A milk distributer beats high growth technology stocks hands down. AUD 100k turned to AUD 3.1 million in 5 years. The company increased revenue by 11.2x (a CAGR of 62.1%) and gross profit by 17.8x (a CAGR of 77.87%) in five years. More importantly, during the same time period the company had deployed a meagre capital in fixed assets to deliver this stupendous performance. The company continues to grow and gain market share across geographies that it is operating in, and in the due course it has been increasing stake in its key supplier in a prudent manner.

Summary

- Since listing on ASX in March 2015, A2M is up ~32x.

- A2M has a capex light business model with strong profitability.

- The business continues to grow in its key markets underpinned by strategic partnerships.

- Growing across regions:

- Earlier this year, it marked entry to Canadian market.

- Late last year, infant nutrition products were launched in South Korea & Hong Kong.

A2M has been one of the best growth stories on ASX over the past years. The company was established in 2000 to better understand the scientific benefits of A2 protein type. Australia & New Zealand are the primary markets of the business. It also sells in China and the United States of America. Most recently, the company has also entered Canadian market.

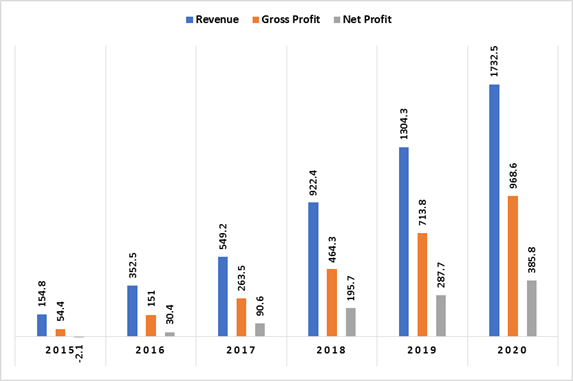

Topline-Bottomline (NZD Millions)

Source: Thomson Reuters/EODHD/Others, Kalkine

Over the five years to FY20, the company has grown its revenue to $1,732.5 million from $154.8 million in FY15. During the same period, gross profit increased to $968.6 million from $54.4 million and net profit reached $287.7 million from $0 million (loss).

In the same period, A2M’s revenue CAGR is 62.1% and gross profit CAGR is 77.87%. More importantly, the business has delivered this solid CAGR in revenues with ~$13.8 million (FY15-FY20) fixed assets investment/capital expenditure on fixed assets.

It is because A2M sits on the gold mine, Synlait Milk (ASX:SM1). As a strategic partner, SM1 does all heavy investments for the production of major goods sold by A2M, which is why A2M’s balance sheet remains clean with nil debt.

Minimum fixed assets mean a lower depreciation, consequently lower replacement requirement or fresh capital expenditure – making A2M a CapEx light business model.

A2 Milk Company is like a marketing business, which primarily focuses on building client relationships, entering new markets, improve product reach, develop new products, increase brand awareness etc.

Thanks to its asset light business model, the company barely incurs capital expenditure, and this has a huge positive impact on the return profile.

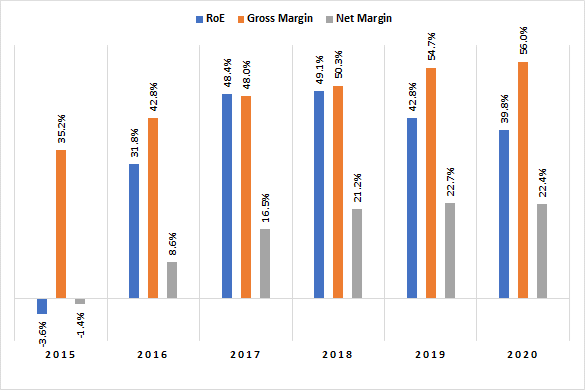

In a matter of 5 years, the company has been able to add close to 2,076 bps to its gross margin from levels of 35.20% to 55.96%%, this clearly shows that the company has tremendous pricing power and efficiency.

The company has seen growth in all its key return ratios, however we notice that the company has seen a drop in ROE in the past, this has come on the back of heavy marketing expenditure (in FY20 the company invested heavily into marketing and distribution to boost China and the US business), which going by the company’s track record the market would be expecting to see it add value in the coming years.

Return Ratios & Margins

Source: Thomson Reuters/EODHD/Others, Kalkine

In April, the company reported that it has been experiencing significant demand, leading to strong revenue growth across regions. Infant nutrition sales in China and Australian were performing strongly.

