US Service Sector Falls More Than Expected

Troubles for the American president Donald Trump seem to be emanating from all the fronts. Politically, he is battling impeachment enquiry initiated by Democrats in the House of Representatives over allegations that he sought to blackmail the President of Ukraine to pressure him into launching an investigation on Joe Biden, former Vice President and the Presidential contender for 2020, over his alleged role in ousting the former Ukrainian prosecutor. The state of the domestic economy also increasingly looks heading towards a recession, which could prove a huge blow to his chances of successfully running for the Presidential post in 2020, given his emphasis that his policies had led to the expansion that was experienced during the last few years. New data reported in the last few weeks indicate that the economy is in a fragile state.

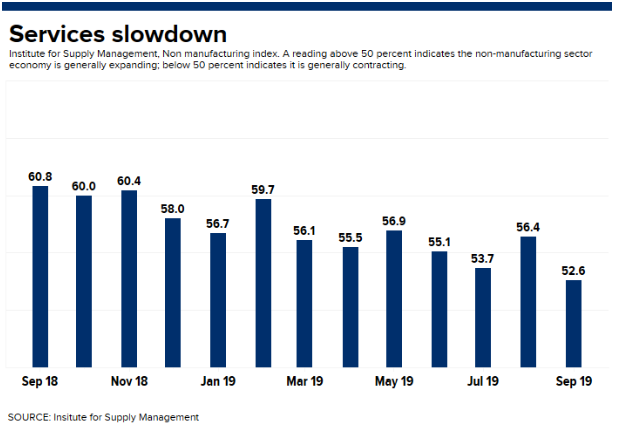

The latest blow to a recent string of weak economic data came when the Institute for Supply Management (ISM) on Thursday revealed that the US services sector grew at its slowest pace in three years during September. The index for the non-manufacturing sector fell from 56.4 in August to 52.6, triggering a rally in government bonds and a sharp sell-off for global stocks, as global risk appetite seemed to wane. It was the lowest reading for the gauge since August 2016 and indicated a slower rate of growth than the previous month, though the index remained above the threshold of 50 that separates expansion from contraction. However, it was significantly lower than the market expectations of 55.

The Institute for Supply Management said that the respondents were mostly worried about tariffs, labour resources and the direction of the economy, suggesting that the tariff war with China had started to take a toll on the business confidence. The survey showed that 13 of the services industries it tracks reported expansion but falling growth has become a big cause of fear about the US economy, especially as the service sector accounts for the most in the Gross Domestic Product (GDP) of the country. While the pace of growth in core retail sales in the US has been strong of late, investors are worried that it might not be sustainable for long, as the growth in core retail sales tends to track the headline reading, which in turn does not augur well for the broad economy as the economic growth in recent months has been driven by private consumption.

Many experts reckon that the need to devote more of income to pay for tariffed goods will impact the broad spending power of the population, which would not take much time to spiral into a full recession, the first after the 2007-08 crisis. The fear of the impact of tariffs on consumer goods on sales and margins of retailers is also indicated by the increasing gap between the rate of sales growth and the ISM index. Only modest job growth in the service sector was reported as the employment index also declined from 53.1 in August to 50.4 in September, and there was a fall in new orders index to 53.7 from 60.3 and business activity index to 55.2 from 61.5 that resulted in bigger than expected drop by the headline index. Moreover, the US services index by IHS Markit recorded its weakest figure since the same period in 2016, and new business growth slid to the lowest since data collection began in October 2009.

The Institute for Supply Management earlier had reported that factory index slipped to 47.8 in September, the lowest since June 2009 and way below the market expectations, which indicated that the manufacturing industry unexpectedly fell deeper into contraction. This extended the drop from a 14-year high recorded just over a year earlier and marked the second straight reading below 50, putting the longest-ever American expansion in a more precarious position. A slowdown in the sector in combination with subdued business investment and economic growth led to analysts imploring the spill-over of the same as weakness in the non-manufacturing survey was broad-based, even though manufacturing makes up just over a tenth of gross domestic product.

