The construction sector in Australia is one of the prime growing areas in the country. Factors like population growth, housing, technology, and labour are major contributors to the sectorâs growth in recent times.

As per a trusted industry outlook, the major construction companies are forecasting a continued solid uplift in major non-residential project work over the course of 2019. Growth would be followed by strong non-mining infrastructure aided by the substantial growth push from public sector spending on the transport infrastructure projects.

The Engineering construction would continue to be a key driver of growth with total turnover expected to rise 8% in 2019. Furthermore, there has been notable development on the major road and rail projects backed by public sector spending.

Commercial building activity is anticipated to be strongly positioned in 2019 as well aided by rising private and public sector investment. The total value of the commercial work is anticipated to increase in the higher single digit figures.

Few key private players in the Construction space in Australia are listed under:

- BGC

- ADCO Constructions

- Fulton Hogan

From the listed universe, these are the few construction companies:

Recent updates on two companies catering to the construction space:

- FLETCHER BUILDING LIMITED

With roots dating back to 1909, Fletcher Building Limited (ASX:FBU) functions through seven divisions- Building Products, Concrete, Distribution, Land and Residential Development, Construction, Steel and Australia division. FBU manufactures building products and operates retail businesses that distribute these products and many more to tradespeople. Besides this FBU builds homes, buildings and infrastructure and is listed on the NZX and ASX.

Presently, the company is the only local fully integrated manufacturer of cement (Golden Bay Cement business) in New Zealand.

Company Overview (Source: Companyâs report)

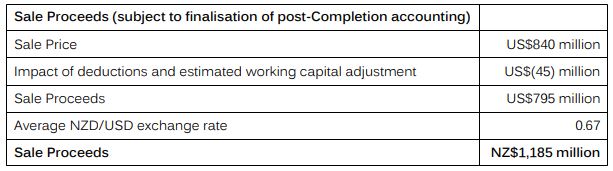

On 4th June 2019, the company announced that it had concluded the sale of the Formica Group to Broadview Holding BV, ahead of its schedule. Below are the details of the sale proceeds:

(Source: Companyâs report)

Commenting on the completion of this sale, CEO Ross Taylor stated that the this was one of the key aspects of the five-year strategy that the company has laid down in June last year, to exit non-core global businesses. This strategy aids FBU to lay its focus on capital and capability behind the Australian New Zealand businesses, with building products and distribution at its core.

The company would be conducting its Investor Day on 26th June 2019, wherein it would provide more insight on the sale.

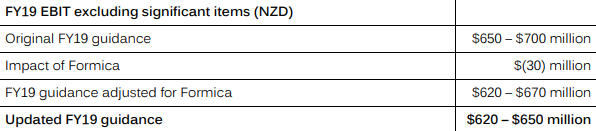

The completion of this sales depicts that FBU would account for eleven months of earnings from the Formica business in the FY2019 result. The FY19 EBIT guidance is provided below:

(Source: Companyâs report)

On May 7th, the company notified about two of its executive team members stepping down from their respective roles in time. Chief Executive Building Products, Michele Kernahan would leave the company at the end of July. John Bell, FBUâs Chief Information Officer, would be stepping down post his retirement and is most likely to leave the company in the 2nd half of 2019.

FBU released its Interim report in February this year. The net earnings were recorded at $89 million for the six months ending 31st December 2018, compared with a loss of $273 million in the first half of FY18. The EBIT was $285 million, compared with a loss of $322 million in its pcp. The earnings for the period were 8% down when compared with EBIT before significant items (adjusted for B+I provision) worth of $309 million in the first half of FY18.

As per the guidance provided by the company for FY19, the EBIT is expected to range between $650 million and $700 million. At the ASM, the earnings guidance provided ranged between $630 million and $680 million. The Formica business (discussed earlier) is the contributor for the $20 million increase in earnings guidance.

