Based in Subiaco, Western Australia, Calima Energy Limited (ASX: CE1) is an international oil & gas (O&G) company, engaged in making investments in O&G exploration and production projects, globally. CE1’s primary assets lie within the Montney Formation, British Columbia, where the company owns and operates 100% interest in 72 thousand acres of drilling rights (Calima Lands).

Good Read: All That Investors Need to Know About International O&G Company, Calima Energy Limited

Three-Well Drilling Program Delivers Successful Testing Results

The company undertook a three-well drilling program in the region including one vertical well and two horizontal wells. Drilling of the vertical well was targeted to measure and analyse the rock samples and later to move to horizontal wells to check the production rate. The result of drilling astonished with a condensate-gas-ratio (CGR) of 20.06 bbl/mmcf with a peak hourly value of 22.15 bbl/mmcf through a choke size of 38.1mm from the first horizontal well.

Whereas, test simulation of the second horizontal well showed consistency with the first horizontal well, indicating healthier productive potential from both the wells. The three wells provided unequivocal confirmation of the extension of the liquids-rich fairway through the Calima Lands in both the Upper and Middle Montney targets.

Moreover, initial production test results from one of the horizontal wells delivered top quartile performance against the peer group.

For more information on drilling, please read “Turning Focus on Calima Energy’s Highly Prospective Montney Project.”

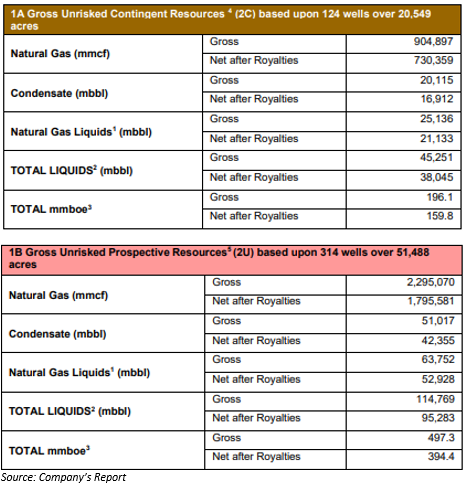

Significant Resource Increase for Calima Lands

Independent geological consulting firm, McDaniel & Associates also revised the gross un-risked resource for the Calima Lands, with total contingency resources (2C) increased to 196.1 mmboe and prospective resources (2U) to 497.3 mmboe including royalties, as of July 2019. The net resources after royalty stood at 159.8 mmboe for 2C and 394.4 mmboe for 2U.

Permit for Pipeline Construction

The strike to commercialisation was made with the approval for pipeline construction to connect existing and future Calima wells to the regional sales network. With upfront capital expenditure of ~C$17 million for the pipeline project expected to deliver up to 50 mmcf/d of wet gas and 1,500 bbls/d of well-head condensate. The further discussion related to project economy depends on the completion of the Field Development Plan (FDP).

In line with its strategy to focus on the Montney Project, the company has planned to sell all or part of its four offshore Production Sharing Contracts (PSCs) in Saharawi Arab Democratic Republic (SADR) at a value higher than AUD 0.132 million. Moreover, Calima Energy has plans to sell Bahari Shares at an amount higher than AUD 1.32 million.

As of September 2019, the company remains well funded with the working capital position of AUD 5.6 million, including recent receipt of AUD 2.9 million from the sale of the Namibia PEL 90 licence (Block 2813B) and Canadian GST receivable of ~AUD 1.3 million due in February 2020. Also, in July 2019, CE1 announced a capital raising of AUD 12.7 million through a placement worth AUD 4 million and a fully underwritten entitlement offer valued at AUD 8.7 million, both at AUD 0.018 per share.

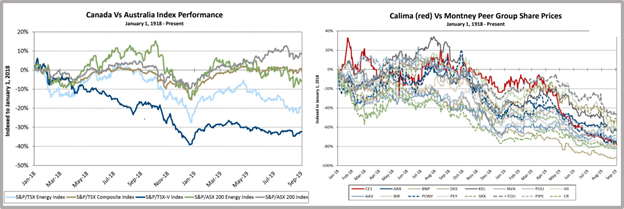

Calima and Canadian Market

As of end of the September 2019 quarter, Canadian exploration & production stocks witnessed decline due to lack of pipeline capacity and government policies along with US vested interest lobbying, resulting in discounted oil & gas prices.

Source: Company Finance News Network Investor Event Presentation

Calima's share price performed in line with the peer group in the Montney region. In comparison to the other big plays in the US, Calima Lands has more productivity and lower drilling cost except for the shortage of outlet capacity of the pipeline, which may increase the total selling cost.

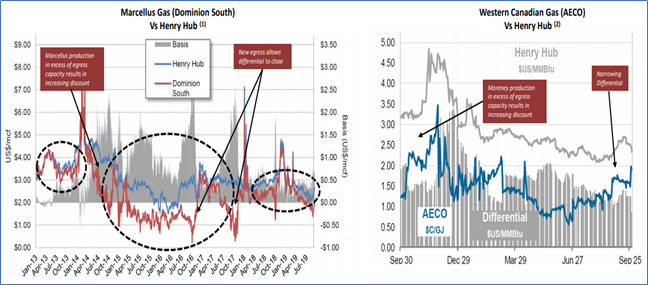

The region has two pipelines connecting to the market, i.e. Marcellus Gas (Dominion South) and Henry Hub. The supply has exceeded the capacity at Dominion South, leading to a decrease in price. Though at Henry Hub the prices increased, making Montney profitable as shown below.

Source: Company Finance News Network Investor Event Presentation

Current production stands at 7bcf/d and 400,000 bbl/d of condensate and NGL at the Montney Formation, which is likely to increase by 12-13bcf/d in the next seven years with new projects and pipelines.

Globally, oil demand is expected to grow by 1.2 mn b/d, due to the growth of world GDP to 3.4% in 2020 from 3% in 2019, projected by the IEA based on a prediction of International Monetary Fund on GDP outlook, and oil oversupply of 0.3 mn b/d is expected in 2020.

The above obstacles of egress capacity and oversupply may not affect the CE1 performance, courtesy to anticipated pipeline construction and over 70% gas production in Calima Lands, thereby triggering a positive near-term outlook for the company.

Stock Price Information – The stock of CE1 closed the day’s trading at AUD 0.008 on 3 January 2020 with a market cap of AUD 17.24 million.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. The above article is sponsored but NOT a solicitation or recommendation to buy, sell or hold the stock of the company (or companies) under discussion. We are neither licensed nor qualified to provide investment advice through this platform.