_06_19_2026_12_34_15_139937.jpg)

Gold has long proven itself as the safest bet among all commodities while offering good returns. Do we have other commodities with risk-rewards like gold? No, but there are a few with good returns in accordance with the risk possessed. With the upsurge in battery storage and consumer electronics, commodities such as Lithium and Nickel are now being accepted in our daily use items.

GOLD

Gold Prices in 2019

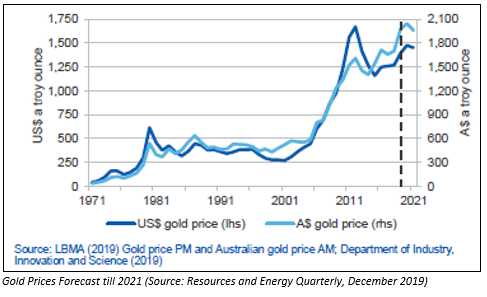

The average London Bullion Market Association (LBMA) gold price hit a six-year high of US$1,558 an ounce on 4 September 2019. However, in the December quarter, the LBMA gold price experienced a 4.5 per cent fall to US$1,488 an ounce when compared with the September figure.

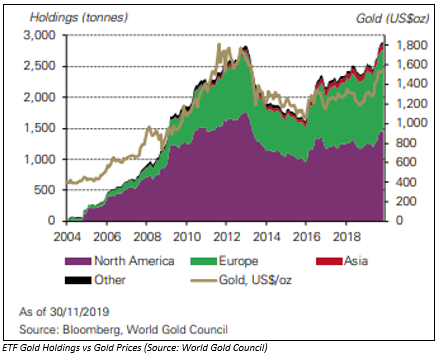

Owing to the steady hold of the Australian dollar against the US dollar, the Australian dollar gold prices have lowered since the record of 3 September 2019. With US-China trade dispute plaguing the entire year, significant inflows in the gold ETF sectors was experienced with the highest ever gold back ETF holding achieved during the year.

Investors have been wary of riskier assets of bulk commodities and equities, due to which they invested their will into gold, leading to multi-year highs for the US dollar gold price and record highs for the Australian dollar gold price during 2019.

Gold Prices in 2020

As markets are still responding to the global economic slowdown, geopolitical issues, problems in the Middle East and civil discord in Hong Kong, the opening of 2020 would be stronger for gold.

Also, recent indications of delayed resolution to the US-China trade war due to the upcoming US Presidential elections and uncertainty over Trump’s second term as the US President would further fuel up the gold market for the rest of 2020.

The same is reflected in the price forecasts from the Chief Economist published in the Resources and Energy Quarterly (December 2019 edition). The gold prices are estimated to reach an average of US$1,474 an ounce in 2020, before falling to an average of US$1,450 an ounce in 2021.

Interesting Read: Gold Price: Unappreciated or Appreciated

Gold Consumption

The global gold consumption rose to 1,108 tonnes during the September quarter, fuelled by the ETF inflows. In fact, October experienced the record gold-backed ETF holdings, followed by a marginal decrease in holdings in November due to outflows from North America and Europe.

The exacerbating US-China trade dispute, slowing global economic growth, and convoluting stance of the US Federal Reserve as it trimmed down the interest rates thrice (July, September and October) in 2019 augmented gold demand in 2019. The investment in gold as a safer bet dominated the consumption sector for gold, which remained weak due to high prices.

As per forecasts by the Chief Economist published in the Resources and Energy Quarterly (December 2019 edition), gold consumption in 2020 would continue to increase, mostly driven by investments from central banks, retail investment and jewellery demand.

Demand for gold in the jewellery sector would grow after a slump in 2019, due to the fast-economic growth, improved consumer sentiment and compulsory branding by Indian jewellery retailers. The record low-interest rate environment and required diversification of central bank reserves would fuel gold demand from central banks.

NICKEL

Nickel Prices in 2019

On 30 August 2019, the government of Indonesia brought forward a ban on nickel ore exports. The new effective date of the ban is 1 January 2020, almost two years before the expected date.

The Indonesian authorities had allowed the export of lower grade nickel (<1.7% Ni) in 2017 at a time when the country lacked infrastructure to process low grade nickel ores to produce high quality products. However, with the commencement of multiple HPAL (high pressure acid leach) projects, the country can now use its low-grade nickel ores to produce high grade cathode material for EV battery.

Indonesia’s export ban has prompted fears of a market deficit. The nickel price averaged at US$16,000 a tonne in the December quarter. The impact of lower production of stainless steel in China resulted as a downward force on nickel prices.

