The gains were short-lived as the stock dived into the negative region, touching a day’s low at $46.82, marginally lower from the previous close of $47.07.

With a number of countries increasing the border control measures amid the increasing cases linked to the Omicron virus variant, the enterprises operating within the hospitality industry, aviation businesses, travel operators, consumer facing corporations and other leisure businesses are likely to be affected in the upcoming weeks if the healthcare authorities fail to contain the spread of virus.

US Markets Positive | Omicron Fears Ease | Top Global Stories to Know

As the vaccine makers and the biotechnology firms examine the new virus strain and the prospective response of existing vaccines, the remedial action with the maximum possible effectiveness may take time. While vaccine scientists and specialists study the virus, a bunch of countries have restricted international travel from the South African region.

The Dow Jones Industrial Average slipped in the wee hours of trading, while Nasdaq Composite strengthened. Dow Industrials added 103.55 points, or 0.30 to 35,002.89, Nasdaq Composite surged 221.99 points, or 1.43% to 15,713.64, whereas the broader share indicator S&P 500 rose 44.37 points, or 0.97% to 4,638.99.

US Market News: Amid the blue-chip components of Dow Industrials, shares of Salesforce, IBM, Microsoft, Apple, UnitedHealth Group, Home Depot, Nike, Cisco Systems, Coca Cola, Amgen, P&G and Chevron rose 1-3%, providing the major positive points to the index. While, on the other hand, the heavyweight stock of Merck & Co, Walt Disney, Caterpillar, Dow, Goldman Sachs, Walmart, Boeing and JPMorgan Chase collapsed between 1% and 5%.

The shares trading in the negative territory weighed on the market index, partially offsetting the positive push provided shares oscillating in the green.

A sharp upswing in the large-cap technology shares including Apple, Microsoft, Amazon, Tesla, Facebook, Alphabet, Nvidia, ASML, Adobe Systems, Costco Wholesale, Cisco Systems, Pepsico, Qualcomm, Advanced Micro Devices, Moderna and Intuit considerably supported the tech heavy index as these gained. The stock of Moderna emerged as the biggest gainer amid the 100 components of Nasdaq.

The index gains were slightly counterbalanced with the drop in shares of Peloton Interactive, NetEase, Zoom Video Communications, eBay, T Mobile US, Fiserv, Baidu, Trip.com Group, Biogen, JD.com, MercadoLibre and Paypal.

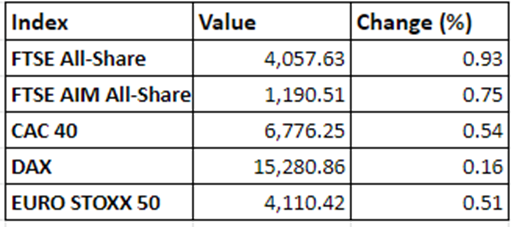

UK Markets: London shares staged a meaningful comeback in the session on Monday with the domestic benchmark FTSE 100 retaking the psychological level of 7,100. The index pared the gains in the terminal trades. The index registered an intraday peak of 7,161.91. Meanwhile, the consumer credit in the UK jumped by GBP 0.706 billion in October as Britons borrowed GBP 0.6 billion in the form of credit card debt. This has been the strongest net borrowing since July of 2020.

According to the Bank of England data, the individual borrowing including the personal loans and car finances translated into GBP 0.1 billion of net lending in the corresponding period. The headline FTSE 100 gained 65.92 points, or 0.94% to finish at 7,109.95. The mid-cap heavy index FTSE 250 advanced on similar lines with the market index rising 218.44 points, 0.97% to 22,756.33.

FTSE 100 (29 November)

Source: EODHD/Others

Market Snapshot

Top 3 volume leaders: Lloyds Banking Group, International Consolidated Airlines and BP

Top 3 sectoral indices: Consumer Services, Automotive and Fossil Fuels

Bottom 3 sectoral indices: Personal Care, Precious Metals and Precious Metals

Crude oil prices: Brent crude up 3.63% at $74.19/barrel; US WTI crude up 4.23% at $71.03/barrel

Gold prices: An ounce of gold traded at $1,785.85, down 0.13%

Exchange rate: GBP vs USD - 1.3293, down 0.35% | GBP vs EUR - 1.1803, up 0.17%

Bond yields: US 10-Year Treasury yield - 1.514% | UK 10-Year Government Bond yield - 0.8575%

Markets @ 16:35 GMT