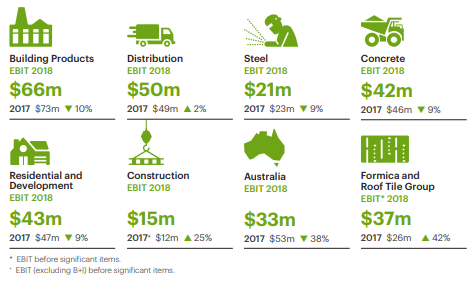

EBIT across the group (Source: Companyâs report)

Share Price Information:

On 5th June 2019, the shares were trading at A$4.930, down by 1.004% compared to its previous close. Its 6-month return has been 10.67% and the YTD stands slightly better at 10.18%.

- SRG GLOBAL LIMITED

SRG Global Limited (ASX: SRG) is an engineering focussed, maintenance, construction, and mining services group functioning across the asset lifecycle. The company headquarters are in Subiaco.

In March 2018 SRG Limited acquired TBS Group and six months post the acquisition, SRG and Global Construction Services Ltd merged to form SRG Global.

On 4th June 2019, the company announced that it had tied a three-year contract renewal with Transpower New Zealand Limited. The renewal was made to deliver specialist industrial services like removal of present coatings via specialist blasting, minor steel replacement and application of industrial protective coatings.

Transpower is the owner and operator of the National Grid, high voltage transmission network across New Zealand, with over 170 substations.

The anticipated revenues (based on historical revenues) under the framework contract were approximately NZ$35 million.

Commenting on the same, Global Managing Director, David Macgeorge stated that contract further reinforced the strong relationship of both the companies.

On 30th May 2019, the company finalised a long-term contract with GFG Liberty OneSteel. According to the deal, SRG would deliver refractory services across the Whyalla Steelworks site. The projectâs scope is inclusive of Installation of refractory products, Gunning and casting of Steelworks materials and Installation of refractory anchors.

The deal is for an initial four-year period and with the option to be extended by 2 years. The proceeds of this are most likely to generate a revenue of almost $45 million across the six-year term or approximately $30 million in the initial four-year term.

Continuing its contract winning spree, the company, announced a long-term contract with South32 Worsley Alumina on 27th May 2019. The three-year initial contract has the option to extend further by three years. In the Worsley Alumina operation, the project scope is inclusive of the provision of engineered access solutions. The revenue anticipated is approximately $32 million in the initial three-year term and around $60 million, subject to the exercise of the extension option.

The company had also secured two contracts worth approximately $17 million with VicRoads and Belhasa Six Construct LLC on 23rd May 2019.

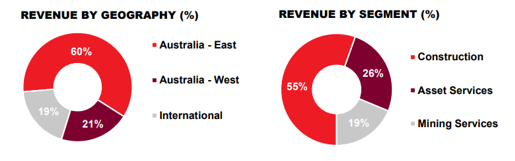

The company presented at the Euroz Conference on 13th March. Below are a couple of snapshots of its highlights from the presentation:

Revenue break-up (Source: Companyâs report)

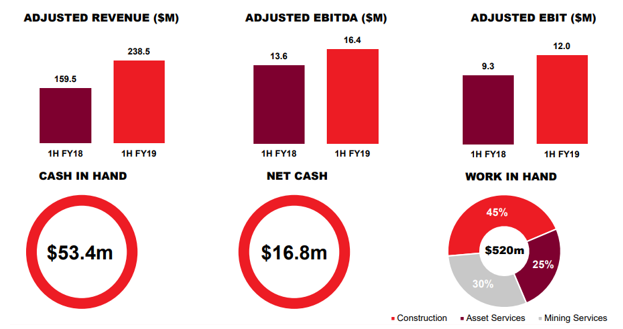

Financial overview (Source: Companyâs report)

Share Price Information:

The stock is trading at A$0.430, up by 3.614% compared to its previous close. Its 6-month return has been negative 19.00% .

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.