Spark Infrastructure Group (ASX: SKI) deliver safe and reliable electricity to Australian homes and businesses. Today, the company held its Annual General Meeting in which all 7 resolutions were passed via Shareholders voting.

While addressing the shareholders at the AGM, the companyâs Chairman Dr. Doug McTaggart told that Spark Infrastructure Group is well placed to take advantage of the rise of renewables, from more interconnection and from new technologies to enhance the stability and performance of the grid.

Currently, there are three key trends which are expanding role of networks.

- Retirement of coal-fired generation and significant large scale renewable energy build

- More interconnection required to balance intermittent generation across regions

- Solar rooftop PV, batteries and electric vehicles declining in cost and improving customer choice

The companyâs vision is to create long-term value through capital growth and distributions for Securityholders from its portfolio of high-quality, long-life essential service infrastructure assets.

The company has refreshed its strategy to position itself to take advantage of the accretive growth opportunities. While providing an update on the companyâs asset in the energy supply chain, the chairman informed that Spark Infrastructure is a leading listed owner of essential service infrastructure in Australia. The company has interests in some $17 billion of energy network assets in total, delivering energy to more than 5.6 million customers across Victoria, South Australia, New South Wales and the Australian Capital Territory, in addition to transporting electricity across the National Electricity Market (NEM) to other states.

The companyâs assets have been ranked as among the most efficient networks in Australia. This efficiency allows the company to pass on savings in the network component of electricity prices to millions of Australians, with real price reductions to customers during Spark Infrastructureâs ownership. These benefits are also shared with the companyâs Securityholders through outperformance of financial incentives.

The companyâs Board has adjusted the outlook for distributions for 2019 to account for the pro-forma tax impost to its businesses in 2019 assuming that these amounts are taxable in accordance with the decision. It is expected that the company will become a taxpayer in short term. The Board has issued a revised distribution guidance of at least 15.0 cents per security for 2019, subject to business conditions.

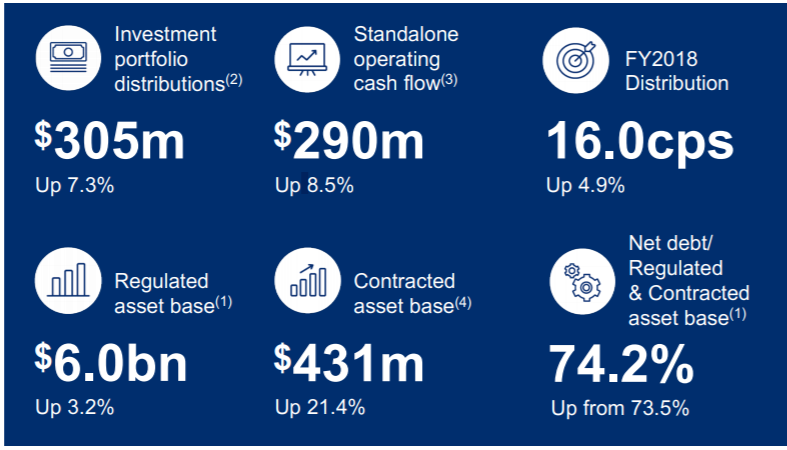

In FY 2018, the company reported Adjusted proportional EBITDA of $825 million, up 4.8% on the previous corresponding period (pcp). At the end of 2018, the company had a standalone operating cash flow of $290 million, up 8.5% on pcp.

2018 Financial Highlights (Source: Company Reports)

2018 Financial Highlights (Source: Company Reports)

In the last one year, the share price of the company increased by 4.44% as on 23 May 2019. At the time of writing, i.e., on 24 May 2019, the stock of the company closed the dayâs trade at a price of A$2.340, down 0.426% during the dayâs trade with the market capitalisation of ~A$3.95 Bn.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.