?If we overuse one factor of production, keeping other inputs fixed, the productivity initially increases then flattens, declining sharply after a certain point.? This is termed as the law of diminishing marginal productivity, that is commonly considered by leaders in productivity management.

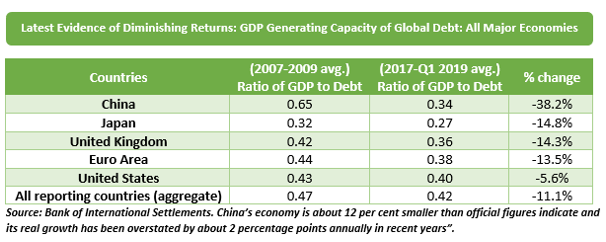

A similar pattern has been observed in real GDP of the world?s major economies as their GDP generating capacity of debt is diminishing rapidly (see figure below).

It has been observed that from 2017 to Q1 2019, each dollar of global debt produced only $0.42 of GDP growth in the world?s major economies, that was 11.1 per cent down than the previous ten years? data.

The decline in the US was comparatively less than all the major foreign economies, indicating that the country is at a far better position than the rest of the world in terms of debt productivity. ?Each dollar of debt generated $0.40 of GDP growth in the US, which was higher than the Euro Area, United Kingdom, Japan and China.

Besides debt productivity, there are many other macroeconomic indicators that help market experts assess the health of an economy. Considering this, let us discuss some updates on different macroeconomic indicators in the major economies of the world:

Australia

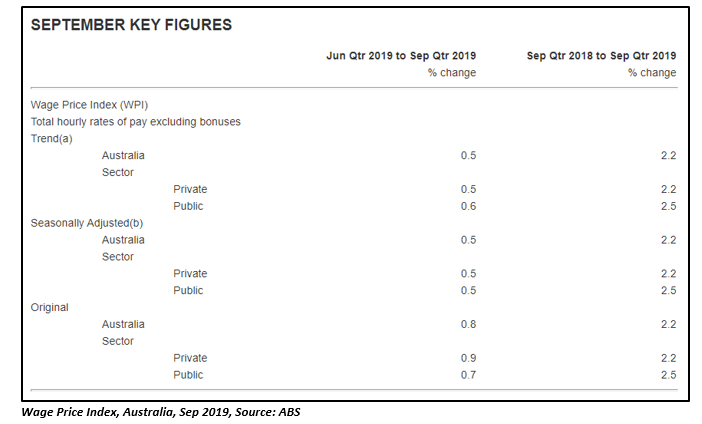

As per a recently announced data by the Australian Bureau of Statistics (ABS), the wage price index rose 2.2 per cent through the year to the September quarter 2019 in seasonally adjusted terms. Though the wage growth of 2.2 per cent was lower than the 2.3 per cent growth seen in the year to the June quarter, it was in line with economists' forecasts.

The wage price index is a leading indicator of consumer inflation as when businesses pay more for labour; the higher costs are usually passed on to the consumer.

The recent data indicate that Australia saw a wage growth of 0.5 per cent in the September quarter, with an increase of 0.9 per cent and 0.7 per cent in Private and Public sector indexes, respectively. During the quarter, Tasmania recorded the sharpest quarterly rise of 1.3 per cent, while Western Australia noted the lowest quarterly increase of 0.7 per cent.

The wage growth in the quarter was primarily influenced by the end of financial year salary reviews for individual arrangements, regularly scheduled enterprise agreement rises, and a surge in modern awards receiving as a result of the Fair Work Commission Annual Wage Review (3.0 per cent in the 2018-19 decision).

?

?

United States

A recently announced ISM non-manufacturing PMI indicated a solid pick up in the non-manufacturing economic activity of the US in October 2019. The index reported was well ahead of market expectations (53.5) at 54.7 for the month.

Non-manufacturing PMI is a major indicator of economic health as businesses respond quickly to market circumstances, and their purchasing managers usually holds the most recent and appropriate insight into the firm?s view of the economy.

Small Business Optimism Index also showed an improvement in small-business owners' confidence in the country?s economy in October 2019. The NFIB Small Business Optimism Index was 0.6 point up on the previous month, to 102.4 in October 2019. The result was 0.1 points higher than the forecasts of 102.3 points. The October rise was influenced by GDP-producing plans for inventory investment, job creation and capital spending.

Moreover, the continued efforts of the White House to close the gap in goods and services contracted the country?s deficit to $52.5 billion in September, according to recently released data by the US Commerce Department.

The contraction in the trade deficit was driven by the US-China move towards the tariff truce. In October this year, the US agreed to remove the existing tariffs on China under phase one deal, under which Beijing was supposed to request cancellation of some proposed and current US tariffs on Chinese imports. In return, China was likely to promise to step up its purchases of US agricultural products.

However, the US President, Donald Trump, has recently warned of raising tariffs on Chinese goods if the two countries don?t make a deal. Though the President is not clearly denying the occurrence of the significant phase-one deal, he mentioned that the deal will only be accepted if it's good for the US, its workers and its great businesses.

Japan

Japan?s Producer Price Index (PPI) dropped by 0.4 per cent year-on-year (y-o-y) in October 2019, against market expectations of 0.3 per cent fall. Previously, the PPI fell by 1.1 per cent over the year to September 2019. The PPI rose 1.1 per cent month-on-month in October, 0.1 per cent less than the forecasts of 0.2 per cent growth.

The Producer Price Index is usually considered as one of the leading indicators of consumer inflation, arising from the fact that when corporations raise the price of their goods, the higher costs are usually passed on to the consumer.

New Zealand

Against market expectations, the Reserve Bank of New Zealand has kept the benchmark interest rate steady at 1.0 per cent. Short term interest rates are the paramount factor in currency valuation, and traders mostly look at other indicators just to predict how rates will change in the future.

Majority of the economists were anticipating a quarter-percentage point cut in the official cash rate. The decision was taken to balance the need to stimulate inflation against fresh signs of stabilization in the global and domestic economies.

In addition to interest rate, the Food Price Index (FPI) for October 2019 was also announced by Stats NZ, which indicated a rise of 0.6 per cent in food prices in seasonally adjusted terms. Fruit and vegetable prices in the country were 1.2 per cent up after seasonal adjustment relative to September 2019.

Although food is among the most volatile consumer price components, this indicator garners some attention because New Zealand's major inflation data is released on a quarterly basis.

Euro Area

The ZEW Indicator of Economic Sentiment that reviews the economic conditions of Germany and other nations in Europe, jumped 20.7 points to -2.1 in November 2019 relative to October. The ZEW Economic Sentiment notably improved, beating market expectations of -13.2.

Eurozone ZEW Economic Sentiment also climbed swiftly to -1.0, greater than -23.5 observed in October, beating expectation of -11.5.

Positive sentiment was credited to the improved potential for an enhancement in international economic policy and softer Brexit negotiations between the EU and the UK.

United Kingdom

The recently released official figures by the Office for National Statistics (ONS) demonstrated a decline in British unemployment to 3.8 per cent in the September quarter, driven by a fall of 58,000 people in employment. This was the biggest quarterly fall observed by the nation since 2015.

As per market experts, the employment in the nation has dropped at its sharpest rate in four years in the midst of mounting evidence that a decelerating economy is taking its toll on the UK labour market.

The data may induce the Bank of England to cut the official interest rates in the near future, expect market experts.

In addition to these indicators, investors are closely eying the upcoming CPI and retail sales data for the UK and GDP figures for Germany.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.