The ongoing earnings season in corporate world has its own significance as various companies have released their results for the full year. Hence, the details for the whole year come into visibility at one place for assessment by the investors. The annual report contains the detailed information of financials, project development and deals, if any, etc. Today, we are discussing two stocks - SeaLink Travel Group Limited and Rural Funds Group with an eye on dividends.

SeaLink Travel Group Limited

SeaLink Travel Group Limited (ASX: SLK) provides ferry services, tourism cruises, charter cruises and accommodated cruising. The company is also engaged with accommodation and restaurant services at Fraser Island and Vivonne Bay, coach tours, tug and barge services, travel agency services, and packaged holidays.

FY19 â Key Highlights: The recently completed year saw benefits from past acquisitions and business development initiatives. Fraser Island business in Queensland and Bruny Island ferry operations in Tasmania performed well. Tourism businesses faced challenges from unseasonal weather events, slower international visitor growth, and unplanned local disruptions. The company maintains its focus on growth opportunities, mainly, in transport industry to enhance the stability and diversification and to set off the seasonality impact on the business.

On operational front, the company integrated the Kingfisher Bay Resort Group and refurbishments were initiated. SLK commenced the Bruny Island ferry service in Tasmania along with the start of construction of two vessels intended for the purpose. During the period, the company divested two Capricornian Class vessels for which the net proceeds at $9.9 million was higher than book value.

The company declared a final dividend of 8.5 cents per share (fully franked) which will be payable on 17 September 2019 to shareholders registered as on 4 September 2019. The announced dividend was higher by 0.5 cents per share compared to FY18. With this, the full year dividend for FY19 comes in at 15 cents per share, up from 14.5 cents per share in FY18.

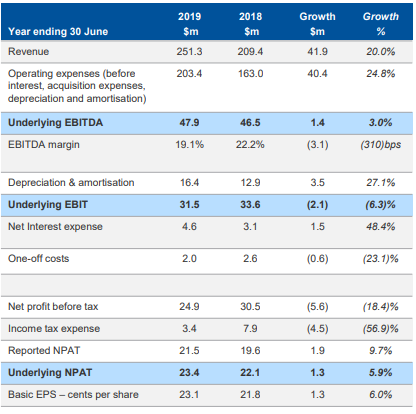

The company recently, released its full year results for FY19, according to which, SLK recorded a statutory Net Profit after Tax (NPAT) of $21.5 million as compared to a NPAT of $19.6 million in FY18. Underlying NPAT stood at $23.4 million as compared to $22.1 million in the previous financial year, posting a growth of 5.9%. Underlying EBITDA at $47.9 million posted a growth of 3% against EBITDA of $46.5 million in FY18. FY19 underlying EBITDA did not include impairment of the investment in UWAI amounting to $1.6 million, business acquisition costs related to Fraser Island worth $0.2 million, and expenses valued at $0.2 million associated with the unsuccessful tender for Sydney Ferries. The company posted strong net operating cashflow of $40.7 million during the period which was up 42.8% year over year. Net debt on balance sheet also declined by $21.4 million or 20.3% year over year to $83.9 million.

Summary Profit Statement (Source: Company Reports)

Divisional Performance:

SeaLink South Australia: The division witnessed a fall of 6.6% in EBIT (before corporate allocations) to $16.9 million in FY19 as compared with $18.1 million in FY18. The decreased EBIT can be attributed to challenging year for the PS Murray Princess, with revenue down 9% from the record high achieved in FY18.

Captain Cook Cruises â New South Wales and Western Australia: With softer demand from international tourism, the division faced challenges during FY19. The division posted a fall of 3.3% in revenues to $53.4 million in FY19 from $55.2 million in FY18, with EBIT declining from a profit of $0.5 million in FY18 to a loss of $1.1 million in FY19. The lower sales and EBIT were mainly on account of lower chartering revenue from the Harbour City Ferries contract along with a sluggish business environment. Dining revenue witnessed a growth of 1.0% in FY19.

SeaLink Queensland: The division witnessed a decline of 8.6% in underlying EBIT to $20.2 million in FY19, from $22.1 million in FY18. Revenues also posted a decline of 0.8% from $78.4 million in FY18 to $77.8 million in FY19, mainly on account of losses of third-party dry leases over two Capricornian vessels valued at $2.3 million.

