The year 2020 has rather been a kind year for Uranium as we witnessed its prices surge by ~22% from US$24 per pound on 17 March 2020 to US$29.45 per pound on 9 April 2020. Similarly, URA Global X Uranium ETF was up by ~31% from 23 March to 8 April 2020. However, this sudden rise comes post a prolonged fall of ~71% that Uranium witnessed in the last five years, with prices crashing from US$24.04 on 29 April 2015 to US$7.09 on 18 March 2020. On 09 April 2020, the index closed at US$9.49.

What is driving the sudden spike in prices even under a subdued demand scenario due to the COVID-19 spread? The answer lies in economics; if demand is not increasing, there must be something happening at the supply side, enhancing the price of Uranium:

Supply Shortage: The closure of world’s biggest Uranium mine Cigar Lake of Cameco, Canada has dwindled the market with 14 million pounds per year of supply. Also, due to the fear of COVID-19, South Africa as a precautionary measure closed all the mining operations, that has resulted in Namibia, a big Uranium player to reduce its supply.

Also, Kazakhstan government restriction due to the Coronavirus outbreak, Kazatomprom, world’s largest producer and seller of Uranium, anticipate its 2020 output to be 16% lesser than the previous guidance for the year. The production amount equates to 10.4 million pounds, comparable to 8% of global supply. Due to the stance taken by the Kazakhstan government the Uranium price to shot up to US$29.45 per pound on 9 April 2020.

The revival of US Domestic Market: US President Donald Trump has earmarked on a US$150 million per year for total ten years, i.e. a total budget of around ~US$1.5 billion to aid the domestic Uranium producers for nuclear power generation. The domestically purchased Uranium is a strategy to reduce the Country’s dependency on imported Uranium which stands at more than 90% of total Uranium consumption in the US.

Falling Impact of Fukushima: In 2011 Fukushima tsunami causing a nuclear disaster that had resulted in a huge number of stockpiles flooding the Uranium market due to the closure of nuclear power generation. The Japanese utility stockpiles selling in the market had dwindled the price below US$18 per pound in late 2016. However, the case no longer holds with many mines cutting the production and suspension of mines. All these factors have led to the anticipated future supply shortage resulting in a surge in the Uranium price.

Would the price continue to rise in the near term?

It all depends on the future scenario of the market. The reopening of mines after COVID-19 may boost the market with Uranium supply. Also, any future mishaps can lead to the stranded stockpiles of Uranium flooding the market as we saw in case of Japanese stockpiled hampering the market since 2011.

Not only this but geopolitical collaboration can also help in maintaining the price of Uranium as we generally see in case of the Oil price by OPEC countries. Kazatomprom can flood the market with cheap Uranium after reopening of mines to drive away the competition from the market by capturing maximum share in the market. Or, it can produce in proportion to maintain the price of Uranium and benefitting every stakeholder in the market.

It is also worth mentioning that though Kazatomprom is the largest producer of Uranium, the price play cannot be sustained for long as Australia being the top Uranium resources could exert pressure on the prices. It is to be noted that 30% of the world’s Uranium comes from Australia, securing 1st position while Kazakhstan stands at 2nd with 14% of total resources as of 2017.

Good Read: Uranium Stock Guide: Paladin Energy.

Australia and Uranium

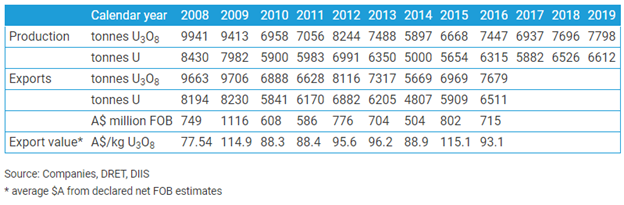

The Uranium mining started in 1954 in Australia, and it holds around one-third of the total world resources. Australia produced around 7798 tonnes of U3O8, placing it as the world’s third top producer after Kazakhstan and Canada. Interestingly, Australia does not use Uranium for electricity generation and exports all the Uranium produced.

Country Wise Uranium Production and Export

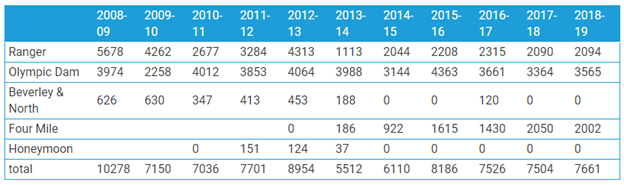

Presently, three mines are operating in the Country to produce Uranium, and they are Ranger mine, Olympic Dam and Four Mile producing around 2094t, 3565t and 2002t of U3O8 respectively in FY19.

Source: World Nuclear Organization, DRET and DIIS

Uranium Outlook

Apart from the closure of big mines in Canada and Kazakhstan, Australia's Ranger mine too is expected close by 2021, depleting the Country's Uranium production. However, upcoming projects such as Honeymoon mine new prospect of Boss Resources may aid in pushing the production by the end of 2025.

As per the Department of Industry, Science, Energy and Resources, the Uranium price is anticipated to increase to US$40 per pound by 2025. Also, Australian Uranium export is expected to increase from A$558 million in FY20 to A$652 million by FY25.