US Markets: Three major American stock averages slipped sharply on Friday, 10 December, erasing most of the morning gains after the annual inflation rate in the United States jumped to the highest level in the last 39-and-half years. Dow Industrials, Nasdaq Composite and S&P 500 started on a positive footing, declined from respective intraday peaks after the US Bureau of Labor Statistics declared the rate of inflation accelerating to 6.8% in the month of November 2021.

This has been the highest reading since June of 1982, but the outcome was widely anticipated. November has been the ninth straight month when the rate of inflation in the US has remained well above the 2% target determined by the US Federal Reserve. Markets recovered partly as the trading progressed in mid-morning deals as inflation rate stood in the range of street estimates.

In the early morning trades, Dow Industrials advanced 100 points, with the tech leader Nasdaq Composite and broader share indicator S&P 500 rising over 0.5% each. The rate of inflation approaching near 40-year high certainly intensifies the case for the Federal Open Market Committee to escalate the speed of tapering of its ongoing bond buying programme. The US Federal Reserve is slated to announce the decision on key interest rates and the precautionary measures to contain the boiling rate of inflation on Wednesday, 15 December.

The Dow Jones Industrial Average traded 59.33 points, or 0.17% higher at 35,814.02, the technology heavy market index Nasdaq Composite added 49.93 points, or 0.32% to 15,567.30, whereas the wider share barometer S&P 500 rose 17.74 points, or 0.38% to 4,685.19.

US Market News: Amid the components of Dow Jones Industrial Average, shares of Cisco Systems, Microsoft, Salesforce.com, Apple, Coca-Cola and Honeywell International gained 1-3%, while the heavyweight constituents including Goldman Sachs, Chevron and Boeing lost 1-2%, partly offsetting the positive point contribution extended by the aforementioned stocks.

Even with a moderate gain and back-to-back muted sessions in the last three days including today, the leading Wall Street indices are on track to register a gain of nearly 3% with Dow Industrials and S&P 500 leading the rise and Nasdaq Composite finishing with an approximate surge of 3%.

With the announcement of inflation data, the market participants have shifted their focus to the policy decisions taken by the FOMC next week and a slew of major macroeconomic data points set to be announced by 17 December.

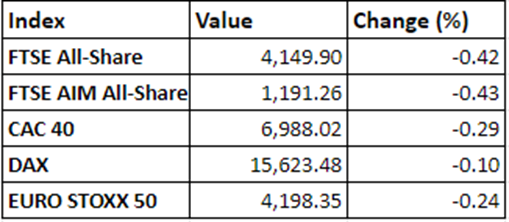

UK Markets: Taking the cues from the lacklustre Wall Street session, London equities dived deeper into the negative region with the domestic benchmark index FTSE 100 losing the psychological level of 7,300 in the terminal trades on Friday. Irrespective of volatile trading activity in the last three sessions, FTSE 100 remains on track to post a weekly jump of a little more than 2%.

Shares of British American Tobacco advanced more than 2%, emerging as the lead gainers today, while the stock of Darktrace collapsed 3% as the corporation enjoys terminal days of its inclusion in the prestigious FTSE 100 index. The stock of the market capitalisation leader AstraZeneca crashed more than 2%, effectively wiping out most of the positive points contributed by other fellow constituents.

FTSE 100 (10 December)

Source: EODHD/Others

Market Snapshot

Top 3 volume leaders:, Vodafone Group, Lloyds Banking Group, and BP

Top 3 sectoral indices: Tobacco, Finance Services, and Food Products

Bottom 3 sectoral indices: Automotive, Medicine and Biotech, and Consumer Services

Crude oil prices: Brent crude up 0.71% at $74.97/barrel; US WTI crude up 0.59% at $71.36/barrel

Gold prices: An ounce of gold traded at $1,784.25, up 0.42%

Exchange rate: GBP vs USD - 1.3230, up 0.08% | GBP vs EUR - 1.1704, up 0.00%

Bond yields: US 10-Year Treasury yield - 1.463% | UK 10-Year Government Bond yield - 0.7280%

Markets @ 16:00 GMT

© 2021 Kalkine Media®