US Markets: Wall Street started in the negative territory on Wednesday, 17 November, with the three major indices losing their respective psychological marks as market participants remain anxious about the inflationary hurdles. Marginal drops in the indices can be due to profit-booking sessions as American equities have seen a vibrant rise following the upbeat corporate earnings for the July-September quarter with a large section of heavyweight corporations exceeding the street estimates.

The traders have seemingly factored in the recent spikes of Covid cases in European and some of the Asian countries. The persistently higher cost of raw materials has been invariably hurting the profitability of manufacturers, as well as the enterprises involved in the construction businesses.

Meanwhile, the housing starts in the United States slid to an annualised rate of 1.52 million, witnessing a sequential drop of 0.7% in the month of October 2021, the US Census Bureau data showed. The housing starts were well below the street expectations as the figure fell to the lowest in the last six months. This has been the second consecutive drop in the housing starts as faltering supply chain and logistics systems, higher costs of building & construction materials and dearth of skilled workforce continues to hurt the operations.

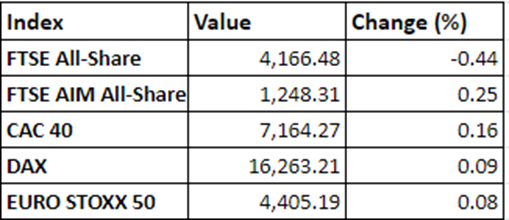

Global Markets traded lower on Wednesday

The high input costs, alongside the short-staffed situation makes it extremely difficult for many businesses to realise earnings close to the pre-Covid levels, at a time when most of the commercial setups are allowed to resume their operations at the maximum possible capacities. Among the major blue-chip companies, Cisco Systems and Nvidia are slated to announce the quarterly report card after the market hours.

The NYSE-controlled Dow Jones Industrial Average lost 179.73 points, or 0.50% to 35,962.49, the tech heavy Nasdaq Composite shed 18.39 points, or 0.12% to 15,955.46, while the broader share market index declined 9.97 points, or 0.21% to 4,690.93, as market-wide sell-off weighed on the leading stock indices.

US Market News: Shares of Visa fell more than 5% after Amazon declined to take UK-issued Visa cards as a mode of payment on its platform. Amazon has cited the “high cost of payments” as the primary reason for discontinuation of UK-issued Visa cards on Amazon.co.uk. The decision will come into effect from 19 January, 2022.

The stock of Visa emerged as the biggest loser amid the 30 components of Dow Industrials on Wednesday. Other major shares that fell considerably include Goldman Sachs, Travelers Companies, American Express, Walgreens Boots Alliance, Caterpillar, Chevron, 3M, Coca Cola and JPMorgan Chase.

Shares of Apple saw a rise of over 1%, effectively trying to counterbalance the negative points provided by the aforementioned blue-chips shares. The marginal uptick in the stocks of Home Depot, Salesforce.com, Amgen, UnitedHealth Group and Boeing failed to offset the losses.

Shares of Tesla made a sharp comeback with the stock appreciating more than 5%, leading the 100-constituent pack of Nasdaq Composite. The upswing was thoroughly supplemented by the rise in shares of Ross Stores, Moderna, CrowdStrike Holdings, NetEase, Apple, Charter Communications, Match Group and Amazon.

The proportion of decliners outnumbered the advancers on Nasdaq with the shares of Baidu, PayPal, Peloton Interactive, JD.com, Activision Blizzard, MercadoLibre, Pinduoduo, eBay, Fiserv, Lululemon Athletica, Intuit, T Mobile US, Biogen, Walgreens Boots Alliance, Microchip Technology, Micron Technology and Copart crashing 1-5% in the session so far.

UK Markets: London equities were hammered by the fears of inflationary hurdles with the UK CPI based rate of inflation soaring to 4.2% in the month of October, exceeding further above the Bank of England’s target as corporations increasingly passed on the burden of higher input prices to the consumers. This has been the highest rate of inflation in the United Kingdom since December of 2011, nearly a decade.

Following the development, the benchmark index FTSE 100 dived deeper into the red, slipping below the psychological level of 7,300 in the wee hours of opening trade on Wednesday. The higher costs of housing and utilities have largely driven the rate of inflation in October of 2021 with the prices of electricity, gas and liquid fuels witnessing a major surge on the back of mounting energy prices globally. On a month on month basis, the inflation rate jumped to 1.1% from 0.3% in September.

The key barometer dropped 33.96 points, or 0.46% to 7,293.01, whereas the mid-cap UK average fell 85.05 points, or 0.36% to 23,454.66, after briefly touching the positive territory during the day.

FTSE 100 (1-year performance)

Source: EODHD/Others

Market Snapshot

Top 3 volume leaders: Lloyds Banking Group, Vodafone Group and Barclays

Top 3 sectoral indices: Automotive, Precious Metals and Software and Computing

Bottom 3 sectoral indices: Electricity Generation and Distribution, Finance Services and Industrial Engineering

Crude oil prices: Brent crude down 1.37% at $81.30/barrel; US WTI crude down 1.69% at $78.39/barrel

Gold prices: An ounce of gold traded at $1,867.85, up 0.74%

Exchange rate: GBP vs USD - 1.3464, up 0.28% | GBP vs EUR - 1.1911, up 0.45%

Bond yields: US 10-Year Treasury yield - 1.625% | UK 10-Year Government Bond yield - 0.9710%

Markets @ 16:25 GMT