US Markets: All the three stock averages of Wall Street extended the gains on Tuesday, 7 November, with the technology heavy Nasdaq Composite advancing 3%, Dow Industrials gaining more than 500 points, and the broader S&P 500 rising a little over 2%. The market-wide buying has propelled the leading indices on track to finish in the positive territory this week, may close to their respective record highs.

As the equities recover lost ground, investors are seemingly in a hurry to accumulate shares on dips as Nasdaq Composite and Dow Jones are still oscillating 1.8-2.4% lower as compared to the recently acclaimed all-time highs. On the other hand, the S&P 500 has narrowed the gap between the record high as the index recorded an intraday peak of 4,690.50 on Tuesday, it had made a record high of 4,743.83 in the second half of November 2021 itself.

The indices have partly retraced all the losses incurred due to the heightened worries following the emergence of Omicron variant of Covid-19 (SARS-CoV-2) virus. As the fears surrounding the extent of damage due to new strain of virus alleviate, market participants have regathered the lost optimism as other material drivers for the equities remain largely unchanged, barring some.

With the anticipation of increased consumption in the run up to the Christmas festivities and the year-ender break, the consumer spending is likely to increase in the upcoming weeks, effectively benefiting the enterprises as they try to make the most of the busiest trading period of the year.

The trade deficit of the United States shrinking to $67.1 billion in the month of October also complemented the recovery as the Washington administration managed to decrease it from the record high shortfall of $81.4 billion in September of 2021. Resilient volumes of exports from the US to European, as well as Asian countries productively supported the balance of trade as the country reported the lowest trade deficit in the last six months.

In October of 2021, the exports from the US surged 8.1% to a record high of $223.6 billion, largely driven by the shipments of crude oil, automobiles, non-monetary gold, industrial machineries, diamonds, civilian aircraft and soybeans, the data from Bureau of Economic Analysis showed. Interestingly, the trade slippage with the EU region also narrowed to $16.6 billion, witnessing a drop of $2.1 billion.

The Dow Jones Industrial Average rose 579.25 points, or 1.64% to 35,806.28, the tech leader Nasdaq Composite rallied 443.12 points, or 2.91% to 15,668.27, whereas the wider share indicator S&P 500 surged 97.79 points, or 2.13% to 4,689.46.

US Market News: Shares of American Express, Salesforce.com, Intel, Apple, Microsoft, Goldman Sachs, Nike, Visa, Dow, Chevron, Caterpillar, Boeing, JPMorgan Chase, McDonald’s, IBM and UnitedHealth Group gained 1-5%, contributing majorly towards the upsurge in the Dow Industrials. Shares of Merck & Co and Verizon were the only two shares amid the 30-component heavy Dow Jones that slipped more than 1% each.

Shares of Intel soared as much as 7.86% in the wee hours of trading as the company plans to launch the initial public offering (IPO) of its subsidiary Mobileye in the United States by the middle of 2022.

Amid the Nasdaq Components, shares of Apple, Microsoft, Amazon, Tesla, Alphabet, Facebook, Nvidia, ASML, Adobe Systems and Netflix emerged as the major heavyweight gainers, supporting the tech leader by rising 1-6%. The stock of Pinduoduo moved up sharply as it amassed a gain of more than 13%, emerging as the biggest gainer on Nasdaq Composite. On the other hand, shares of Comcast, Charter Communications and Sirius XM stood as the only major losers with the stocks declining 2-7%.

UK Markets: London equities surged sharply on Tuesday, with the headline market index FTSE 100 rising more than 100 points to comfortably recapture a level well above 7,300. The index came closer to the previous 52-week high as the 101-stock average is less than 1% away from the respective 52-week peak of 7,402.68.

Shares of Anglo American, BHP Group and Ferguson emerged as the biggest gainers amid the components of the index as the stock advanced 5-7%. Barring the shares of pharmaceutical majors AstraZeneca and Reckitt Benckiser, all 18 shares among the top 20 stocks by market capitalisation witnessed an appreciation.

The stock of HSBC Holdings, Diageo, GlaxoSmithKline and BP jumped more than 1% each, while the shares of Rio Tinto, Glencore and Lloyds Banking Group soared 2-5%.

On the contrary, shares of the market capitalisation leader AstraZeneca dropped more than 2%, partly offsetting the positive points provided by the aforementioned blue-chips. Other than AstraZeneca, stocks of B&M European Value Retail and Reckitt Benckiser Group were the only components that plunged over 1%. The FTSE 100 added 107.62 points, or 1.49% to 7,339.90, whereas the mid-cap barometer FTSE 250 gained 364.09 points, or 1.59% to 23,245.42.

FTSE 100 (7 December)

Source: EODHD/Others

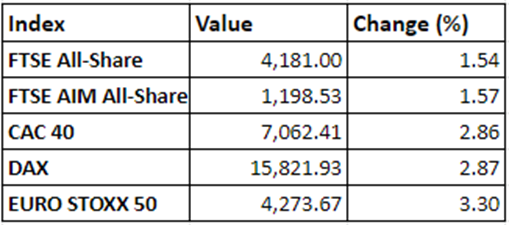

Market Snapshot

Top 3 volume leaders: Lloyds Banking Group, BT Group and Vodafone Group

Top 3 sectoral indices: Industrial Metals, Industrial Transportation and Personal Goods

Bottom 3 sectoral indices: Medicine and Biotech Sector

Crude oil prices: Brent crude up 3.65% at $75.75/barrel; US WTI crude up 4.22% at $72.42/barrel

Gold prices: An ounce of gold traded at $1,786.75, up 0.41%

Exchange rate: GBP vs USD - 1.3232, down 0.24% | GBP vs EUR - 1.1764, up 0.11%

Bond yields: US 10-Year Treasury yield - 1.444% | UK 10-Year Government Bond yield - 0.7225%

Markets @ 16:30 GMT