About Tesla: Tesla, Inc. (NASDAQ: TSLA) is engaged with the designing, developing, manufacturing and selling fully electric vehicles. Apart from this, the company is also involved in solar energy generation and energy storage products, which includes the complete process comprising of - designing, manufacturing, installing and selling of these products. The organisation categorises the functional activities of the business in two segments- (a) automotive, and (b) energy generation and storage.

2QFY19 Results Update: The company recently, announced its quarterly numbers for the second quarter where it posted record production and deliveries resulting in the generation of free cash flow of $614 million during the period. With net proceeds of $2.4 billion in the combination of public offering of equity and convertible bonds, the company saw a cash and equivalents of $5 billion at the end of the period, which was also a record in the history of TSLA. With decent cash on working capital front, the company is focusing on the launching of Model 3 production and Model Y production in China and the United States, respectively. With the steps taken for increasing cost efficiencies coupled with strong deliveries in the quarter, the company saw a substantial decline in GAAP net loss as compared with the first quarter of 2019.

Model 3 Update: In the Q2 FY19 period, Model 3 witnessed the highest deliveries attaining a record of 77,634. Further, Model 3 in the US region, proved to be the best-seller among the premium vehicle. Moreover, the outselling of gas-powered equivalents combined, saw a strong momentum in other markets. Europe is witnessing good improvement in terms of sales of Model 3 where the model is performing in-line with its recognised premium players. The Management previously had notified that over 60% of Model 3 trade-ins are not premium brands, which shows a comparatively bigger addressable market for Model 3 than earlier expected. Model 3 is available with all the variants in the geographies - North America, Europe and Asia and is gaining in terms of customer preferences. During the period, it was also observed that the majority of the orders were placed by the consumers for a long-range battery option with an average selling price for Model 3 standing at ~$50,000. With the higher demand, cost related to manufacturing continued to decelerate. Model 3 witnessed an improved momentum on production front during the quarter, with record production during the months of May and June 2019. The manufacturing equipment in Fremont witnessed a capacity of producing 7,000 Model 3 vehicles for a single week which is expected to rise further. The company is targeting the production of 10,000 total vehicles for all the variants of Model 3 in a week by the end of calendar year 2019.

Model Y Update: Tesla initiated the preparation for Model Y production in Fremont in the second quarter of 2019. With the substantial overlap of vehicle parts for Model 3 and Model Y, the company was benefited from leveraging the present manufacturing designs, while developing the manufacturing facilities for Model Y. Moreover, the company is putting its effort to accommodate the cost related to Model Y with only a minimum cost premium targeted over Model 3. The company expects Model Y to be more valuable in terms of profit as compared with Model 3 on account of the larger market size for SUVs with higher ASP.

Infrastructure Update: With the growth in fleet, the company has continued to expand its service and Supercharger capacity. During the second quarter, the company witnessed an addition of 101 vehicles to Mobile Service fleet along with inaugurating 25 new store and service locations. The size of customer fleet has been doubled in the last twelve months and losses from service were stable on yoy basis. Supercharger capacity grew to around 1,600 charging locations on globally with accelerating rate of throughput of vehicles.

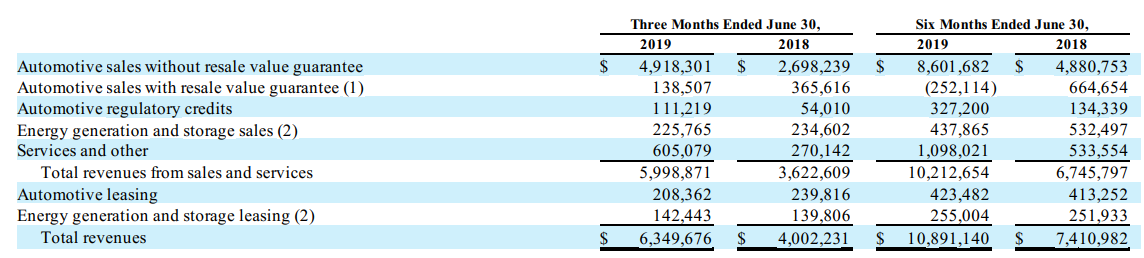

2QFY19 Revenue Mix: Besides, during the second quarter of FY19, the company recorded a revenue of $6,349,676 as compared to $4,002,231 in the prior corresponding period. For the 6 months period ending 30 June 2019, the company recorded the total revenue of $10,891,140 against $7,410,982 in the prior corresponding period.

Total Revenues (Source: Companyâs Report)

Total Revenues (Source: Companyâs Report)

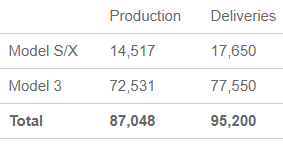

Q2 2019 Vehicle Production & Deliveries: Also, the company recently announced its production numbers for the second quarter FY19. During the period, the company produced vehicles of 87,048 with record deliveries of ~95,200 vehicles as compared to the quarterly highs of ~91,000 deliveries, and ~86,600 units produced in the fourth quarter of 2018. Moreover, the company progressed well in terms of streamlining its global logistics and delivery procedures to improve the working capital management with increasing cost efficiencies. A number of orders in the period were observed surpassing the deliveries. With this, the upcoming quarter would see a higher order backlog and the Management is quite confident about its positioning with increasing production and deliveries in Q3. At the end of 2QFY19, customer vehicles in transit stood at more than 7,400.

Production and Deliveries in 2QFY19 (Source: Companyâs Report)

Acquisition of Maxwell Technologies: Recently, in May 2019, the company announced that it has completed the acquisition of Maxwell Technologies by swapping all outstanding shares of the company for 0.01930 per common share of Tesla along with cash in lieu of any fractional shares of Tesla common stock, excluding interest and less withholding taxes, if any. The purchase consideration was of $207.2 million (902,968 shares issued at $229.49 per share, the opening price of Tesla common stock on the Acquisition Date).

Outlook: Further, TSLA intends to increase its manufacturing reach to new geographies with the help of introducing new products and better customer experience. As the cost efficiencies require an improvement in utilising the existing factories and local production, the company is progressing well to introduce the local production of the Model 3 in China which is likely to take place at the end of 2019 and Model Y in Fremont is expected to be introduced in the beginning of 2020. The company is making its effort for European Gigafactory and expects to conclude the site location in the upcoming quarters. The company intends to make the higher deliveries on annual and sequential basis. However, instabilities are not ruled out as a result of seasonal effect. The earlier guidance for the vehicle deliveries for the year stood at - 0.360 million to 0.400 million. Moreover, the company is expecting free cash flow for the quarters to be in positive territory whereas the periods of introducing new products and ramp up activities might see some variations.

The company is of the view that it has reached to the stage of being self-funded and with this, it expects the GAAP net income to be in positive territory for the third and further quarters. However, the Management will remain focused on increasing the volume, capacity expansion along with cash generation. The company has planned the capital expenditure for 2019 to be in the range of $1.5 billion to $2 billion which is lower than the earlier projection.

The Management will look for the opportunities so that it can enhance its capital efficiencies and shift cash outflows for the upcoming quarters. The projections involve progress of key projects and the expansion of Supercharger and service networks.

Stock Performance: On 13 August 2019, TSLAâs stock last traded on NASDAQ at a market price of $235, with a market capitalisation of the stock standing at ~$42.09 billion. The stockâs trading range for the 52-week high and low was noted of $379.49 - $176.9919, respectively. The stock has corrected ~34% in last 1-year period.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.