1300 Smiles Ltd (ASX:ONT)

1300 Smiles Ltd (ASX: ONT) owns and operates a full-service dental facility in New South Wales, South Australia, and Queensland. ONT is continuously gazing the opportunity to expand its business into other geographical areas throughout Australia. For the purpose, ONT establishes its own operations as well as acquires already established dental practices.

In the past, the company had a conservative approach related to acquisition and very few such events took place in FY15 and FY16. Management changed its stance from FY2017 and embarked on the path of acquisition to strengthen and boost the business. However, management prefers to acquire established practices only when they make positive impact to the result. The same approach is adopted while opening a greenfield site by analysing the local demand, demographic outlook and scalability.

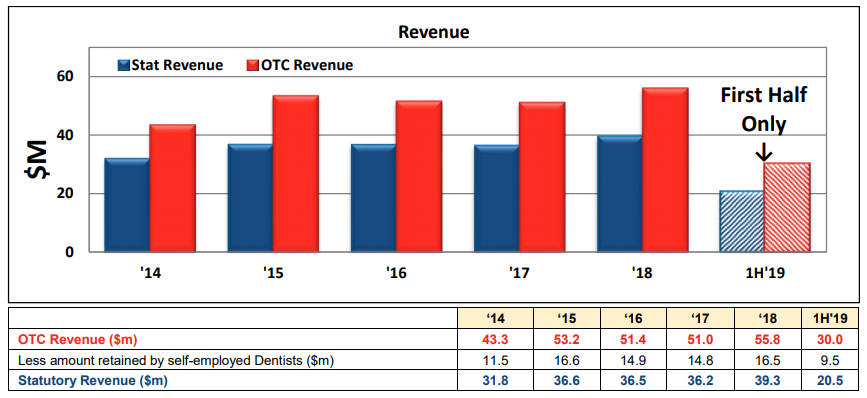

On the financial front, ONT has witnessed a steady revenue path in last few years. If we look at the last 3 years, revenue has gone up significantly to $ 55.8 million in FY18 from $ 43.3 million in FY14 (6.5% CAGR growth).

1HFY19 has seen a remarkable performance and recorded an OTC-Revenue of $ 30 million and statutory revenue at $ 20.5 million on account of strong growth in its long-established practices and newly acquired practices.

Revenue Trend (Source: Company Reports)

EBITDA came in at $ 7.1 million (up 5.7%, yoy) and margins improved to 24% in 1H2019. NPAT at $4.1 million (up 4.3%, yoy) and EPS at 17.3 cents (up 4.3%, yoy) prima-facie paints a strong picture as far as financials are concerned.

Recent Developments: ONT recently acquired two established multi-chair dental practices in Springfield Lakes and Maroochydore to strengthen its geographic position. The acquisition of these two practices will bring growth potential with excellent dental health options in mentioned regions. The acquisition is likely to boost the revenue with approximately $4.5 million and EBITDA margins at 16-18% in the future.

Company has acquired a 5-chair dental practice in the northern Brisbane suburb of Strathpine with the objective of further enhancing its service offering and footprint in South- East Queensland. This acquisition together with the Springfield Lakes and Maroochydore acquisitions will generate additional revenue of ~$6.5 million resulting in the higher margins and profitability to shareholders.

As of now, ONT focuses on to increase the business and profitability and for that matter, the company has been on acquisition spree along with expanding its present facilities to be fully utilised. Going forward, ONT looks at organic growth through its existing locations and by adding new practice management facilities.

ONT has adopted certain benchmarking, training and mentoring to its dentists which leads to an increase in turnover.

ONT has been paying a good dividend to its shareholders. In FY18, the company has announced a final dividend of 12 cents and an interim dividend of 12 cents (fully franked), total at 24 cents. In 1HFY19, company announced an interim dividend of 12.5 cents. At the CMP of A$6.15, dividend yield comes in at 3.98%, and the stock is trading at PE of 18.64x. If we look at the stock performance for one year, ONT has posted a negative return of 4.65%. At the market close (on March 29, 2019), the stock price of 1300 Smiles Ltd (ASX:ONT) was noted at $6.150, with the market capitalization of $145.62 million.

Pacific Smiles Group Limited (ASX:PSQ)

Pacific Smiles Group (ASX: PSQ) is in the business of dental care with independent dentists providing clinical treatments to patients. Fees charged to dentists for these fully serviced dental facilities is the key revenue stream for the business.

Financial Performance: Looking at the key financials, revenue for 1HFY19 came in at $ 59.8 million as compared to $ 50.5 million in 1HFY18 posting a strong upside of 18.5%. This growth can be largely attributed to the new centres opened in FY19 and FY18 along with the strong patient fee growth in same centres which saw a growth of 9% (yoy) in 1HFY19 against 3.3% in 1HFY18. EBITDA grew marginally by 2.5% coming in at $ 11.2 million in 1HFY19 as compared to $ 10.9 million in 1HFY18. EBITDA was adversely impacted by lower than expected fees per appointment and higher than expected telecom infra and connectivity expenditure.

Guidance for FY19: Company has revised its EBITDA growth outlook for FY19 to 5% from 10%. Patient Fee growth outlook has also been revised downward to 12-15% from 10-15%. Same Centre Patient Fee is expected to grow >5%. PSQ intends to open at least 10 new dental centres in FY2019. Dividend pay-out ratio is expected in the range of 70-100%.

Meanwhile, the Stock has underperformed the overall markets and given a negative return of 31.47% (1-year). At CMP of $ 1.165, the stock is trading at PE of 22.4x and dividend yield comes in at 5.24%. Also, the stock is trading at near its 52-week low.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.