Summary

- There are growing speculations on the upcoming cut in cash rate in November.

- The interest rates have been on the decline since 2019, which has adversely impacted the pensioners.

- Since most pensioners are self-funded, the COVID-19 financial crisis is two-fold for them as they fight health risks too.

- The financial sector has also been hit adversely, along with pensioners and investors.

- It is expected that the economy might benefit from low cash rates, but at the expense of the elderly.

Speculations are rife about further cash rate cuts by the RBA. The anticipation is a sigh of relief for mortgage loan borrowers and consumers, while troublesome for financial system and retirees. People with investments and deposits are struggling as their interest incomes fall.

Cash rate cuts have been received well by the demographic holding liabilities; however, banks have faced the brunt of this interest rate reduction this year. The primary objective of the cash rate cut has been to provide stimulus to the economy amid the Global Virus crisis. The pandemic-induced restrictions have contracted the economy significantly.

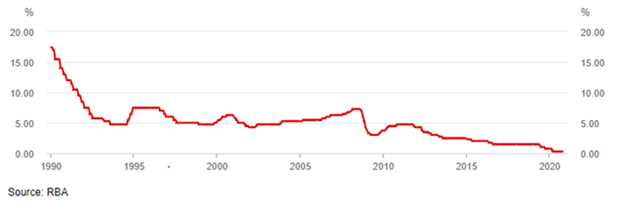

While the Government has provided fiscal relief along with healthcare aid packages, interest rate cuts have been on the RBA’s agenda for long. The fallback in cash rate started in mid-2019 and the interest rates have been on the decline since then.

The rate cut speculations come after Phillip Lowe’s speech at Citi’s 12th Annual Australia and New Zealand Investment Conference in Sydney. In his speech, Governor Lowe announced that there is no possibility of cash rates bouncing back any time soon. Cash rates cannot be increased till the target inflation rate of 2-3% is not achieved.

IN CASE YOU MISSED: Key Takeaways from Phillip Lowe’s stance on rate cuts and stimulus

Impact on the Elderly Demographic

Pensioners and retirees depend on their interest income to survive. Most of the elderly demographic have their funds and deposits secured with the banks.

Cash rate does not affect customers directly, as it is the rate at which banks borrow from each other (overnight loans) to maintain daily settlements. As cash rate falls, banks face the risk of reduced interest income from other banks on these “overnight borrowings”.

This risk is passed onto the customers in the form of reduced interest rates offered on their deposits. Consumers with investments as well as with deposits with the banks are the ones to be hit severely.

Fixed-interest investments, namely, bank accounts and term deposits are a huge part of retirement savings. During unprecedented times like right now, people are struggling with job losses along with the risk of catching the virus. It is important to have a fixed source of income to fall back on during these uncertain times.

Most pensioners are self-funded and depend on their interest incomes to meet their daily requirements. Adding to that, the health risks for the elderly are much greater than those faced by the younger generations. With their assured stream of income falling significantly, the elderly might have to rely on other sources to survive.

ALSO READ: RBA Cash Rate Decision Under the Spotlight

What Alternatives Do the Pensioners Have?

In times like these pensioners would see no other alternatives than to use their deposits, if need be. Depending on only one fixed source of income would not be sufficient. The government can help the pensioners by cutting the deeming rates and introducing favorable policies that help pensioners in these difficult times.

Upper deeming rate determines how much pensioners earn from their savings investments. It is inversely proportional to the amount of pension received. Thus, cutting down the deeming rate could benefit pensioners when they are facing the brunt of low interest rates.

GOOD READ: Everything you need to know about the self-managed superannuation fund

Current Economic Scenario

Unemployment rates are currently at an all-time high in Australia. As unemployment increases, all measures adopted as a remedy to combat contracted consumption might go in vain as it is expected that people would again start to save.

The pandemic has made people more risk averse. Their appetite for handling difficult times has decreased due to a long period of uncertainty. Thus, most people would avoid being at the riskier side of things and would save more to protect themselves from any impending downturn.

Economic recession fuelled by serious job losses and salary cuts comes attached with a risk of an increase in NPAs or Non-Performing Assets. As people are unable to repay loans and they delay on their mortgage payments, there is a fear that these would become non-performing. Thus, an expected increase in NPAs is eminent.

Another issue of concern is providing loans to new borrowers. Banks would most likely avoid lending to new and risky borrowers.

ALSO READ: RBA says Australia might already be out of recession

Expected Positive Outcomes

It is expected that cash rates would not rise till the inflation rate is brought down between the target range of 2-3%. The RBA understands that current policy measures might influence the financial stability in the long run. As of now, the focus is on private sector job creation as well as easing loan payments.

The positive implications of the monetary policy easing are still unclear. The effectiveness of the policy might be hampered by the long-term risks associated with it, which may start to show in some time.

Thus, the financial sector, as well as pensioners, might end up cushioning out the economic damages faced by the other sectors, while struggling for survival in present times.