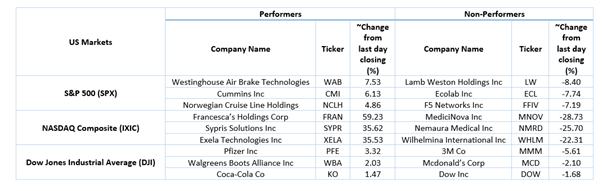

US Markets: Broader indices in the United States traded in red - particularly, the S&P 500 index traded 2.31 points or 0.07 per cent lower at 3,237.10, Dow Jones Industrial Average Index contracted by 92.21 points or 0.35 per cent lower at 26,492.56, and the technology benchmark index Nasdaq Composite traded lower at 10,497.63, down by 38.64 points or 0.37 per cent against the previous day close (at the time of writing, before the US market close at 11:56 AM ET).

US Market News: The Wall Street trended downwards over the continued debate on the stimulus package. The US Confidence index declined to 92.6 in July 2020 from 98.3 in June 2020. Among the gaining stocks, JC Penny shares surged by close to 24.0 percent after the company is reported to be bought by private equity firm Sycamore. Intel shares were up by about 0.5 percent after the company said that its Chief Engineering Officer is leaving the company. Among the decliners, Harley Davidson's shares were down by close to 5.0 percent after the company reported loss against street's consensus of profit. 3M was down by about 4.5 percent after the health-care product maker company reported earnings below market consensus. McDonald was down by close to 2.6 percent after the company reported lower restaurant sales in the quarterly earnings report.

US Stocks Performance (at the time of writing)

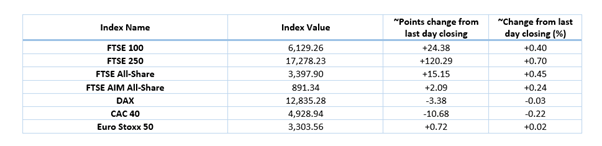

European News: London and the European market opened in green. As per the Confederation of British Industry data, the retail sales index improved to 4 in July 2020 from -37 in June 2020. Meanwhile, the National Institute of Economic and Social Research (NIESR) stated that the UK government needs to extend the furlough scheme until June 2021 to cope up with the impact of Covid-19. Among the gaining stocks, Card factory shares increased by about 5.2 percent after the company reported reopening of stores and better than expected sales. Mitie Group was up by about 2.1 percent even though the company reported a decline in annual revenue due to loss of contract. IAG was up by about 1.6 percent, although the company received strike threats over job cuts. AstraZeneca was up by close to 0.6 percent after the company reported that Farxiga, its diabetes treatment, met the last stage trial testing goal. Among the decliners, Greggs was down by close to 6.1 percent after the company reported lower sales compared to the previous year. St James Place was down by around 0.9 percent after the wealth management company reported lower operating profit.

European Indices Performance (at the time of writing)

FTSE 100 Index Chart

1 Year FTSE 100 Index Performance (28 July 2020), before the market closed (Source: EODHD/Others, Thomson Reuters)

Stocks traded with decent volume*: (LLOY) LLOYDS BANKING GROUP PLC; (VOD) VODAFONE GROUP PLC; (BARC) BARCLAYS PLC.

Sectors traded in the positive zone*: Healthcare (+1.17%), Utilities (+1.17%) and Consumer Non-Cyclicals (+0.60%).

Sectors traded in the negative zone*: Basic Materials (-1.44%); Industrials (-0.27%), and Telecommunications Services (-0.18%).

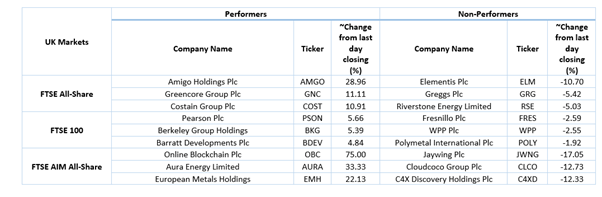

London Stock Exchange: Stocks Performance (at the time of writing)

Crude Oil Future Prices*: WTI crude oil (future) price and Brent future crude oil (future) price were hovering at $40.94 per barrel and $43.52 per barrel, respectively.

Gold Price*: Gold price was trading at USD 1,952.70 per ounce, up by 1.12% from previous day closing.

Currency Rates*: GBP to USD and EUR to GBP were hovering at 1.2946 and 0.9055, respectively.

Bond Yields*: U.S 10-Year Treasury yield and UK 10-Year Government Bond yield were trading at 0.582 per cent and 0.108 per cent, respectively.

*At the time of writing