Three Consumer Discretionary stocks discussed under this article include two high-growth business with operations spreading across the major global markets and a major domestic conglomerate.

All these companies have reported interim results and declared interim dividends today (i.e. 19 February 2020).

Wesfarmers Limited (ASX:WES)

Australian blue-chip group, Wesfarmers has reported results for the half-year ended 31 December 2019. It recorded a net profit after tax of $1.21 billion driven by solid performance across Kmart, Bunnings and Officeworks.

A fully franked dividend of $0.75 per share is declared to the shareholders in records on 25 February 2020, payable on 31 March 2020.

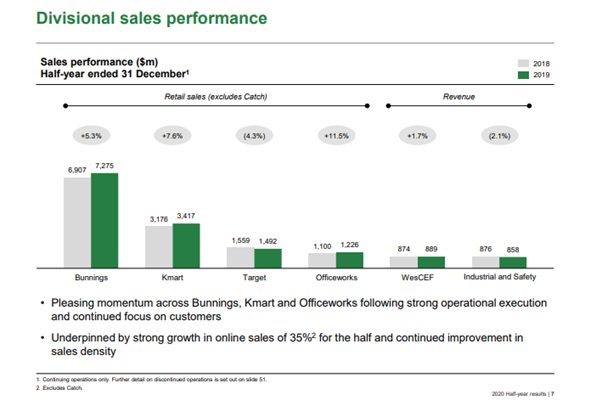

Source: WES HY Presentation

Bunnings

Revenues clocked $7.27 billion for the period, resulting in earnings of $961 million. Net property contributions were lower due to fewer property sales, excluding net contributions from the property, earnings rose 4.3 per cent on pcp.

The improvements efforts were directed to in-store and online customer experience, backed by range expansion, click and collect services.

Kmart

Kmart recorded revenue of ~$5 billion, up 7.6 per cent, with sales increasing by $241 million, offsetting a sales decline of $67 million in Target. In comparison, earnings from the division came lower as against pcp at $345 million.

It includes results from newly-acquired Catch Group. Overall, the division’s lower profit reflects unfavourable FX rates, higher wages, reduction in transactions and subdued apparel performance in Target.

Industrials

Revenues from the WesCEF increased 1.7 per cent to $889 million with lower prices on Chemicals and Fertilisers. Earnings from the business arrived lower at $174 million, down 5.9 per cent over pcp.

Industrial and safety revenue was down by 2.1 per cent to $858 million, and earnings were weak due to subdued performance in Workwear Group and Blackwoods.

Others

There was a profit of $72 million as against $27 million in the previous corresponding period. Results were benefitted from the contribution of Coles Group, property revaluation from Bunnings Warehouse Property Trust, and arrangements from Curragh coal mine.

Outlook

It is being said that the group is positioned to deliver shareholder returns, driven by portfolio restructuring. Its diversified portfolio and commitments to maintaining a resilient balance sheet would enable the group to navigate economic cycles.

Retail divisions of the group are likely to witness investment in efforts to deliver value, quality and convenience. Meanwhile, the industrial portfolio is dependent on commodity prices, FX rates, seasonal and competitive landscape.

WES noted that an oversupply of explosive grade ammonium nitrate in WA market is likely to hurt WesCEF business. Although the group has not faced material disruptions due to coronavirus outbreak, but assessment is ongoing, and the situation is being monitored closely.

On 19 February 2020, WES last traded at $46.55, up by 2.873% from the previous close.

Lovisa Holdings Limited (ASX:LOV)

Fast fashion jewellery retailer, Lovisa Holdings released half year results for the period ended 29 December 2019.

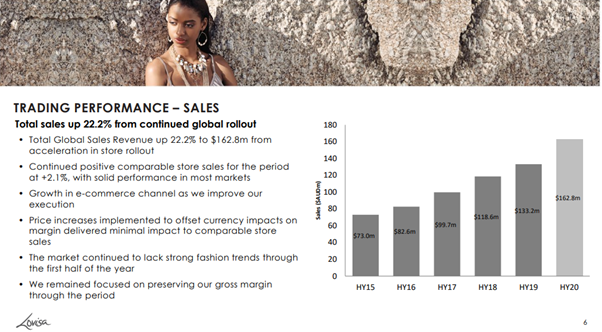

Source: LOV HY Presentation

It has declared a fully franked dividend of 15 cents per share to the shareholders in records on 11 March 2020, payable on 23 April 2020.