Fraser Island: The segment performed well with revenues growing at the rate of 3% on the corresponding period of prior year. The division contributed sales of $54.1 million and EBITDA of $8.0 million with EBITDA margin at 14.8%.

Going forward, with the assumption of average seasonal and current business conditions to remain stable along with fuel prices, the Management is well positioned to improve upon FY19 results. The Management expects underlying EBITDA (including the benefit of CCC initiatives) is likely to be in between $49.0 million to $52.0 million for financial year 2020.

At the current market price of $3.510, the stock is available at price to earnings of 17.320x with market capitalization of $ 367.17 million and annual dividend yield of 4.01%. The stock has corrected ~15% in last one year and is currently trading near its 52-week low of $3.440.

Rural Funds Group

Rural Funds Group (ASX: RFF) is engaged in managing agricultural assets.

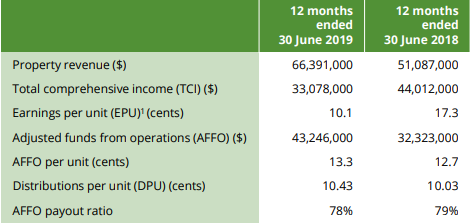

The company recently released its full year financial results for FY19 wherein it mentioned that revenue from property witnessed a growth of 30% owing to JBS transactions, acquisitions, development capital expenditure, and lease indexation. Total comprehensive income (TCI) and Earnings per unit (EPU) were lower mainly on account of non-cash revaluation decrements on interest rate swaps amounting to $18 million. FY19 Adjusted funds from operations (AFFO) per unit came in at 13.3 cents, posting a growth of 4.7% on 12.7 cents in FY18, in-line with forecast. FY19 Distributions per unit (DPU) stood at 10.43 cents against 10.03 cents in FY18. AFFO payout ratio in FY19 at 78% was marginally lower than that of 79% in FY18.

Income and earnings metrics (Source: Company Reports)

During FY19, the company the Group negotiated a transaction related to the acquisition of JBS Australia Pty Limitedâs five Australian feedlots and related cropping land for $52.7 million, including stamp duty and the provision of a $75.0 million guarantee to J&F Australia Pty Limited, for which the approval was received at the unitholder meeting held in the month of August 2018. Another development during FY19 was the purchase of Comanche, a 7,600 hectare (ha) cattle property. During FY19, the company completed an equity placement of $149.5 million to support the JBS transaction, associated costs, and the acquisition of Comanche. RFF purchased Dyamberin (a 1,728-ha cattle property), Woodburn (a 1,062 ha cattle property), Cobungra, a 6,486 ha cattle property, etc. during the year.

Coming to the balance sheet, adjusted total assets witnessed an increase of $222.2 million, mainly on account of the acquisitions, capital expenditure and revaluations of almond orchards, vineyards and water entitlement. Gearing ratio at the end of the period stood at 31% which is within the target range of 30% to 35%, with sufficient capacity to settle remaining acquisitions and committed capex.

The groupâs current assets during FY19 came at $9.33 million including Cash at $2.588 million, Trade and other receivables at $5.043 million. As on 30th June 2019, Investment property and plant and equipment (PPE) were reported at $489.327 million and $172.915 million, respectively.

Net asset value (NAV) per unit came in at $1.57 in FY19 against $1.48 in FY18. Adjusted NAV per unit witnessed a growth of 7%, mainly driven by independent revaluations of almond orchards, vineyards and water entitlement.

Outlook: The Management has forecasted AFFO for FY20 to come in at 14 cents per unit and distribution per unit (DPU) at 10.85 cents per unit, representing a growth of ~4% on FY19. AFFO payout for FY20 is estimated at 77.5%.

At the current market price of $2.120, the stock is available at a price to earnings of 15.080x. The stock closed at $2.120 on 27 August 2019 with a gain of 5.473% on previous trading session, due to the impact of decent results for FY19. The stock has given a negative return of 11.06% and 8.64% in last three-months and six-months respectively. Market capitalization of the stock stood at $673.2 million with 334.93 million shares outstanding. The company has a healthy annual dividend yield of 5.19%.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.