Summary

- Westpac-Melbourne Institute Index of Consumer Sentiment surged by 18% from 79.5 in August to 93.8 in September, an 18% rebound despite the official revelation of Australia being pushed into the first recession since 1992.

- August had witnessed a sharp fall in sentiment due to Victoria’s second wave of COVID-19 outbreak. As new cases slowed down due to an imposition of lockdown, other states also witnessed the same with no new cases.

- While assessment of family finances proved to be buoyant than a year ago, the economic outlook and assessment of spending conditions still stand substantially softer.

- RBA is further expected to take initiatives to loosen the monetary policy.

- Consumer sentiment is returning to normal levels, but there is uncertainty in containing the virus and opening up of economies, which can hamper the progress of the country.

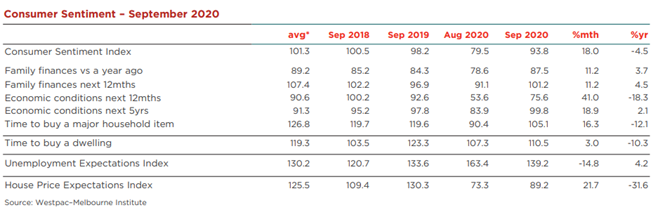

The Westpac-Melbourne Institute Index of Consumer Sentiment soared 18% from 79.5 in August to 93.8 in September. The index is at present just 1.6% below the average over the 6 months prior to the advent of COVID-19 in March. The rebound of 18% after a collapse of 9.5% in August has occurred in spite of the official evidence that Australia has slipped into the first recession since 1992.

DO READ: Australia in recession for the first time in Three Decades; Are There Any Emerging Green Shoots?

The steep drop in August was due to the worsening virus situation in Victoria, where difficult lockdown restrictions were imposed including the Stage 4 restrictions in Melbourne. However, other states were equally weak.

While New South Wales (NSW) saw a 15.5% slump in the confidence as it witnessed continued clusters of virus cases and wider second wave concerns amid Victoria outbreak, Queensland witnessed confidence dive by 8.1%.

Nonetheless, new virus cases in Victoria slackened significantly due to an imposition of lockdown, also, there was no evidence of the second wave in NSW or Queensland.

As per ABS’ latest release dated 8 September, payroll jobs throughout Australia, dropped by 0.4% across the period of 1-month till 22 August.

The head of Labour Statistics, ABS, Bjourn Jarvis stated that accommodation and food services and Arts recreation services had shown signs of improvement by nearly half of the lost payroll jobs hitting the low point in middle of April, staying at 21% and 14% lower than middle of March.

He further added that the industries mentioned above mostly suffered the blow in Victoria, with payroll jobs at 38% and 23%, respectively lesser than middle of March.

He also said that throughout the month’s period up to 22 August payroll jobs plunged down by 2% in Victoria, whereas remaining states of the country reflected payroll jobs increasing by 0.1%. Victoria persisted to reflect the plunge in payroll jobs until the third week of August, which was however at a slower pace than initial part of the same month.

ALSO READ: Payroll Jobs Fall Further In Victoria | ASX Market Update

The September survey was concluded before a slower than generally anticipated move towards reopening was announced on 6 September. Any discontent with this statement could have lowered the 14.9% rise in confidence in Victoria. However, the success achieved in containing the virus would have still overshadowed the dissatisfaction at prolonged lockdown measures.

While assessing September results with that of June when states were in the process of reopening and second wave problems had not yet appeared, confidence in September was back at its June level in NSW; 5.6% lower than June level in Victoria; 2% above in Queensland; 11.2% above in Western Australia and 3.8% above in South Australia.

All components of the index showed improvement

The fiscal support measures taken by the government are evident in the components of the Index. Evaluation of family finances are better relative to a year ago, whereas the economic outlook and assessment of spending conditions are still substantially weak.

The September sentiment results showed that:

- The ‘finances vs a year ago’ sub-index and the ‘finances, next 12 months’ sub-index increased by 11.2% each in September, up by 3.7% and 4.5% above the level in September 2019, respectively.

- The ‘economy, next 12 months’ sub-index rose 41%, but is yet 18% lower than its level a year ago.

- The ‘economy, next 5 years’ sub-index rebounded strongly from the August fall, to be up 19% over the month and 2% above the level last September.

- The ‘time to buy a major household item’ sub-index elevated by 16.3%, but still 12.1% below the levels in last year same month, while the ‘time to buy a dwelling’ index rose by 3% in September

- Sentiment around employment prospects improved by 14.8% in September, while Consumer House Price Expectations Index increased by 21.7% to a robust 10.7% above the June levels in the same month.

Source: Westpac, dated 9 September 2020

Further, ultra-low interest rates compared to a year ago, have lessened the need to pay down debt with 17.1% respondents choosing to pay down debt as a sensible form of saving down from 20.7%. However, preferences of respondents have not shifted to the ‘riskier’ investments like shares and property.

GOOD READ: 5 Tips for dealing with reopening of the economy during COVID-19

There has been a shift in inclination towards bank deposits across the period of one year, with 32.7% respondents preferring bank deposits compared to 26.7%. The overall numbers show that Australians still have an extremely risk-averse preferences for their savings.

RBA expected to loosen monetary policy ahead

The Reserve Bank of Australia (RBA) grew its Term Funding Facilities to ADIs (Authorised Deposit-taking Institutions) from $152 billion to $209 billion, by $57 billion at its latest meeting and the facilities provide ADIs with funding for 3 years fixed at 0.25%. The facilities can be used by ADIs, comprising banks to buy other securities and refinance offshore borrowings. This increased liquidity is anticipated to lower rates further.

ALSO READ: RBA retains cash rate at 0.25% yet again; Majority of ASX indices ended in red

As per Bill Evans, Chief Economist of Westpac, more initiatives to expand the monetary policy are expected from RBA going ahead. This prediction also comes after the announcement from the US Fed that more stimulus is possible as it increases its inflation target.

He also added that further move to expand the money supply are fitting as its actions complement with a renovated budget in October. The July 2022 tax cuts; improving investment allowances; further one-off payments to low-income earners; and a faster infrastructure program can all fairly be expected to be brought forward.

The survey showed that consumer confidence has been returning to normal levels, but the progress in the virus management and opening up of economies still cloud the overall outlook.