Will the rate cuts have a positive impact on the sluggish performance of the hardware division of Metcash Limited (ASX: MTS)? The implementation of the rate cut would explain this with time.

The hardware pillar of the company had a major customer loss in the Queensland region and a slowdown in trade sales with lower sales in ~ first two months of FY20 than PCP. Moreover, impact of the present changes in the economic conditions (related to the residential housing sector, construction and DIY activities) on the pillar cannot be predicted at the moment. Though, the company believes that there has been some improvement in the network post the federal elections.

MTS tumbled 9.84% today on ASX post the release of FY19 results, settling at A$2.840.

Company Profile:

A market leader in the wholesale distribution and marketing industry, Metcash Limited has three main pillars- food, liquor and hardware. The company was founded in 1920 and was officially listed on ASX in 2005. MTS has its registered office in New South Wales.

FY19 Full Year Results:

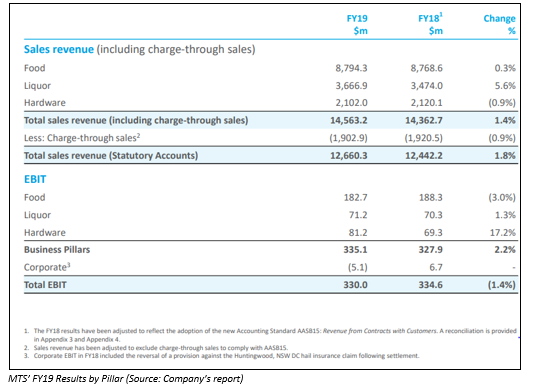

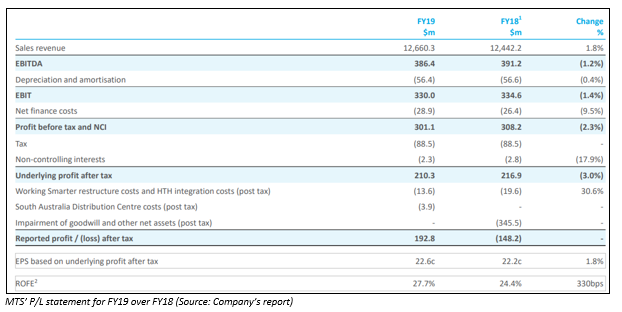

On 24 June 2019, MTS announced its full-year results for 2019. The group sales were up 1.8 per cent on pcp and amounted to $12.7 billion.

The groupâs EBIT reported a drop of 1.4 per cent, reaching $330 million; the food EBIT was down 3 per cent to $182.7 million, liquor EBIT was up 1.3 per cent to $71.2 million and hardware EBIT increased 17.2 per cent to $81.2 million.

The corporate EBIT was recorded at a negative $5.1 million, though it was $6.7 million in FY18.

During the reported period, MTSâ underlying PAT registered a decline of 3 per cent and was recorded at $210.3 million. Its statutory PAT amounted to $192.8 million in FY19, compared to a loss of almost $148.2 million in the same period a year ago. The underlying EPS grew 1.8 per cent to 22.6 cents in FY19.

Let us have an overview of the performance of each segment:

Food: The total sales for supermarkets were down 0.5 per cent, reaching $7.2 billion in FY19. The wholesale sales dropped by 1.5 per cent in the financial year 2019, including a 1.3 per cent decline in 2H19, demonstrating a fourth consecutive half-year period of improvement in the decline rate. On the convenience front, total sales grew 4.4 per cent to $1.6 billion in FY19, driven by new customers, growth from main customers and increased sales of tobacco.

Liquor: The total sales for the segment registered an increase of 5.6 per cent to $3.7 billion in FY19, while wholesale sales to IBA bannered network grew 5.3 per cent. The companyâs IBA retailer network strength was demonstrated, as IBA bannered network reported six years of continuous LfL sales growth.

Hardware: This pillar generated substandard results for the company on the sales front with the total sales down by 0.9 per cent, impacted by the slowdown in construction activity and loss of customers in Queensland in the first half. The online sales, however, grew and trade sales were up (approximately 65 per cent of total sales).

Other Updates and Dividend Update:

The FY19 final dividend stood at 7 cents per share, fully franked with the payment date of 7 August 2019. For FY19, the companyâs total dividends stand at $0.135 per share. The dividend payout ratio is approximately 60 per cent of the underlying earnings per share.

With the completion of its 3-year Working Smarter program, the company recorded a cumulative saving of ~$125 million.

MTS Outlook: The companyâs next five-year vision, named MFuture, is now underway, under which it has several key growth initiatives, like small format convenience store trial and DSA program acceleration under food pillar, national rollout of Porters Liquor and corporate store trial under liquor pillar, and expansion of company-owned stores under hardware pillar.

On the Liquor side, the premiumisation consumption is likely to drive the market in FY20. The focus would also be on the MFuture initiatives to enhance the IBA network.

The company expects additional cost savings to overcome any probable slowdown in the construction activity in FY20.

Changes in the Board: Besides the full year results for 2019, Metcash also notified about a couple of changes in the companyâs Board. Anne Brennan would step down from her role of Non-Executive Director in August 2019 post the companyâs Annual General Meeting for 2019.

Meanwhile, Fiona Balfour would not be contending for re-election at the Annual General Meeting and would retire post the conclusion of the meeting, after serving for almost 9 years as one of MTSâ non-executive directors.

Helen Nash would replace Fiona and assume the role of the Chair for the companyâs People and Culture Committee, while the Board hunts for the other probable and appropriate replacements as non-executive directors.

Earlier this year in February, it was announced that ASX- Listed eCargo Holdings acquired 85 per cent of MTSâ Metcash Export Services Pty Limited, which includes foreign subsidiary in China. ECG is basically a technology, eCommerce and specialist execution group of companies.

The consideration paid for the acquisition amounted to A$2.5 million and 85 per cent of the NAV of the business worth ~A$6 million along with a deferred payment of ~ A$3.5 million.

Post this activity, ECG would tap the growing consumer market in China by having a one-stop offering for businesses to take leverage of the Chinese markets.

MTS is a wholesaler and distributor to a number of retail chains and supermarkets in China. The company functions through cross-border eCommerce stores via key platforms like Alibabaâs Tmall Global and JD Worldwide.

Share Price Information: After the close of business on 24 June 2019, the companyâs stock was trading at A$2.840, down by 9.84 per cent compared to its last trade. With a market capitalisation of A$2.86 billion, the stockâs 52 weeks high and low is A$3.210 and A$2.250, respectively. The annual dividend yield of the stock is 4.29 per cent. It has generated returns of 3.62 per cent, 20.69 per cent and 31.25 per cent in the last one, three and six months, respectively.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.