Perth-headquartered oil & gas entity, Calima Energy Limited (ASX:CE1) certainly deserves praise for the pace at which it advanced the Calima Lands towards a development ready project. Calima Lands is one of the Company’s key assets situated within a liquids-rich sweet-spot of the Montney Formation in NE British Columbia (BC), the most active oil & gas play in Canada.

Calima owns and operates 100 per cent stake in 63,103 acres of Montney drilling rights in BC. The Company has so far made remarkable progress at Calima Lands, in line with its overarching strategy focused on creating value for shareholders via:

In this regard, let us discuss the Calima Lands timeline since its acquisition in 2017 below:

2017: Acquisition of Calima Lands

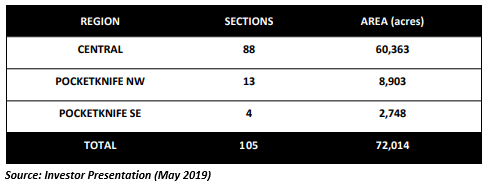

As a consequence of its successful bids in the December 2017 government land auction, Calima’s core acreage holding in NE British Columbia grew to 72,014 acres of drilling rights (105 drilling sections) over acreage believed to be highly prospective for the Montney Formation.

This led to the completion of Calima’s acreage acquisition strategy, post which the Company shifted its focus towards all the operational work required to drill wells optimally located and created to demonstrate the value of the Calima Lands.

The strategy finalisation also enabled Calima to commission a leading Canadian reserves auditor, McDaniel & Associates Ltd to undertake a resource assessment of the Calima Lands.

It is important to note that about 7,542 acres of drilling rights in areas, referred to as Pocketknife expired prior to 31st December 2019. The Company let these areas expire in due course, as these areas were likely to be expensive to include in a field development plan, owing to their shape and separation from the contiguous core region.

2019: Successful Completion of Drilling Operations

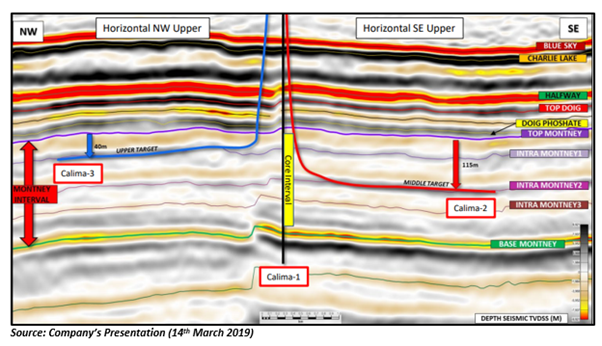

Calima successfully completed a three-well drilling campaign (9,353m) in 2019, with its drilling team delivering the performance that matched with best-in-class drilling performance of other operators in the area.

Three wells (1 x vertical – Calima-1, 2x horizontal – Calima-2 and Calima-3) were drilled as part of the campaign, and the results exceeded Calima’s expectations, which included:

- Top quartile performance relative to the peer group, reflected by initial production test results (1,640boe/d)

- Maximum gas rate 10.2 mmcf/d

- Calima-2 condensate gas ratio exceeded 40 bbl/mmcf and climbed after the initial clean out

In an independent review of the drilling results, GLJ Petroleum Consultants noted that the Company’s focus on intense simulation facilitated the Calima-2 well to attain above-average performance. Moreover, the consultants observed the following:

- Calima-2 well is anticipated to meet or exceed the performance of adjacent wells. This is true both in terms of liquid yield and in terms of overall production performance (like gas production rate).

- The total gas test rate from the Calima-2 well compares favourably to other liquids-rich wells.

Success of the three-well drilling campaign allowed Calima to convert approximately 60 per cent of its core acreage (49 sections of land) to 10-year production leases, covering 33,643 acres. Most of the remaining licences over the Core Lands are likely to mature over 2021/22.

Q3 2019: Finalisation of Resource Update

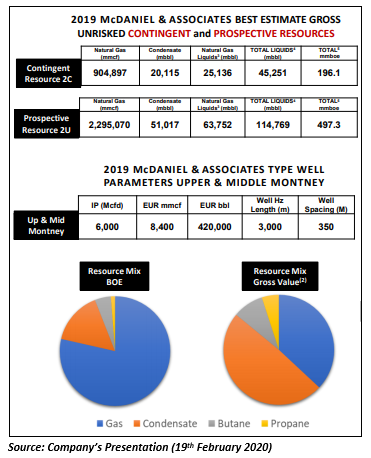

Finalising resource assessment of the Calima Lands, McDaniel updated Independent Resource in July 2019, reporting best estimate gross un-risked prospective resources (2U) of 497.3 Mmboe plus the addition of best estimate gross un-risked contingent resources (2C) of 196.1 Mmboe.

The McDaniel report projected that ~77 per cent of production in terms of barrels of oil equivalent (boe) from the Calima Lands would be gas and ~50 per cent of the value in terms of barrels of oil equivalent (boe) would come from condensate. Besides, the report assessed Estimated Ultimate Recovery (EUR) at 8.4 Bcf and 420,000 bbl per well. Calima Lands project economics are bolstered by condensate, while gas price poses leverage.

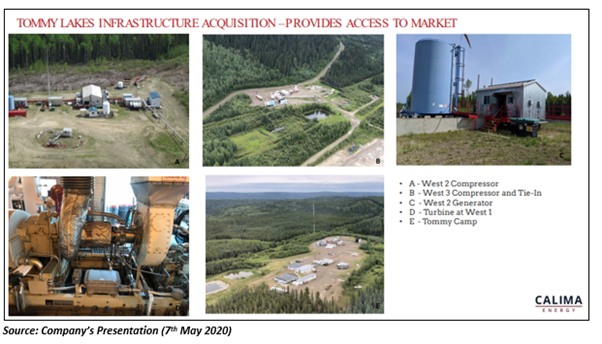

Q1 2020: Acquisition of Infrastructure

Calima successfully acquired Tommy Lakes Infrastructure, including pipelines and facilities in Q1 2020, materially under budget at a cost of $750k, with holding cost anticipated to be at $500k per annum.

The acquisition provided the Company with a cost-effective connection to NorthRiver pipeline and processing facilities and from there to major pipeline networks like NGTL, Alliance and T-North.

Notably, Calima also has a regulatory approval to construct and operate a 19.5 km steel 8-inch service pipeline, connecting existing and future Calima wells to the Tommy Lakes Field West 2 compressor facilities.

The fully permitted facilities, comprising liquids stripping, compression, and associated pipelines, are capable of transporting as much as 50 mmcf/d of gas and 2,500 bbls/d of condensate prior to expansion.

Moreover, the re-use of current facilities provides cost and time savings with minimum environmental impact. Calima also has an option to acquire eleven producing wells that could deliver fuel gas for the start-up phase of production.

Tommy Lakes Infrastructure acquisition has elevated the Calima Lands to become a development ready project, inching Calima Energy closer to a Final Investment Decision. Besides, 2C Contingent Resources of 196.1 Mmboe and 2U Prospective Resources of 497.3 Mmboe strengthens the Company’s position to progress with its strategy focused on realising value for shareholders from its exciting assets.

CE1 closed the trading session at $0.006 on 21st May 2020.

Must Read! Calima Energy Releases May 2020 Investor Presentation, Outlines Strengths of Canada O&G Industry