_07_03_2026_03_50_21_133108.jpg)

Santander UK, a wholly owned subsidiary of the major global bank, Banco Santander is a large retail and commercial bank, actively competing with the four major banks of United Kingdom, serving through digital channels, with special concentration on mobile banking, alongside a network of branches and Corporate Business Centres, which all are aided by its fully equipped call centres.

Parent company Banco Santander S.A- A niche player in the segment

Banco Santander S.A, the Spanish parent company of the Santander UK, is a retail banking giant operating in 10 major markets, including the United Kingdom, Spain, Germany, Poland, Portugal, Chile, Argentina, the United States, Mexico, Brazil and Chile. The group also has substantial market share in the South American country Uruguay and Caribbean island of Puerto Rico. The group is into providing consumer financing businesses (CFB) in other European countries as well and holds a strong presence in China through its wholesale banking and CFB.

Santander UK actively on the growth path

By 2018, the bank was having an active customer base of 15 million with consumer loan book worth £200bn. The majority of the customer loan comprised of mortgages, covering 79 per cent (£158.0bn) of the total loan book, while 12 per cent consisted of corporate loans (£24.bn). The bank is also into accepting customer deposits and has a huge deposit base of £172bn, from 5.5 million of its digital customers. The companyâs focus on the digital channels, particularly mobile, can be gauged with the fact that it has been adding 1385 new active mobile users every day. 55 per cent of the bankâs mortgage loans were re-financed online in 2018, up from 49 per cent in 2017. The bank was having 23,800 people on its rolls and paid £445 million of corporation tax and £86 million through the UK Bank Levy in 2018.

If we talk about the financial performance for the year 2018, there was a 14 per cent decline in profit before tax, mainly because of higher risk control, regulatory costs and pressure on income due to lower new mortgage margins and Standard Variable Rate (SVR) attrition. In lending, the bank, despite the highly competitive market, posted its strongest growth during the year in mortgages in over three years and the progress in lending to non-CRE trading businesses was well ahead of the market. The bank, through its prudent approach on risk mitigation, managed to maintain strong credit quality.

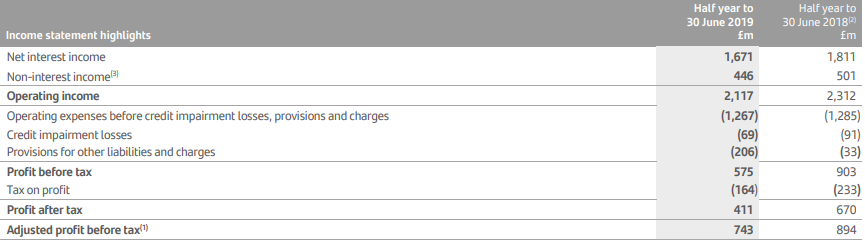

Financial Highlights for the half-year ended 30 June 2019 (£m)

(Source- Half-Yearly Financial Report 2019 of the company)

In the first half year ended 30 June 2019, the net interest income of the bank was down by 8 per cent to £1671 million as compared to £1811 million in the half-year ended 30 June 2018, mainly because of pressure from the mortgage book and £2.1bn of SVR attrition. The non-interest income was down by 11 per cent to £446 million from £501 million in the comparable half-year of 2018. The non-interest income decline was due to £63 million of ring-fencing perimeter changes in Corporate & Investment Banking (CIB), though it was partially offset by £15 million additional consideration received in connection with the 2017 shareholding sale of Vocalink Holdings Limited. Operating income of the bank declined by over 8 per cent to £2,117 million from £2,312 million reported in the half-year to 30 June 2018. Operating expenses before credit impairment losses, provisions and charges were down 1 per cent, largely due to £41 million of ring-fencing perimeter changes and £28 million of Banking Reform costs from H1 FY18, as well as £13 million of transformation costs during the current year. However operating expenses were up by 3 per cent, when adjusted for ring-fencing perimeter changes, banking reform and transformation costs. Profit before tax of the bank was down 36 per cent to £575 million, while adjusted profit before tax was down 17 percent to £743 million.

Bankâs customer and business-centric approach

Santander UK is very customer-centric bank, valuing customers suggestions and is constantly working to provide them with the best of services. It was the customersâ services demand apart from the cost parity that the bank decided to bring all its retail call centres back to the UK in 2011 from India.

In the beginning of 2018, the bank adopted a duel default rate, according to which all new customers were moved to its cheaper âFollow-on Rateâ (FoR) while existing borrowers were left with the higher SVR. The Standard Variable Rate (SVR) is a starting or the primary rate set by all individual mortgage lenders and the SVR is not knotted to the Base Rate set by the Bank of England. It is usually more than the mortgage fixed or reduced rate, based on when the deal was executed. The move has been termed a strategic one adopted by the bank to undercut its competitorsâ SVRs and allows a rather propitious affordability calculation.

Latest customer-oriented announcements by the bank

Santander UK has been firming up its digital channels and had recently proposed to offer telephone banking customers the option to verify themselves through an innovative combination of biometric âVoice IDâ technology and âPhone IDâ. Â Not only this, Santander is also going to introduce âNatural Languageâ to its banking service being operated through telephone. This means once customersâ genuineness has been established, they just have to state the purpose for their call and it gets routed directly through to the related team, removing the need to key in an option from a telephone menu, thus making the process even simpler.

Recently Santander in collaboration with eBay announced to offer loans to the more than 200,000 SMEs using eBay in the UK through its fintech app âAstoâ that will help small businesses in the UK to flourish.

Santander UK is challenging the mighty four of UKâs banking businesses through its digital transformation

The bank with its omnichannel presence is directly challenging the big four banks of the UK, Barclays; HSBC; Lloyds Banking Group; and The Royal Bank of Scotland Group. For the last two years, it has a stable 15 million active customers of which 5.5 million are digital customers; Its cost to income ratio has fallen to 56 per cent in 2018 from 51% in 2017. By the end of 2018 and is strongly capitalised with CET1 capital ratio at 13.2% from 12.2% in 2017. Â The parent group of the bank, Banco Santander has merged all its digital services into a single entity, Santander Global Platform. The main reason behind the measure is to reap EUR1 billion from efficiency gains in IT and operations and through common amenities across regions. In April this year, the bank came up with a plan to spend EUR20 billion on digital technology spread over the coming four years as part of an efficiency enhancement, aimed at pruning EUR1.2 billion in yearly costs. Santander UK on its part is aiming to be the best retail and commercial bank and has been implementing digitalisation through an emphasis on mobile experience with technological transformation, which not only allows it to work more prudently but also leads to cost savings through optimisation of different business channels. The bank has been delivering consistent profitability and a strong balance sheet, through its sustainable business model with low earnings volatility and a low-risk profile.

Outlook

The bank has been a consistent performer, though there have been headwinds and pressure on the earnings coupled with the ring-fencing perimeter changes implementation. Also, due to the impact of the competitive UK mortgage market and uncertain political times, profitability has declined. However, the bank managed to increase its mortgage lending by £1.4bn from the end of 2018 to June 2019, retaining its market share. The management is confident of better performance and has kept its outlook for the year 2019 largely unchanged based on the UKâs impending exit from the European Union. However, with an increased chance of a âno dealâ outcome in October 2019, there could be income pressure on the bank. But positives can be drawn from its digital transformation, which will make up for most of the losses in the medium term.