Summary

- A Roth IRA is an individual retirement account to which you can contribute after-tax dollars and that can provide you with tax-free income.

- The 2021 contribution limit is up to US $6,000 or US $7,000 if 50 or older.

A Roth IRA is an individual retirement account to which you can contribute after-tax dollars and that can provide you with tax-free income and growth in retirement, while there are no current-year tax benefits. You can also withdraw the amount tax- and penalty-free after you turn 59 and half and provide additional flexibility for withdrawals once the account has been open for five years, contribution can be withdrawn at any time, for any reason.

In accordance with the Article 17 of the US and UK tax treaty, if a pension/retirement is tax-free in one jurisdiction, then the other contraction state (UK) will not tax the income, as it is tax-free in the other contracting state (US), which means no tax will be paid to the HMRC. However, the default rule is that it’s taxable in the UK unless and until you affirmatively elect to claim the benefits of the treaty.

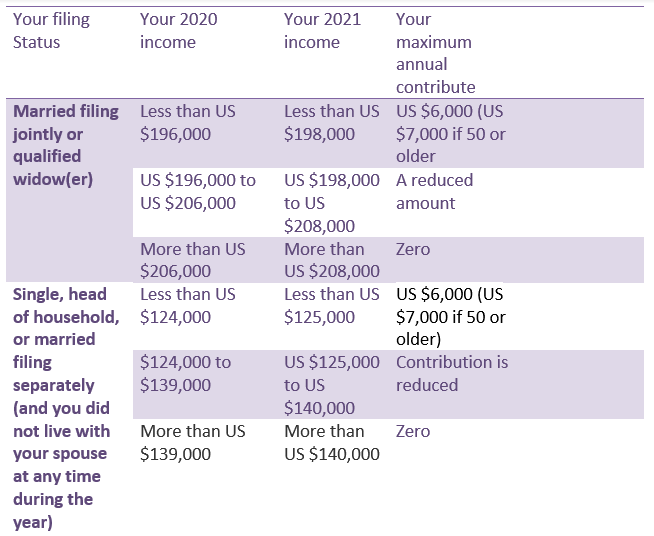

The 2021 contribution limit is up to US $6,000 ($7,000 if 50 or older) for modified adjusted gross incomes below US $14,000 (single filers) or US $208,000 (married filing jointly).

In 2020, the contribution limit was up to US $6,000 (US $7,000 if 50 or above age) for modified adjusted gross income below US $139,000 (single filers) or US $206,000 (married filing jointly).

In a nutshell

The Roth IRA is a tax-advantaged account that holds investment to provide you with tax-free growth and income in retirement. A person can contribute to a Roth IRA from the earned income after the payment of regular income tax with no upfront tax break with a Roth IRA. However, the tax benefits come later, as person pay no income tax on qualified withdrawals.

A person can open a Roth IRA account at a bank or a credit union or online brokerage account. If the Roth IRA account is opened through online broker, you can also use your IRA funds to buy stocks, mutual funds, exchange traded funds (ETF) and bonds. On the other hand, if you open Roth IRA account through credit union or bank, you can use IRA funds in a saving account or a certificate of deposit (CD).

The contributor can withdraw its contribution in Roth IRA account for any reason and any time. However, you have to pay income taxes and penalties if the withdraw is made before 5 years since the first contribution and made before the age of 59 and half.

Contributor doesn’t have to withdraw their money if they don’t want to or have no requirement, as there are no required minimum distributions.

Who all can avail

You can only contribute your earned income that has been received from employment or self-employment in order to contribute to a Roth IRA in any given year. This income is called as Taxable compensation. You can’t contribute any passive or investment income such as dividend, interest or capital gains.

Further, you must be under the income threshold, which is up to US $6,000 (US $7,000 if 50 or older) for modified adjusted gross incomes below US $14,000 (single filers) or US $208,000 (married filing jointly) in the year 2021.

Also, you need to have a taxable compensation of US $6,000, which is US $7,000 if your age is 50 or more, whichever is less.

ROTH IRA INCOME LIMIT FOR 2020 AND 2021

Some benefits

- Tax savings: You can contribute money in Roth IRA, on which you’ll pay income taxes on this year than in the future when your tax rate is higher. If you are paying less tax at present, you may opt to pay more now, so that you get tax-free retirement withdrawals.

- Tax-free distribution: Without paying income taxes, you can withdraw your contribution including earnings from a Roth IRA. But only when you are above 59 years and have held the account for at least five years.

- Flexible timing: You can choose when and how much you want to contribute to a Roth IRA.

- Easy Withdrawals: You can withdraw your contribution any time and for any reasons without any taxes or penalty. However, you may have to pay taxes and penalties if you withdraw investment earnings.

- No age limit to open: You can open a Roth IRA account without any age restrictions as long as you have earned income.

- Double dipping: You can contribute to a Roth IRA in addition to a 401(k).

- No required minimum distributions: The Roth IRA account is not subjected to the required minimum distributions required from a traditional IRA or 401(K) starting at the age of 72.

- Extra time to contribute- you have until the tax deadline to contribute for the previous calendar year.

Some drawbacks

As nothing is perfect, Roth IRA has many disadvantages along with its advantages.

- You can’t take loan from IRA the way you can with many 401(k), which means you can withdraw penalty, interest or taxes.

- Withdrawal of your investment earning in Roth IRA before the age of 59 and half can force you to pay penalty unless you meet one of the mentioned exceptions.

Withdrawing before time

Some of the exceptions to avoid the 10% penalty on the early withdrawals:

- To pay qualified medical expenses, higher education expenses, and health insurance while you’re unemployed.

- Physical or mental disability.

- Paying an IRS levy.

- Qualified reservist distributions.

- You’re purchasing your first home.

- You withdraw the money as a beneficiary.

- You are a parent.

- Taking substantially equal periodic payments.

The lock period

As we know now that the Roth IRA contributions and earnings can be withdrawn any time and for any reasons, but you need to wait for completing 5 years of your first contributions and you need to be more than 59 and half years or above to do that.

- If you withdraw you Roth IRA contributions before the completion of five years, you have to pay income taxes and 10% penalty on the withdrawals

- If you withdraw money rolled over from a traditional IRA or 401 (K) into a Roth IRA before the completion of 5 years, you may have to pay income taxes and 10% penalty.

- You may have to pay income tax if you withdraw earnings, when you inherit a Roth IRA from someone who’s first Roth contribution was less than five-year old.

This vs that

If you are covered under employer retirement plan, traditional IRA can give you an immediate tax break as it reduces your taxable income. If you are covered under the employer-sponsored retirement plan and your income is above the threshold you should consider Roth IRA as it provides tax-free income while retirement.

As the young person faces higher income tax rates as they move along in their careers, the Roth IRA is considered as a smart saving tool as it offers tax-free income in retirement.