The claims by the President that Chinese are bearing the brunt of the trade war now looks set to be challenged by a large part of the society. Moreover, in the initial phase of the dispute, the US economy was going strong, and the stock market was also booming, which contrasted with the Chinese market. But now, the hand of US administration might weaken as they would seek to agree to a deal at the earliest, and if possible, before the 2020 elections. Mr Trump would like a win very soon, and the possibility of this from domestic politics looks very bleak, especially as his brazen nature, which includes suggesting China should launch an enquiry into Mr Biden, has landed him in more trouble in recent times. Lately, he has been accused of inviting foreign powers to interfere in the national elections of the country.

Investors fear that slowdown in the manufacturing sector has spilled over into the broader economy and has impacted the service side of the economy, which would lead to layoffs and market tensions that can force consumers to reduce spending. Many reckon that this is because of the trade war, which is denting confidence, disrupting supply chains and raising costs on businesses, making manufacturing in the country harder and less profitable. The market expects the Federal Reserve Bank to come to the rescue of the economy and investors are now pricing in at least one more interest rate cut before year-end, in stark contrast to the position of the central bank a year ago.

UK Service Sector Fall in Tandem with Declining Prospects

The decline in service sectors seems to have gone global as the latest survey by IHS Markit/CIPS revealed that service sector in the United Kingdom contracted last month, a blow to the administration of the prime minister Boris Johnson, who is struggling to reach a deal with the European Union before the latest deadline of 31 October. The survey showed that a growing proportion of employers had cut staff and activity slowed sharply in September, indicating that economic outlook in the country is darkening.

The seasonally adjusted IHS Markit/CIPS UK Services PMI® Business Activity Index fell from 50.6 in August to a six-month low of 49.5 in September, slipping below the no-change threshold of 50.0 which shows that a majority of companies reported decline in activity. The index had fallen below the threshold of 50.0 only thrice before the latest survey. The figure was below the market expectations and suggested that the economy shrank by 0.1 per cent in the third quarter, after a 0.2 per cent decline in the previous quarter. The all-sector PMI index in September sank to 48.8 from 49.7, as dismal surveys of the construction and manufacturing sectors were reported earlier, indicating Britain has edged closer to its first recession since the financial crisis. The all-sector index was significantly weaker than comparable measures of the eurozone and global activity, signalling the mounting stress faced by the economy as Brexit looms large. It was also reported that jobs in manufacturing and construction fell at quicker rate and UK private sector employment fell at the fastest pace since December 2009 in September.

The survey further revealed that since July 2016, following the EU referendum, companies were the least optimistic of future growth of activity as both new and outstanding business declined at the end of the third quarter. Workforces fell at 19 per cent of survey respondents, and it also reported the biggest cut in employment in over nine years, with jobs at service sector companies being cut for the first time in five months. However, as opposed to compulsory redundancies, most of the firm focused on the non-replacement of leavers. The companies reported that the postponement of orders by clients were due to heightened uncertainty around Brexit and backlogs declined at the fastest rate since January, decreasing for the twelfth successive month. New contracts fell for the sixth time in 2019, and lower volumes of both new and outstanding business reflected the overall reduction in service sector output.

The volume of new export business won by the local service providers declined at the fastest rate since March, providing evidence that global clients had switched to other markets and suppliers amid rising concerns around a potential no-deal Brexit. Though the Future Activity Index remained above 50.0, it was the second-lowest since March 2009, and the lowest since July 2016, and the survey revealed the most sustained decline in sentiment since the second half of 2015 as business expectations weakened for the fourth month running in September. The cost pressures in the latest period were slightly above the trend since 2018, as respondents blamed a range of causes, including the weakness of sterling, salaries, food, and energy/fuel.

Many experts reckon that though the country was not necessarily heading towards a technical recession, growth in the biggest part of the economy has fizzled out, suggesting a greater likelihood that the next move by the Bank of England in interest rates will be a cut. Moreover, surveys indicate that employment is now falling after the early summer had seen resilient jobs growth, driven by a lack of investment, cancelled and postponed projects and falling sales. The September survey responses were dominated by Brexit-related concerns.