Inherited shares are stocks which individuals get through inheritance after the original investor or holder is dead. Inheritance refers to all or part of the assets of a person that are passed on to their loved once after they pass away. Inheritance can be in the form of cash, property, stocks, bonds, jewellery, bank accounts. Inheritance tax is a tax on the estate of someone who is dead. When inheriting shares, the increase in the share value from the time the original holder purchased it till his death is never taxed. So, the beneficiaries are liable for income on capital gains they get during their lifetime.

How much tax you must pay on inherited assets depend on the value of the deceased’s estate, which is based on their assets minus any debt.

Usually, the owner of the assets writes a will on how his/her assets will be distributed. But if the owner dies without leaving a valid will, their assets must be shared out according to certain rules that are known as rules of intestacy and only married or civil partners, and some other close relatives can inherit the assets.

Usually, you do not have to pay tax on anything you inherit at the time you receive it.

You may need to pay:

- Income tax on profit you later earn from your inherited assets such as rental income from property and dividend.

- Capital Gain tax if you sell inherited property or shares.

- Inheritance tax.

Copyright © 2021 Kalkine Media

UK Inheritance Tax and Laws

The Inheritance tax (IHT) can be reduced or avoided in several ways such as gifting, and the tax will only be paid on estate worth above the threshold.

For the year 2021-22, you don’t have to pay any Inheritance tax if the value of the inherited assets is below the £325,000 and you still need to report it to HM Revenue & Customs (HMRC). This means only the value of assets above for £325,000 will be taxed at 40%. The Inheritance tax allowance is increased if the assets include property is passed to a direct descendant such as children or grandchildren then the threshold can increase to £500,000.

Married couples and civil partners can also pass on their allowance to their spouse. If your assets are worth less than your threshold, so any unused threshold can be added to your partner’s threshold when you die. Which means their threshold can be as much as £1 million.

If the person has left 10% or more of the net value to charity in his/her will, the inheritance tax can be reduced to 36% from 40%.

Reliefs and Exemption

If the deceased person has given some gifts when he/she is alive, that may be taxed depending on when the deceased person gave the gift. The person may get taper relief, which means the Inheritance tax charged on the gift is less than 40%.

Business Relief allow some assets to be passed with no Inheritance tax or with a reduced bill. Further, a person may also get Agriculture Relief if the assets include a farm or woodland.

The inheritance tax is not paid directly, but funds from your estate are used to pay to HM Revenue and Customs (HMRC). Person who received any gift might have to pay Inheritance tax, but only if the deceased person gives away more than £325,000 and died within 7 years.

You may also need to pay Inheritance tax if your inheritance is put into a trust and the trust can’t or doesn’t pay.

Inheritance laws for money and shares

In most cases beneficiary doesn’t have to pay any tax on money and shares but have to pay tax if the deceased person’s estate can’t or doesn’t pay, in such case HMRC will contact the beneficiary.

A beneficiary has to pay income tax on interest earned from money and dividends paid on shares that were inherited. Further, he has to pay capital gains tax if inherited shares are sold and that have gone up in value since the person died.

Inheritance laws for joint property, shares and bank account

In most cases, the beneficiary doesn’t have to pay any stamp duty or tax in inherited property, shares or the money in joint bank accounts with the deceased person. Inheritance tax will depend on how shares or property were owned and how the bank accounts were set up.

If a person and deceased person jointly own an asset then they will be known as joint tenants and if the person owned a part of the assets then they are known as tenants in common. Each part could be half or an agreed percentage of the money, shares or property.

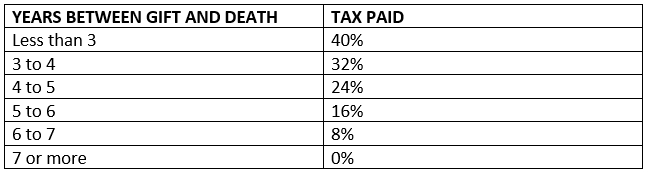

The 7-Year Rule

The Inheritance tax is to be paid at 40% on the gifts given by a deceased person three years before his death.

The gifts transferred by deceased person 3 to 7 years before the death are taxed on a sliding scale known as taper relief.

The Inheritance tax is not paid on small gifts that are made from normal income; these types of gifts are known as exempted gifts.

The gifts that are taxable are:

- Anything that has a value such as property, money, possession;

- The loss when a person sells assets to his child for less than its worth, the difference in value is known as gift.