It seems to be a prosperous new year for the Australian property market, which has retained its upward trend initiated in the second half of 2019. The property prices revival has swept away every capital city of Australia, particularly Sydney and Melbourne, which continue to lead the market in terms of housing value increases.

Property consultant CoreLogic’s latest home value index demonstrated a rise in property prices in every capital city of Australia, with Sydney and Melbourne showcasing a rise of 1.1 per cent and 1.2 per cent, respectively over January 2020. Market experts opine that Sydney and Melbourne have made up much of the property prices fall they observed in 2018-19 and are likely to reach new peaks soon.

Amidst the current market scenario, Australian property investors are banking on the real estate market, which is expected to return high growth this year. Given this backdrop, let us discuss three real estate stocks listed on the ASX:

GDI’s Half-Year Results Out

Internally managed, integrated funds management and property group, GDI Property Group (ASX:GDI) has recently announced its half year financial results for the period ended 31st December 2019. The Company observed significant progress in its operational divisions during the period, as highlighted below:

- Leased 14,522sqm of lower level accommodation for 5 and 6 years to Minister for Works.

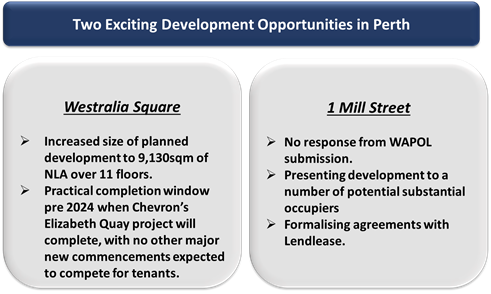

- De-risked Westralia Square, with the upside to be delivered through leasing the upper levels into a stronger market in FY20 and FY21.

- Exchanged contracts to acquire 180 Hay Street, Perth for $12.59 million.

- Purchased a $98.0 million portfolio of 17 metropolitan Perth properties (Portfolio) occupied by high profile car dealerships and service centres on major arterial roads.

- Established GDI No. 46 Property Trust post balance sheet date.

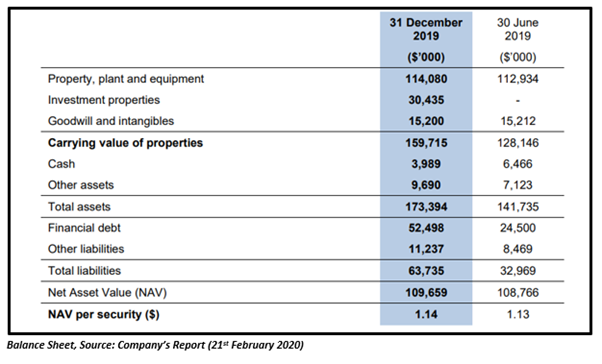

Moreover, the Company reported a Net Tangible Asset (NTA) per security of $1.32 for the period, which was $0.06 per security up from the NTA reported at 30th June 2019.

The Company’s NTA has increased following the revaluation of its Westralia Square and Mill Green, which valued at $316.0 million and $343.0 million, respectively at 31st December 2019. Now, the Company’s portfolio is valued at $759.0 million independently.

In addition, the Company announced:

- Absolute total return of 7.84 per cent for the period.

- Total securityholder return of 9.30 per cent for the half-year

- Covenant Loan to Value ratio of 9.35 per cent.

The Company also declared Funds From Operations (FFO) per security and Distributions per security of 4.397 cents and 3.875 cents, respectively. Consequently, its payout ratio was recorded as 88 per cent of FFO and 114 per cent of Adjusted FFO. The Company’s distribution confirmed its full year guidance of 7.75 cents per stapled security for FY20.

GDI closed the trading session at $1.52 on 24th February 2020, with a fall of ~1.3 per cent.

Aspen Group Continues to Grow on a Profitable Basis

Aspen Group (comprising the Aspen Property Trust and Aspen Group Limited) (ASX:APZ) has recently released solid operational and financial results for the half-year period ended 31st December 2019. Over the half-year, the Company took full advantage of a range of opportunities to offer competitively priced accommodation in the nation’s $7 trillion residential, retirement and short stay sectors.

The value of the Company’s property portfolio rose by 25 per cent over the period to $160 million, especially through acquisition of the Perth Residential Portfolio ($238k per dwelling) and the Lindfield Apartments ($206k per dwelling).

