Highlights

- Catapult reports revenue growth pushed by increased subscriptions in FY22.

- The wearables company sees the SAAS model as beneficial for its customers.

- The company boasts of US$26.1 million cash at bank.

ASX-listed wearables technology business, Catapult Group International Limited (ASX:CAT), announced its FY22 financial results today (26 May).

The intersection of sports science and analytics has got the company to a 'major inflection point'. As highlighted in its FY22 results, 92% of Catapult's revenue is now contracted and recurring. It's core elite wearables business - P&H pro, reflects high growth. However, the company is still losing, reporting negative EBITDA and NPAT numbers. As a result, on ASX, CAT's share price is down 1.739% to AU$1.130 a share today morning (10:26 AM AEST).

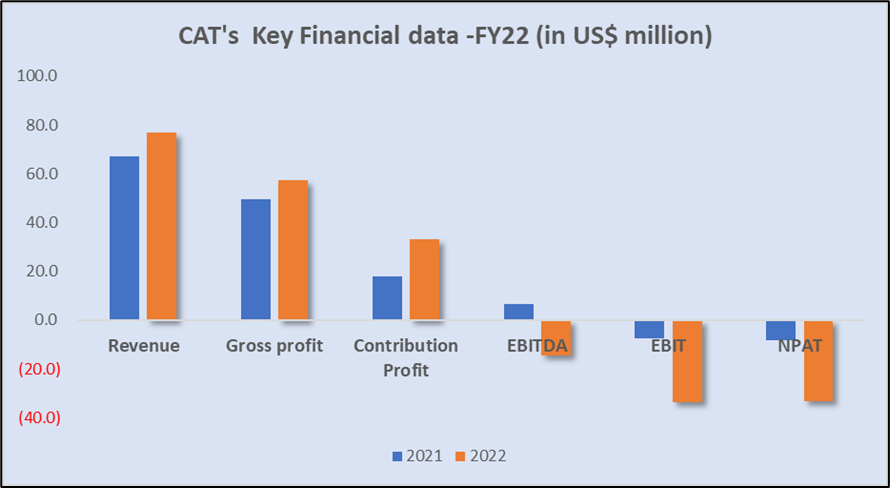

A financial snapshot of Catapult’s FY22

Catapult has witnessed a subscription growth of 29% in FY22 due to an accelerated ACV growth. The total revenue has seen a 14.4% boost over FY21 as a proportion of high-growth subscription revenue offset the cessation of its capital P&H sales. Based on revenue growth, the company's gross margins have improved slightly. There is a reported increase in the proportion of Catapult's subscription business revenue, consistent with its additional investment in accelerating ACV growth.

Image source: © 2022 Kalkine Media ®

The year-on-year change in underlying EBITDA, free cash flow and R&D spending is also in line with the company's accelerated growth investment in sales. However, it has reported an underlying EBITDA loss of US$5.8 million. Meanwhile, the operating cash flow has remained positive at US$2.7 million despite the significant operating investments. Notably, Catapult has reported strong performance against its key SaaS metrics.

While Catapult's growth investments were fully funded, it claims to have a previously proven ability to generate positive EBITDA and free cash flow. It also claims to be well-positioned financially, with US$26.1 million worth of cash in its bank account (as of 31 March 2022).

Management’s take

Talking on the recently released FY22 results, Will Lopes, CEO of Catapult Group International Limited, said that the company's transition into a fully SaaS model could better serve its customers and provide them with the objective data they need. According to him, the 'dramatically' accelerated subscription revenue is proof of this. Talking about business verticals, he said the P&H vertical delivered high growth. Also, its Tactics and Coaching solutions business witnessed a boost after the acquisition of SBG.

He believes the post-pandemic sports world has a strong rebound in sales, especially in North America, increasing its future confidence. New customer addition and latest innovations continue to position Catapult for capturing demand at all levels of the sport.

More from Technology- Pushpay (ASX:PPH) shares spurt after acquisition talks are confirmed

The road ahead for Catapult

Catapult remains confident about a strong ACV (annual contract value) growth in the short and medium-term. The anticipated ACV growth range is 20-25% in FY23, with an ACV Churn of 4.5 to 6.0%. The company is also confident of its ability to generate strong operating cash flow even in the long term. Catapult expects to generate a positive cash flow in FY23, and its planned organic investments remain fully funded.

However, Catapult continues to see a moderate degree of supply chain challenges and cost inflation in FY23. The company predicts these to impact freight, COGS, wage costs, and inventory sourcing.