Its revenue increased 22.2 per cent to $162.8 million with comparable sales growth of 2.1 per cent for the period with new store additions delivering growth across most markets.

The US and European markets continue to tap growth, and new stores were opened in the UK (4), France (10), and US (21). Sales in South Africa increased by 15.9 per cent benefitted from new stores and comparable sales growth.

ANZ markets recorded strong sales growth for the period, driven by comp sales growth as well as online sales. Asian business was lower due to store closures in Singapore, and slower sales in Singapore and Malaysia.

Despite an increase of 19 per cent in gross profit to $128.5 million, its gross margin was lower by 2% due to FX impacts, and actions were undertaken on prices to tackle lower AUD, but in a constrained manner to maintain brand proposition.

Its investments in people and process were directed to underpin the growing global business. Despite new stores and higher operating costs, the cost of doing business was consistent with the prior period at 50 per cent to sales driven by some efficiency gains.

Its cash from operations before interest and tax was $46 million with operating cash conversion near to 100 per cent. Capital expenditure for the period was $19.8 million driven by new stores, representing an increase of $7.3 million, and thus an increase in depreciation expense.

Outlook

Its Malaysian and Singapore business has been most impacted due to coronavirus, as a result, comparable sales growth is slowing in the early part second-half. Lovisa is witnessing the impact of containment efforts in China, and supply chain issues have been encountered as China constitute a major supply chain part of the business.

It anticipates seeing more influence in the coming months, and the impact due to coronavirus is dependent on the length of the outbreak. Currency headwinds would continue to impact the gross margins.

The company is focused on increasing its store network with investments in support structures, especially in the US, and it continues to review opportunities to enter new markets.

On 19 February 2020, LOV last traded at $11.3, up by 2.914% from the previous close.

Domino’s Pizza Enterprises Limited (ASX:DMP)

Domino’s Pizza franchisee, DMP has released half-year results for the period ended 29 December 2019.

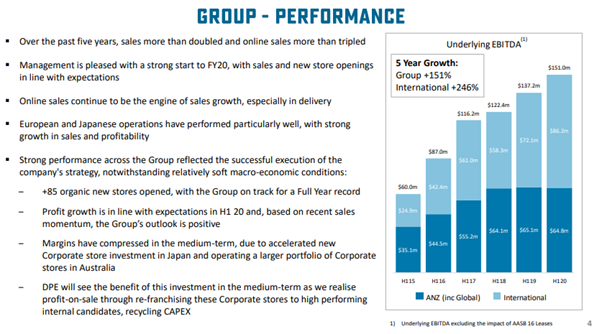

Source: DMP HY Presentation

An interim dividend of 66.7 cents per share, fully franked, is declared for the shareholders in records on 26 February 2020 payable on 13 March 2020.

Its global food sales rose by $151.3 million to $1.58 billion, indicating an increase of 10.6 per cent over pcp, and a 4.1 per cent on a same-store sales basis.

It was noted that the company is on track to surpass $3 billion in global food sale this financial year, driven by international operations aiding growth and profitability in Europe, counterbalancing short-term domestic headwinds.

Growth in online and delivery sales was a major driver to growth across all markets, and online sales clocked $1.1 billion with a growth of 18.8 per cent, including the third party order platforms where the business is holding the aces against incumbent competitors on speed, service, product price and quality grounds.

Its international growth is underpinned by new store openings with 85 newly opened stores across the group, taking the total stores of 2607 across nine countries.

Outlook

It was noted that the same-store sales growth in the first trading weeks of the second half is 6.3 per cent with financial year to date growth of 4.6 per cent. Also, the network sales are up by 10.7 per cent for the financial year to date against pcp.

In the start of the second half, there were 11 organic new stores for trading and significant store opening are planned in the second half of the year.

DMP looks to build on the opportunities presented by the existing markets, having more population than the US and more GDP than China. Besides, the management is active in examining additional markets to deliver value for the business.

On 19 February 2020, DMP last traded at $63, up by 9.641% from the previous close.