With the slowdown in various global economies, consumer staple companies are considered a safe haven due to their defensive business model. If in the future economic tough times hit, people are not going to stop buying food, drinks, washing powder or razors. However, it might be considered beneficial for companies like Woolworths, Coles and Metacash as customers may get attracted to discount retail stores. These can be considered a recession-proof company and can provide safe returns to their shareholders by protecting them from bear markets with limited volatility in stock price and stable dividends payouts.

Woolworths Group Limited

About the company: Woolworths Group Limited (ASX:WOW) primarily operates in Australia and New Zealand, with 3,292 stores and approximately 196,000 employees. The primary activities in which the company is involved are:

- Australian Food: Operating 1,024 Woolworths Supermarket and Metros

- Endeavour drinks: Operating 1,577 stores under Dan Murphyâs, BWS, and Summergate brands. The group also operates Cellarmasters, Langton and winemarket.com.au online platforms.

- New Zealand Food: Operating 189 Countdown Supermarkets as well as a wholesale operation which supplies a further 69 stores.

- Big W: Operating 183 BIG W stores.

- Hotels: Operating 328 hotels, including bars, dining, gaming, accommodation and venue hire operations.

Planning to close some stores: Woolworths is planning to close approximately its 30 Big W and DC stores as the segment showed an EBIT loss of $85 million as compared to the previous year loss of $110 million.

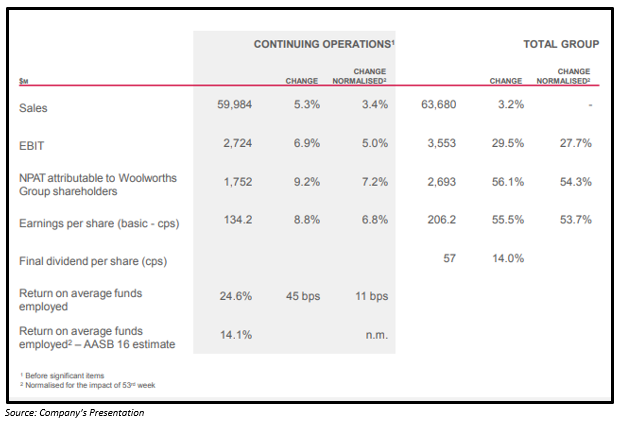

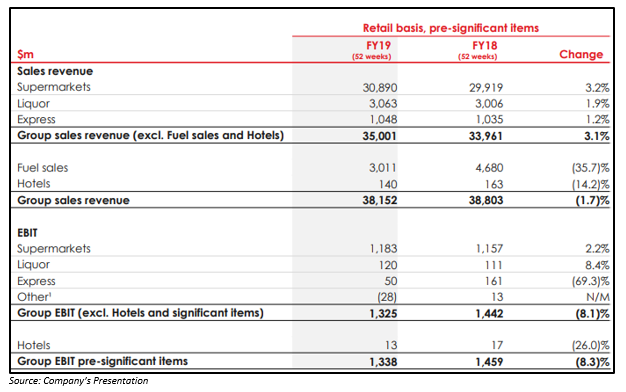

FY19 Results Highlights: Company reported a good set of numbers with sales increasing 3.4% to $59,984 million. EBIT from operations increased by 5% to $2,724 million. NPAT from operations increased by 7.2% to $1,752 million. On a segmental basis, Australian Food ended FY19 with good momentum after sluggish growth in H1. H2 sales increased by 3.9%, resulting in full-year sales increase of 3.1%. EBIT improved by 3.8% for the year and New Zealand Food had a strong 2nd half with a growth of 3.6% and H2 EBIT growth of 4.4%. Supported by the establishment of CountdownX, this segment delivered strong online sales growth of 40% in FY19. With refreshed strategy and settled weather, Endeavour Drinks reported an improved H2. Endeavour Drinks normalised FY19 EBIT declined by 9.7% partly impacted by non-cash impairment charges related to Summergate.

Woolworths has declared a final dividend of 57 cents up by 14% as compared to the previous year on account of good net profit growth of 8.5%. The stock at its current price is providing a dividend yield of 2.74%.

Stock Performance: On 3 September 2019, the stock of WOW closed the trade at a price of AUD 36.710, down by 1.432% as compared to its previous closing price, The stock is currently trading near its 52-week high of AUD 38.06, with a market cap of around AUD 46.87 billion and approximately 1.26 billion outstanding shares. The company is trading at a PE multiple of 18.06x. In the previous six months, the company has given a total return of 27%.

