Highlights:

- On Monday, Westpac Banking Corporation (ASX:WBC) released its 1H FY23 results ended 31 March.

- In the reported period, WBC’s net profit grew 22% to AU$4 billion from AU$3 billion in pcp.

- WBC’s board declared a 100% franked distribution of 70 cps for 1H FY23, reflecting an increase of 15% on pcp.

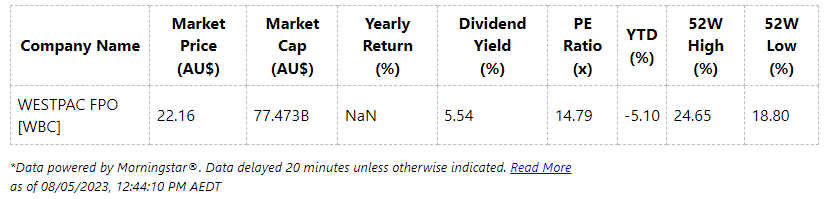

Australia’s first bank with an array of innovative financial packages, Westpac Banking Corporation (ASX: WBC), grew by 3.091% and was trading at AU$22.010 on Monday, 8 May 2023 at 11:40 am AEST after the ASX bank stock published its interim report ended 31 March this year.

Let’s get apprised of the ASX200 banking stock- WBC’s 1H FY23 results.

On Monday, the bank, in its 1H FY23 results, noted revenue (from ordinary activities) rose by 8% to AU$11,003 million from AU$10,230 million in pcp. For the reported period, WBC’s net profit grew 22% to AU$4 billion from AU$3 billion in pcp stemming from greater net interest margin (NIM) due to rising interest rates. The bank’s performance steered a material improvement in ROE and ROTE, increasing by 205 bps to 11.3% and 229 bps to 12.8%, respectively.

WBC’s NIM in the interim period expanded by 5 bps to 1.96% from pcp. Net interest income was up 10% to AU$9,113 million from AU$8,288 million in pcp due to an elevated net interest margin, along with a 7% rise in average interest-earning assets. Core NIM got a boost of 20 bps to 1.90% from wider deposit spreads and increased return on capital balances.

The 1H FY23 operating expenses were down 7% to AU$4,988 million from AU$5,373 million in pcp partly because of sold businesses. Notable items and the effect of businesses sold were AU$5,006 million, decreasing by 1%, demonstrating benefits of their simpler organisation and reduced use of third-party service providers.

In the half-year period, the CET1 capital ratio of 12.3% was more than their target range of 11% - 11.5%, delivering AU$3.6 billion of capital above the top end of the target range.

For the half-year period, the bank’s board declared a 100% franked distribution of 70 cps, reflecting an increase of 15% on pcp, representing a payout ratio of 61%. Basic EPS was up 26% to 114.2 cents. The distribution is payable on 27 June 2023 and has an ex-dividend date of 11 May. The record date of distribution is 12 May this year.

On the outlook front, WBC said that Australia’s economy remains resilient with lesser unemployment and rising population growth, it is anticipated to slow down across the rest of this year. The bank said that the credit rise (housing and business) will ease. They also mentioned that intense mortgage competition is likely to negatively affect industry and WBC’s margins in 2H FY23.

The bank is entering this environment from a position of strength. They have set the balance sheet for a tougher outlook. They continue to manage the bank conservatively, with the flexibility to aid growth and handle further difficult situations.