After a rocky start to the year that began with the bushfires and now owing to the coronavirus pandemic and an oil price war hitting share prices hard, ASX 200 shares seems to be at a turning point finally after the index has been up by over 200 basis points in May. Though the sinusoidal trend has continued to make investors nervous, sentiments seem to be building on positively after economies gradually ease lockdown restrictions and the possibility of a vaccine keeps hope high.

On 19 May 2020, the S&P/ASX200 ended the trading session at 5559.5, up by 1.81 % or 99 basis points.

The top gainer of the index was James Hardie Industries Plc (ASX:JHX) and the day’s hot stock fetched ample market and media interest after it released its Q420 and preliminary final report for the year ended 30 March 2020 results.

The stock quoted $23.82 per share and zoomed up by 11.204% relative to its last close. It has an annual dividend yield of 1.94 and has delivered returns of 15.72% in the last one month.

JHX’s Financial Results- Q420

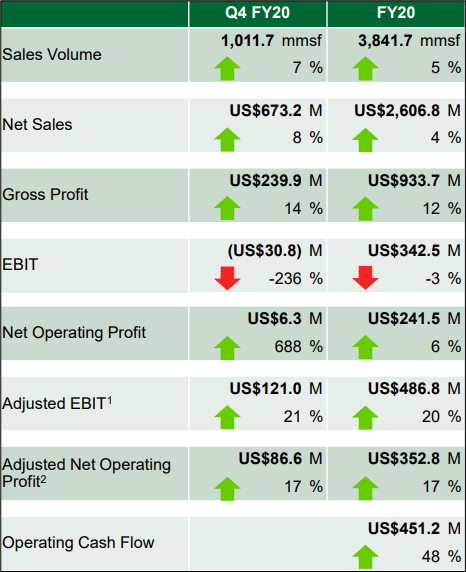

On 19 May 2020, JHX declared results for the 4th quarter along with year ended 31 March 2020.

Globally, the Company delivered robust fourth quarter results, showcasing its capability to constantly perform in growing as well as highly volatile markets. The quarter also marked JHX’s fourth consecutive quarter of robust financial results, with a full year Adjusted NOPAT worth US$ 352.8 million, up by 17% relative to the prior year (pcp).

Q420 Highlights

- Group Adjusted EBIT of US$ 121 million, up by 21% on pcp

- Group net sales of US$ 673.2 million, an increase of 8% on pcp

- North America Fiber Cement Segment volume increased 10% compared to pcp

- North America Fiber Cement Segment Adjusted EBIT margin was 25.3%

- Asia Pacific Fiber Cement Segment Adjusted EBIT margin was 20.5%

- Europe Building Products Segment Adjusted EBIT margin was 4.6%

CEO, Dr. Jack Truong seems particularly pleased with the outstanding North America performance as the Company continued to grow above market while delivering exceptional returns. Supporting this achievement was 11 percent volume growth noted in its exterior business division along with interior business’ sustained volume growth recorded at 5 percent.

The Company’s Lean manufacturing initiative demonstrated enhanced performance throughout the North American manufacturing network, and catalysed the delivery of 26% Adjusted EBIT increase (25.3% Adjusted EBIT margin).

The APAC segment’s financial returns yielded revenue which was up by 2%. The Company’s Europe Building Products section showcased robust revenue increase noted at 7 percent in Euros (directed by fiber gypsum rise of 3 percent and fiber cement growth of 50 percent).

Despite the extremely volatile operational market situation in March 2020, JHX was successful in supplying to its customers impeccably, growing revenue by double digits in all its operative region and making the month remarkably strong.

This propelled substantial upgrading in the Company’s liquidity position, which was up from US$ 464 million at 31 December (last year) to US$ 510 million at 31 March (current year) and finally US$ 578 million at 30 April (current year). The leverage ratio trimmed to a multiple of 1.9x as noted on 31 March this year (from 2.1x recorded on 31 December last year).

JHX’s Financial Results- FY20

The Company’s FY20 result was catalysed by the strong North America performance, delivering over 7% growth above market and US$ 29 million in Lean cost savings in the fiscal year. JHX’s (full year) EBIT margin in North American region was reported at 25.9 percent.

FY20 Highlights

- Group NOPAT was reported up by 17% on pcp at US$ 352.8 million

- Group Adjusted EBIT demonstrated an increase of 20% on pcp at US$ 486.8 million

- Group net sales were up by 4% on pcp at US$ 2,606.8 million

- North America Fiber Cement Segment volume increased 8%

- North America Fiber Cement Segment Adjusted EBIT margin was 25.9%

- Asia Pacific Fiber Cement Segment Adjusted EBIT margin was 22.7%

- Europe Building Products Segment Adjusted EBIT margin was 8.2%

Dividend Details

No FY2020 second half dividend will be paid to CUFS holders. The FY2020 first half ordinary dividend of US 10.0 cents per security was paid to CUFS holders on 20 December 2019. JHX will be required to deduct Irish DWT of 25% of the gross dividend amount for future dividends unless the beneficial owner has completed and returned a non-resident declaration form.

The FY2019 second half ordinary dividend of US26.0 cents per security was paid to CUFS holders on 2 August 2019. The FY2020 first half dividend was and any future dividends will be unfranked for Australian taxation purposes.

Q420 & FY20 Highlights (Source: JHX’s Report)

JHX’s Current Priority

Globally, pandemic protocols are expected to be in place and the Company has been adhering to strict social distancing policy and extensive disinfection and hygiene processes. It has been facilitating 24/7 PPE and hygiene kits, sick leave and child-care support, work from home models where applicable to service customers seamlessly while ensuring the safety and well-being of its employees to offer a safe and sustainable work environment.

JHX also aims to gain market share, execute lean manufacturing initiatives, develop high impact innovations, and ensure strong liquidity and financial flexibility.

JHX’s Outlook

Currently, the Company is unable to provide annual guidance owing to the highly volatile and uncertain circumstances driven by the COVID-19 pandemic and its impact on demand in the Company’s operative countries. However, with the anticipation of continued positive momentum into FY21, the following forecast was provided, based on current estimates and assumptions-

- In Q121, the North America segment Adjusted EBIT margin is likely to be between 22% and 27%

- At the end of Q121, liquidity might exceed US$ 600 million

- At the end of Q121, leverage ratio could remain below 2.0x

JHX believes that one needs to stay strong during the crisis to emerge from it even stronger. At the back of relentless focus on safe and sustainable work environment, an outstanding FY20 performance, strong liquidity and financial flexibility that has resulted in the expectation of continued positive momentum into FY21, it will be interesting to gauge today’s i.e. 19 May 2020 ASX gainer unfold itself in forthcoming months.

(NOTE: Currency is reported in Australian Dollar unless stated otherwise.)