COLES Group Limited

About the company: Coles Group Limited (ASX:COL) is an Australian based company that operates predominantly in the retail industry. The company sells various products including fresh food, groceries, liquor, household goods, fuel and financial services via its store network and online platforms. The company operates through 3 divisions: Coles Supermarkets, Coles Liquor and Coles Convenience. The primary activities in which the company is involved are:

- Coles Supermarkets: Coles Supermarkets is a national full-service supermarket retailer operating more than 800 supermarkets.

- Coles Liquor: Coles Liquor is a nationwide liquor retailer with 900 stores trading as liquor land, vintage cellars, first choice liquor and first choice liquor market and an online liquor retail offer.

- Coles Express: Coles Express is one of Australiaâs leading fuel and convenience retailer, spread over 700 locations throughout the country.

FY19 Results Highlights: The company reported a good set of numbers with the sales revenue increasing by 3.1% to $35 billion. Supermarket segment was the biggest contributor in the segment with 88% in the revenues and it grew by 3.2%. Gross margin increased by 20 bps due to strategic sourcing and continued execution of Own Brand strategy. Segment EBIT increased by 2.2% driven by better sales and enhanced gross margins. Liquor and Express sales were flat in the year with a marginal upside of 1.9% and 1.2% respectively. However, liquor segmentâs gross margins jumped to 22.3% due to margin improvements from improved supplier collaboration and Exclusive Liquor Brand. Online sales grew by 30% as compared to the previous year, generating a revenue of $1.1 billion.

As a public company Coles declared its first ever dividend of 35.5 cents per share comprising a final dividend of 24 cents per share and a special dividend of 11.5 cents per share.

New initiatives: The company is planning to renew its 51 supermarkets, 52 liquor stores and 259 Coles Express including food to go (FTG) roll-out. It is planning to open new 22 supermarkets and 27 liquor stores. After its robust growth in online segment, the company is planning to expand its 120 Click and Collect locations.

Stock Performance: On 3 September 2019, the stock of COL closed the dayâs trade at a price of AUD 14.150, trading near to the 52-week high of 14.268, with a market cap of around AUD 18.53 billion and approximately 18.53 billion outstanding shares. The company is trading at a PE multiple of 12.91x. In the previous six months, the company has given a total return of 23%.

Metcash Limited

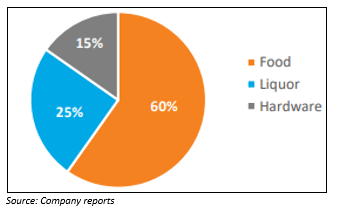

About the company: Metcash Limited (ASX:MTS) is Australiaâs leading wholesaler and distributor, supplying approximately 5,000 independent retailers which form part of bannered network and several other un-bannered businesses across the food, liquor and hardware sectors. The Companyâs segments include Food and Grocery, Liquor and Hardware.

The Group employs over 6,000 people and indirectly supports employment in independent retail networks.

FY19 Results highlights: Metcash reported flat yearly numbers for FY19 with sales at $14,563 million, which were up by 1.4% annually. Main growth was seen in the liquor division, which was up by 5.6% to $3,666 million. Food segment sales were flat for the year and the Hardware segment saw its sales dip by 0.9% to $2,102.0.

Revenue contribution from different segments:

In the supermarket segment, the total sales declined by 0.5% to $7.2 billion however in the convenience segment the total sales increased by 4.4% to $1.6 billion due to sales growth from major customers, increased tobacco sales and the addition of new customers. The total hardware sales declined by 0.9% to $2.1 billion negatively impacted by 1) Slowdown in construction activity, 2) Loss of large HTH customer in QLD in H1FY19 and 3) Net closure of stores.

The Group declared a final dividend of 7 cents per share with total dividends of 13.5 cents for FY19. The company has a dividend payout ratio of 60%. The stock at the current price is providing a healthy dividend yield of 4.75%.

Outlook for FY20: Metcash has entered into a 5-year supply contract with Drakes Supermarkets. Supermarkets will continue to invest in growth initiatives through the MFuture program, which will help cost savings in FY20 to offset inflation in the Food pillars. Continuation of the âpremiumisationâ consumption trend is expected to be the key driver of market growth in FY20 for liquor division.

Stock Performance: On 3 September 2019, the stock of MTS closed the dayâs trade at a price of AUD 2.83, with a market cap of around AUD 2.58 billion and approximately 909.26 million outstanding shares. The company is trading at a PE multiple of 13.65x. The company has given a total return of 19% on a YTD basis.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.