Highlights

- BNPL companies became consumer favourites during the pandemic when many individuals suffered from job losses and delayed payments.

- BNPL service providers do not charge interest on loans and slip past the existing Consumer Credit Code.

- The new changes would be able to protect consumers and create a more secure BNPL segment.

Buy-now-pay-later companies have had a rollercoaster ride since they rose to power during the early days of the pandemic. After quickly garnering public attention, BNPL firms came under the scanner for the lack of regulation seen in the sector. However, authorities were quick to respond to this lack of regulation and have been introducing reforms in the sector.

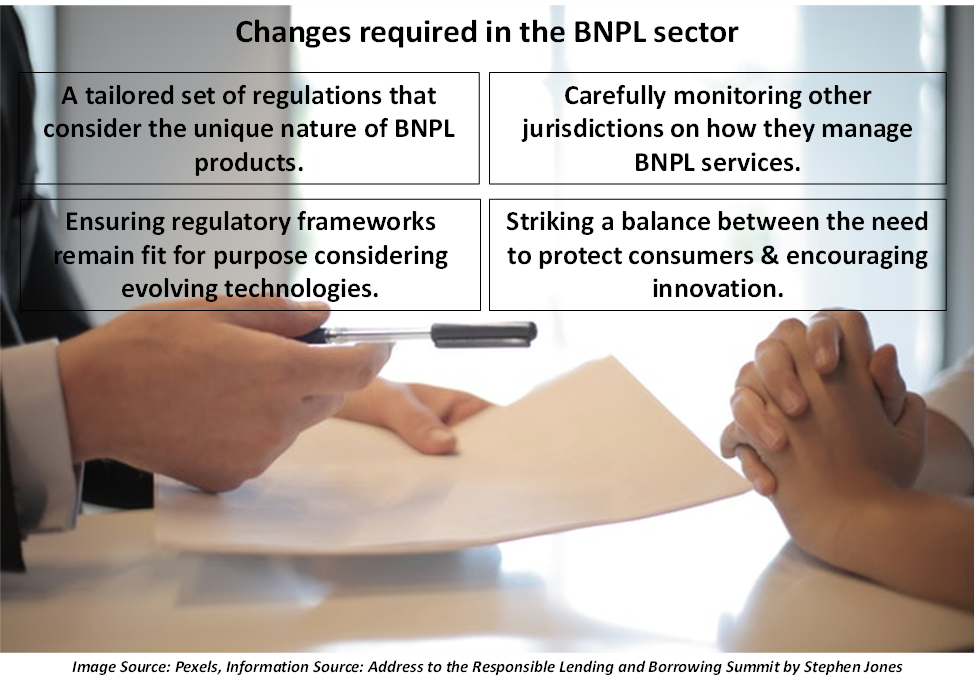

The drastic turn of events seen by the BNPL sector certainly makes it a unique part of the economy. The new changes come as a part of a larger movement towards more robust credit laws.

DO NOT MISS: Is Higher Interest Rate A Peril For BNPL Sector?

Additionally, the changes have been introduced after a series of bad debts and overcrowding of credit markets was observed. Many have hailed the changes as a fresh beginning for the BNPL sector, making the environment more protected and secure for consumers and businesses.

Why are Australians Borrowing More Via BNPL, Payday Lenders?

Since the BNPL sector operates mostly through online methods, slip-ups are likely to snowball into something serious. However, some companies also offer offline methods of executing BNPL transactions. As consumers have the liberty to buy expensive products without actually paying anything at the counter, there is a grave risk for suppliers.

INTERESTING READ: Ten highest paid CEOs of ASX 200 companies

Why is the needle on BNPL companies?

Though the sector has been around for quite some time, it saw a peaking in popularity during the pandemic. Job losses and delayed income forced many households to depend on the easy loan options presented by the BNPL sector. Essentially, BNPL companies offer consumers the option to pay for products later or in easy instalments after buying them from the seller.

In a nutshell, BNPL companies take on the debt of consumers in exchange for a merchant fee. The striking feature here is that this debt comes without any additional interest. Thus, the pandemic was the perfect time for the BNPL sector to soar.

Since no additional interest was charged on the purchases, BNPL services did not directly fall under the Consumer Credit Code. However, the new financial services minister Stephen Jones stated at a recent conference that new protection laws would have to be implemented by 2023 to safeguard consumers.

A new set of rules and restrictions is not the only challenge for the sector, as many big companies have also released their BNPL products. This means increased competition, and a move toward a more closed environment might force small players in the field to exit the market.

What changes will be implemented?

Minister Jones highlighted that BNPL services should be considered a part of the credit ecosystem as they serve the same purpose as other products in the segment. Additionally, the BNPL sector continues to dominate the market, with a large share of consumers showing interest in BNPL services. This further intensifies the need for regulatory oversight in the segment.

As of now, some enhanced features have also been introduced to the BNPL market, which includes performing credit checks on consumers before giving advances. However, these features are not mandatory, and so many companies are not following them.

Additionally, there are no restrictions on how many such services can be availed at a time. This means a user can be availing of BNPL services from multiple providers simultaneously. While this may seem incentivising for some consumers, they are likely to accumulate huge debt, which lenders may not be able to notice.

This can be a major challenge for financially vulnerable households that belong to the low-income category. The additional challenge presented by loan sharks has made the lending market more volatile. They are also known as payday lenders and often target low-income individuals in desperate need of money. These loan sharks also do not charge interest, and much like BNPL players, they also escape the existing credit regulations.

Thus, the new changes aim to protect consumers and make businesses a safe environment to indulge in. Current BNPL giants such as Afterpay and Zip could see a string of new clerical and documental work being unloaded onto them. However, this would ensure that the sector moves onto its next booming phase in a proper and secure manner.