Moreover, its financial performance got materially improved in 1H FY20 relative to 1H FY19:

- Operating profit after tax rose by 55 per cent to $3.66 million or 3.80 cents per security.

- Statutory net profit after tax improved by 319 per cent to $2.29 million.

- Property net operating income rose by 11 per cent to $6.36 million.

- Net corporate overheads fell 15 per cent to $2.42 million.

- Net finance expense rose by 60 per cent to $0.71 million.

- Ordinary distribution improved by 20 per cent to 2.75 cents per security or $2.65 million.

As per the Company, its portfolio is very attractively priced and positions it well to provide competitively priced accommodation to its customers, supported by the following data:

- Property value per approved site at $73,113.

- Weighted Average Cap Rate (WACR) at 8.17 per cent.

Earnings and Distribution Guidance for FY20:

The Company has maintained its earnings and distribution guidance at 6.75 to 7.00 cents and 6 cents per security, respectively for FY20.

The Company notified that its half-year underlying earnings were ahead of budget, while the major bushfire events along the south coast of New South Wales have negatively affected profits at its Tween Waters and Barlings Beach properties by at least $500,000 in late December and January.

The Company will continue to seek opportunities to grow the business and portfolio on a profitable basis in the residential, retirement and short stay sectors.

APZ closed the trading session flat at $1.17 on 24th February 2020.

Lendlease’s Development Pipeline Surges to $112 billion

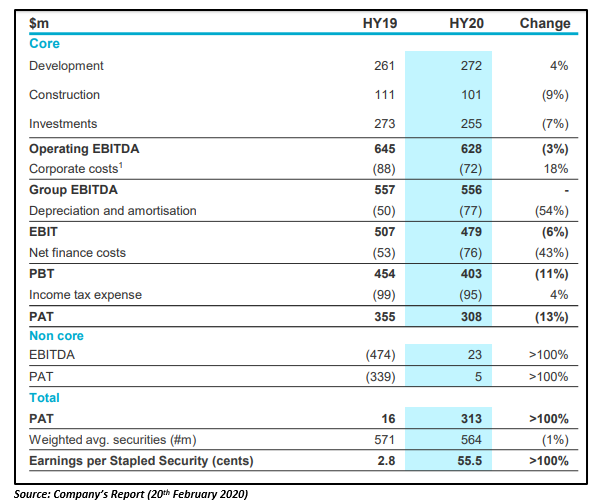

Australia’s leading international property and infrastructure group, Lendlease Group’s (ASX:LLC) development timeline surged to $112 billion over the half-year period ended 31st December 2019, driven by a growing number of major urbanisation projects in its international gateway cities across Europe and the US in particular.

During the period, the Company majorly secured two major urbanisation projects to its portfolio - a partnership with Google in the San Francisco Bay Area and Thamesmead Waterfront in London – which have a combined estimated end development value of over $36 billion.

The other key highlights of the half-year include:

- Urbanisation pipeline of $98 billion comprising 21 major projects in nine global gateway cities.

- Lendlease Global Commercial REIT listed in Singapore.

- Launch of One Sydney Harbour, Barangaroo - $1.4 billion of apartment presales.

- Sale of Engineering business to Acciona agreed for $180 million.

- Developed and published four climate scenarios in line with Taskforce for Climate-related Financial Disclosure (TCFD) recommendation.

- Funds Under Management (FUM) of $37 billion, up 8 per cent on the prior corresponding period.

In addition to reporting solid operational results, the Company delivered strong financial results for the period. The Company notified that a core business profit after tax of $308 million generated a return on equity of 9.6 per cent. Moreover, its gearing was 14.7 per cent, which was the mid point of its 10-20 per cent target range and is anticipated to be between 15 to 20 per cent by the end of FY20.

The Company also reported:

- Development ROIC of 7.3 per cent, which was below 10 to 13 per cent of the target range.

- Construction EBITDA margin of 2.3 per cent, within its 2 to 3 per cent target range.

- Investments ROIC of 10.7 per cent, which was on the top end of 8 to 11 per cent target range.

- 30 cents per stapled security of initial distribution.

- Return on Equity of 9.8 per cent.

The Company seemed to be in a strong financial position, with a liquidity of $3.1 billion.

Going forth, the Company expects to convert a number of commercial and residential opportunities in H2 FY20. In addition, it intends to focus on leveraging its competitive advantage via the urbanisation and investment platforms.

LLC closed the trading session at $19.05 on 24th February 2020, with a fall of ~1.2 per cent.