Good Read: ASX-Listed Nickel Miners Charging On The Stock Exchange As Nickel Sets Sail In The Global Market

Nickel Prices in 2020

The Indonesian ban and market deficits would support strong nickel prices. The average price forecast for 2020 and 2021 stands at US$15,800 and US$16,500 a tonne, respectively. The Chinese stainless steel consumption growth and the US-China trade dispute would further impact the nickel industry in the approaching times.

Moreover, the supply to make up for the Indonesian ban (the world’s largest producer), mostly from the Philippines, New Caledonia, Canada and Australia, would decide the changes in market dynamics for the nickel industry.

Nickel Consumption

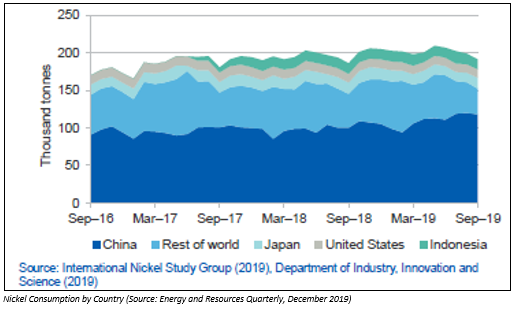

In 2019, global consumption of nickel would grow to 2.4 million tonnes, representing a marginal increase of 2.5% year on year. This is a slower growth as compared to previous years, mostly due to weaker economic conditions, globally.

Nickel consumption for the year till September grew in China by almost 13% year on year due to stainless steel production in the country. However, during the reported nine-month period, nickel consumption fell almost everywhere, primarily on account of lower consumption in Japan and flat consumption in Indonesia.

Nickel consumption would continue to increase at a steady pace, mostly due to higher usage in China. Indonesia banned ores would be used for the domestically developing integrated NPI/FeNi projects such as IMIP, Weda Bay and many more upcoming complexes. Strong demand could be expected from energy storage and electric vehicle markets, with high grade final cathode products from Japan, China and Indonesia.

LITHIUM

Lithium Prices in 2019

Lithium market is experiencing supply glut and would continue to do so. With multiple products of different grades and prices, the impact of the pricing factors depends on the type of the product, destination, and the refinery ramp-ups.

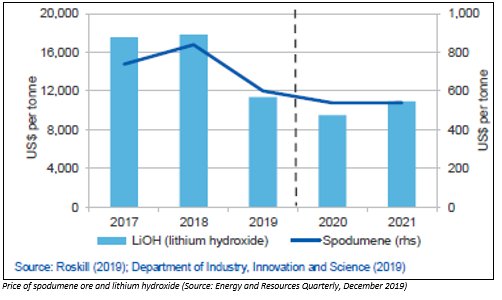

Lithium carbonate spot prices fell drastically to US$7,700 a tonne in November 2019, which included cost, insurance and freight to China. Lithium hydroxide prices vary roughly from US$8,100 a tonne in China to US$12,000 in South Korea and Europe. The spread in prices has led to oversupply in the premium markets.

Spodumene concentrate, a predecessor to the lithium hydroxide product, has experienced a sharp pullback in the supply to ease the downward price pressure and is likely to register an increase in future demand to support long term supplies.

Future Prices

Lithium prices would recover once the demand outpaces the supply. With the cut in supplies and push by producers for better quality of the product, the prices for lithium would grow back in future. Prices are expected in the range of US$9,500 a tonne in 2020 and roughly US$10,925 a tonne in 2021. Meanwhile, the miners are focusing on improving the concentrate product quality, enabling the production of battery-grade lithium products at lower prices.

Lithium Consumption

Consumption of lithium carbonate equivalent stood at 315,000 tonnes in 2019. The consumption would grow at a rapid pace of more than 20% by 2021, majorly due to growing acceptance of electric vehicles and improvements in battery capacity. Increasing battery manufacturing capacity in China and upsurge in trade may involve the combination of lithium hydroxide from brines and spodumene concentrates. Numerous offtake agreements for indirect vertical integration of inputs to manufacturers are taking place.

China, which is the world’s largest electric vehicle market, has experienced a decline in the demand recently due to subsidy cuts to purchase incentives by the Chinese government and a decline in consumer confidence. The lowering of high energy storage battery technology has enabled the carmakers to compete with their products outside the high-end vehicle market.

These are few commodities to look for in 2020 and upcoming years. The macroeconomics and the commodity market dynamics would further decide the play. These commodities would boost up the commodity markets in the near future.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.