US Markets: Wall Street started on a vibrant note on the second day of new year 2022 with the broader benchmark S&P 500 and Dow Jones Industrial Average hitting fresh record highs on Tuesday, 4 January, 2022, led by the market-wide optimism of comprehensive economic recovery in the fresh 12-month stretch. The wider share indicator strengthened over the psychological level of 4,800, while the 30-component heavy Dow Industrials breached 36,800 for the first time ever.

With the present market dynamics and renewed investors’ optimism, the leading stock indicators are set to register fresh peaks in the present quarter. The buying is likely to escalate in the upcoming weeks as market participants will continue to accumulate the heavyweight constituents before the commencement of the fourth quarter and full year corporate earnings cycle.

Alongside the major financial results, the macroeconomic data points detailing the prospective effect of the Omicron variant in the December of 2021 will be closely observed by the market participants.

The previous calendar year has been one of the most positive years for American equities as the leading stock averages not only strengthened over the pre-Covid peaks, but the three majors including the tech-heavy Nasdaq Composite, Dow Jones and S&P 500 also made record highs on multiple instances, effectively reinstating the lost confidence amidst the investors.

As the Covid cases continue to mount in the United States and the major European economies, investors are likely to exercise caution in the upcoming weeks, as there could be some shocks and surprises in the Q4 earnings. It remains crucial to see whether all the components of the Dow Industrials manage to exceed or meet the investors’ expectations and the respective projections provided by themselves during the Q3 earnings season.

The Dow Jones Industrial Average advanced 269.96 points, or 0.74% to 36,855.02, the broader share average S&P 500 rose 17.47 points, or 0.36% to 4,814.03, while the technology heavy barometer Nasdaq Composite suddenly declined 62.40 points, or 0.39% to 15,770.40, effectively erasing the gains on day one of 2022.

US Market News: Shares of Caterpillar, JPMorgan Chase, Goldman Sachs, American Express, Visa, Coca-Cola, Boeing, IBM, Travelers Companies, Chevron, and Dow emerged as the leading gainers among the 30 heavyweights of Dow Industrials, with the stocks zooming 1-3%. On the other hand, the stocks of Salesforce.com, Cisco Systems, and UnitedHealth Group were the top losers on Tuesday.

Shares of Apple traded little changed in negative territory on Tuesday after the iPhone maker became the first listed corporation to have a market capitalisation of $3 trillion. The stock of Apple traded at $181.96, down 0.02% from the previous close of $182.01.

Among the constituents of Nasdaq Composite, shares of DocuSign, Marriott International, Paccar, Cognizant Technology, Trip.com Group, Twenty-First Century Fox, Kraft Heinz, CSX, Xcel Energy, Fiserv, Booking Holdings, Skywork Solutions, CDW, and Monster Beverage were the major gainers, with the stocks rising 1-4%. Shares of Atlassian Corporation, Peloton Interactive, JD.com, Idexx Laboratories, Moderna, Pinduoduo, Workday, NetEase, CrowdStrike Holdings and MercadoLibre plunged 3-8%.

UK Markets: In an eventful session on the first trading day of 2022, UK shares made an energetic start to the new year with the domestic benchmark index FTSE 100 reclaiming the psychological level of 7,500 for the first time in the last 23 months.

The leading share average in the City of London surged more than 120 points, largely propelled by the heavyweight shares of Unilever, Diageo, HSBC Holdings, Royal Dutch Shell, BP, British American Tobacco, Glencore, BHP Group, Anglo American, National Grid, London Stock Exchange, Prudential and Lloyds Banking Group.

Among the top 20 corporations on the London Stock Exchange by market capitalisation, shares of AstraZeneca emerged as the biggest losers as the stock dived more than 2%, effectively offsetting a major portion of positive points provided by the aforementioned shares. Alongwith the market capitalisation leader, shares of Relx and GlaxoSmithKline were the other decliners among the top 20 components.

Shares of International Consolidated Airlines led the charge of FTSE 100 with the stock rallying over 12%, while the shares of Dechra Pharmaceuticals and Ocado Group lost 6-8%.

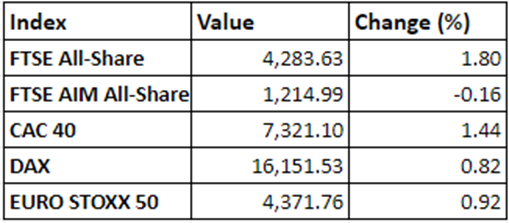

The 101-stock heavy FTSE 100 soared 123.07 points, or 1.67% to 7,507.61, after hitting a 23-month high of 7,516.10, while the mid-cap indicator FTSE 250 added 464.82 points, or 1.98% to 23,945.63, after briefly hitting an intraday peak of over 24,000.

FTSE 100 (04 January)

Source: EODHD/Others

Market Snapshot

Top 3 volume leaders:, Vodafone Group, Lloyds Banking Group, and International Consolidated Airlines

Top 3 sectoral indices: Travel, Personal Goods, and Fossil Fuels

Bottom 3 sectoral indices: Precious Metals, Medicine and Biotech and Software and Computing

Crude oil prices: Brent crude up 1.56% at $80.19/barrel; US WTI crude up 1.58% at $77.28/barrel

Gold prices: An ounce of gold traded at $1,814.45, up 0.80%

Exchange rate: GBP vs USD - 1.3547, up 0.56% | GBP vs EUR - 1.1974, up 0.43%

Bond yields: US 10-Year Treasury yield - 1.659% | UK 10-Year Government Bond yield - 1.0630%

Markets @ 15:31 GMT

© 2022 Kalkine Media®