Highlights

- The big four banks have lowered their variable mortgage rates ahead of the central bank’s possible rate hike decision.

- Commonwealth Bank of Australia (ASX:CBA) is the latest big four bank to decrease its lowest variable rate for owner-occupiers.

- Opting for lower interest rates now could help cushion borrowers from steep interest payment hikes expected later this year.

As the Australian economy continues to walk on its recovery path, the country has begun to wind back its pandemic-era stimulus. While the Reserve Bank of Australia (RBA) has not yet raised its interest rates like its peers, the big four banks have begun to factor in potential cash rate hikes.

Ahead of the monumental decision by the RBA to increase interest rates, the big four banks have decided to decrease their variable mortgage rates. In fact, competition in the variable home loan space is heating up, with banks opting for lower variable rates and high fixed rates.

A possible rise in the cash rate would most likely prompt commercial banks to raise the interest rates they offer to their customers. When the cash rate increases, it makes borrowing more expensive for commercial banks which intend to maintain sound financial backing.

For the uninitiated, the cash rate is the rate on ‘overnight’ funds at which banks lend to one another. However, going beyond the bookish definition, the cash rate holds a much deeper purpose in an economy and is a benchmark against which many other interest rates are set.

Following an interest rate hike by the RBA, commercial banks are most likely to follow suit and increase their interest rates on all types of loans. However, till the time rate hikes are not implemented, these banks have taken a seemingly polarising approach by decreasing variable rates on mortgages.

ALSO READ: Five things to expect from pre-election Australia Budget

The big four banks and their interest rates

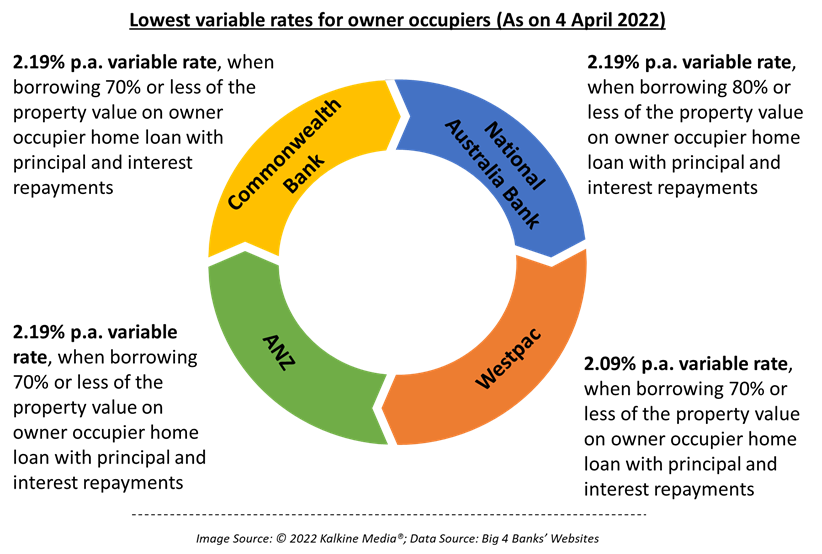

All big four banks have taken a swift approach to lower variable interest rates, one after the other. Interestingly, these banks have introduced steep hikes in their fixed-rate mortgages, in sharp contrast to the decline in variable rates. Consequently, variable mortgage rates offered by these banks have come close to 2%, with Westpac offering the lowest variable rate.

These rates have been conditioned ahead of the possible interest rate hikes by the central bank. As soon as the Reserve Bank implements an interest rate hike, the commercial banks could soon turn the tables and increase these variable rates.

The latest decline in the lowest variable rates for owner-occupiers came from the Commonwealth Bank of Australia (ASX:CBA) on 25 March 2022. However, the bank took a different route for the fixed-rate mortgages. The 1-year fixed mortgage rate was increased by 0.20% to 2.99%. While the 2-, 3-, 4- and 5-year fixed mortgage rates were increased up to 0.30%, with the 5-year fixed rate reaching the highest at 4.29%.

INTERESTING READ: When was the last housing market crash in Australia?

Why have big four banks reduced variable rates?

In a seemingly unanimous turn of events, the big four banks have reduced the variable rates. Evidently, these banks appear to be competing for a sizeable market share as cash rate rises are underway. Offering lower rates now would be beneficial to consumers who wish to take out a housing loan in the near term.

These lower rates are mostly applicable to only those borrowers who can put down a deposit of 30% or more. This means that banks are currently in a bid to lock in the lower-risk borrowers for the long haul. In September last year, these banks were offering 3-year fixed rates between 1.98% and 2.19% on home loans. However, given the latest anticipation surrounding cash rates, these fixed rates have shot up to 3.79%.

The surging bond rates have somehow prompted banks to charge high interest on fixed-rate mortgages. Over the last few months, the 3-year and 5-year bond rates have surged on expectations that the RBA would be forced to increase interest rates as inflationary pressures build up. This, in turn, suggests that variable rates might also be subject to some sharp upticks in time.

Did Covid Change the Australian Property Market for Good?

Owner-occupiers can utilise the recent step taken by the big four banks and lock in a lower variable rate before such rates increase to unpalatable levels. This would provide a cushioning effect against the drastic surge in interest payments that could arise when the variable rates are eventually increased.

Bottom line

Mortgage lending has dramatically surged in Australia, casting fears of a bubble burst in the housing sector. Previous experiences have shown that higher lending contributes to inflated housing prices. However, a slowdown is beginning to emerge in the property market, while fears are rife that a sudden deflation in prices could bring turmoil in financial markets. Till then, consumers can prevent themselves from high interest payments by opting for lower rates now to avoid missing the boat.

INTERESTING READ: Disinformation Register: Debunking mistruths about 2022 Australian federal election