Last year, the slowdown in the housing market impacted the performance of various building and material sector companies. Recently, the conditions in the housing market were slightly softened with housing prices increasing in Sydney and Melbourne while auction clearance rates remained high in both cities. The conditions have improved but not significantly enough to improve the outlook of several construction companies.

Boral Limited (ASX: BLD)

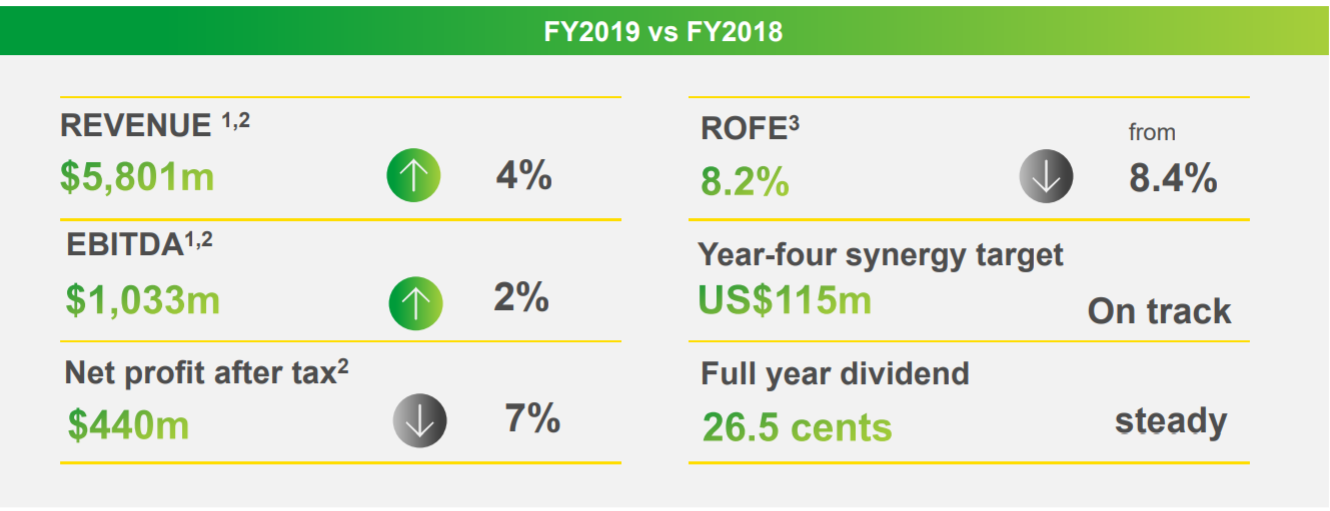

Recently, Australiaâs leading construction material and building supplier, Boral Limited reaffirmed its FY20 guidance which reflected lower earnings and higher depreciation charges. The company said it is expecting its NPAT (before significant items) to be around 5 to 15% lower in FY20 relative to FY19. For FY20, the company expects Property earnings to be around $55 million to $65 million, with a firmer view of the second half expected in February.

In its first quarter of FY20, Boral felt volume pressures and reduced earnings in several of its businesses.

Boralâs business include:

- Boral North America - a leading supplier of building products and largest fly ash marketer in the USA;

- Boral Australia- a leading, vertically integrated construction materials player supplying residential, non-residential and infrastructure construction markets;

- USG Boral- a gypsum-based, interior linings product leader in Asia, Australasia and the Middle East;

In Boral Australia business, the company witnessed lower earnings in the first quarter of trading, with the softer housing market in Australia and delays in infrastructure projects underpinning 8% lower concrete volume relative to last year, and broadly flat asphalt volumes.

Even, the Q1FY20 earnings from Boral North America were slightly lower than the last year. In line with the companyâs expectations, in the Fly Ash business, earnings from site services were lower in the first quarter, mainly due to the completion of a major Synmat construction project, ahead of starting potential new work at other utility sites.

In USG Boral also, the first quarter earnings were slightly lower than last year, due to the slowdown in residential construction in Australia, as well as the continued downturn in South Korea, only partially offset by improvements in Thailand and China.

Last year, the company delivered USD 32 million of synergies from the Headwaters acquisition, slightly ahead of plan, and it is on track to achieve its four-year synergy target of USD 115 million in FY2021.

Source: Company Reports

Boral FY20 Guidance

In FY2020, the company is expecting a 5% EBITDA decline in the first half but expects to deliver a better outcome in the second half.

In Boral Australia, several major projects, including Queens Wharf and Westgate Tunnel projects are expected to ramp up in the second half. The company anticipates additional improvement initiatives of around $40-$50 million from its supply chain optimisation, rightsizing and organisational effectiveness programs.

In Boral North America, both volume growth and price increases are expected to contribute to second half earnings growth â particularly in the fourth quarter, which is seasonally the strongest quarter for the year.

Along with this, a comprehensive improvement program of more than 50 individual initiatives is expected to deliver benefits in FY2020, primarily from January 2020. These include, for example, optimising product weights and mix designs in its concrete roofing business to lower raw material and energy costs, accelerating procurement savings across all businesses, and earlier commissioning of a new Windows production plant in Houston. These initiatives are in addition to the ~USD 20 million of synergies expected in FY2020.

And in USG Boral, the company expect a broadly balanced first half and second half of underlying earnings â prior to the impact of the increased earnings that it will receive following the closure of the transaction with Knauf. The company is of the view that its business is on track to deliver annualised cost savings of around $21 million from Project Horizon by FY2021.

At market close on 6 November 2019, BLD stock was trading at a price of $4.900, down by 3.733% intraday, with a market cap of ~$5.97 billion.

# Holding Company Limited (ASX: WGN)

Innovative Australian construction materials and services provider # Holding Company Limited has advised that its earnings in FY20 are not expected to be materially better or worse than FY19. This company expects its first half results of FY20 to be lower than the second half.

# intends to expand its concrete plant network to ensure that it has more control over the downstream use of its cement, flyash and quarry products.

Last year, the company completed construction and commissioned the wharf at the Pinkenba site, which will give it better access to sea-faring vessels for both incoming and outgoing cargo. This will allow it to take advantage of opportunities to penetrate markets using delivery methods other than its usual road transport.

At market close on 6 November 2019, WGN stock was trading at $1.885, up by 1.072% intraday, with a market cap of $300.97 million.

CSR Limited (ASX: CSR)

Construction and building products provider, CSR Limited (ASX: CSR) recently released its half year results for the six months ending 30 September 2019. The company earned statutory net profit after tax of $68.8 million for the half year, up from $26.8 million in the prior comparable period and Net profit after tax of $71.6 million, down from $89.6 million in the prior comparable period.

The Building Products EBIT in the half year was $95.9 million, down by 18% on pcp, due to the slowdown in residential construction activity. The company earned EBIT (continuing operations) of $113.1 million which is 16 per cent lesser than pcp.

While providing the outlook FY20 (year ending 31 March 2020), the company confirmed that in the medium to longer term, demand for CSRâs building products is expected to be supported by housing activity driven by population growth, high employment and low interest rates.

At market close on 6 November 2019, CSR stock was trading at a price of $4.660, up by 0.215% intraday, with a market cap of ~$2.29 billion. The stock is trading near to its 52 weeks high price of $4.790. Notably, in the past six months, CSR stock has provided a return of 38.39%.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.