As a result, its third quarter revenue exceeded management expectations. This result was delivered primarily due to change in consumer behaviour due to COVID-19, including an increase in stocking levels by sales channels.

A lower NZD against USD also provided favourable impact to the revenue as China revenue is transacted in USD. Due to travel restrictions and delays in new recruitment, there was a lower level of overhead cost.

Increased stake in Synlait Milk Limited (ASX:SM1) – A2M’s Manufacturing partner

A mark of a good investment decision is gauged by how an investment decision is made during market volatility. The company made a prudent investment decision in March, by capitalising on the opportunity provided by market volatility and increased its stake in Synlait Milk to 19.9% from 17.4%. It acquired shares through on market purchases at a price of $4.95. This investment further cements the relationship the company has with its major supply chain partner also securing its interests if need arises such as corporate takeover of SM1.

A2M’s CEO, Mr Geoffrey Babidge stated that A2M was presented with an opportunity to increase strategic stake in Synlait Milk after a significant decline in share price.

Entry into Canadian Market

In March, the company announced that an exclusive licensing agreement was executed with Agrifoods Cooperative. Under the agreement, Agrifoods would undertake production, distribution, sales and marketing activities for a2 MilkTM in Canada.

A2M would provide Agrifoods with access to intellectual property, proprietary systems, marketing assets and expertise. It would also work with Canadian farmers to source the milk supply locally. A2M is funding the venture primarily and would establish distribution network across Canada.

An impressive run of Topline amid Pandemic

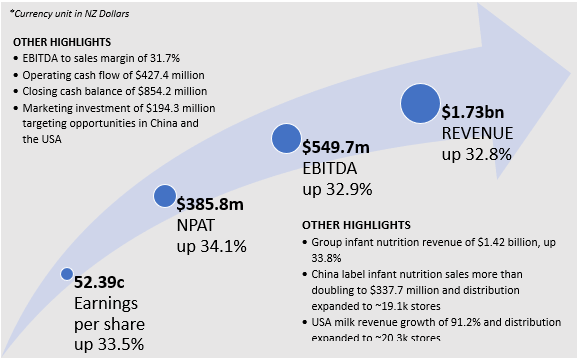

The company showed an impressive run in the FY20 with increase in revenues demonstrating growth experienced across the core markets and product categories. The EBITDA margin of 31.7% was in line with the guidance of 31-32%. The revenue of $1.73 billion was also in line with management expectation.

Source: Company’s Report

Gross Margin increased to 56.0% YOY from 54.8% backed by better price yield and the positive effects of currency movements partially offset by increased COGS related to infant nutrition

The Company experienced increased growth in China and USA backed by investment made in these geographic regions to boost businesses. In FY20, A2M incurred higher distribution costs, invested in building human resource capacity and made marketing investment of $194.3 million to boost business in China and the USA.

The Company also increased spending on Admin & other areas to gain consumer insights and assist business expansion by improving internal capability.

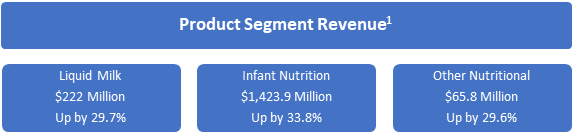

1 Excludes UK discontinued operations.

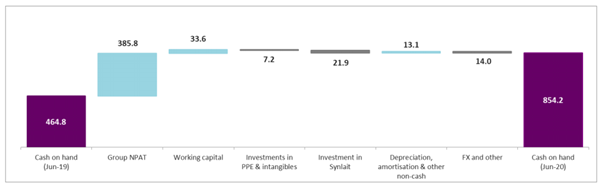

Cash Balance

a2 Milk Company finished the FY20 period with a cash balance of $854.2 million. the increase in the cash on hand was led by strong Group earnings and improved working capital of $33.6 million because of better timing of supplier payments. The company intends to rely on merger and acquisition opportunities to fuel more growth within its business by building up on manufacturing.

Kalkine Image (Source: ASX Update)

The Mataura Valley Milk Acquisition

The A2 Milk Company is set to deploy $270 million to acquire a 75.1% interest in Mataura Valley Milk (MVM), New Zealand based dairy nutrition business. The deal upon completion will allow A2 milk to utilize the Mataura’s facility to set up a blending and canning capacity in the future.

According to the announcement, MVM has agreed to allow A2M to conduct a confirmatory due diligence within a definite period and discuss definitive transaction documentation. The decision of exclusivity arrangement is supported by China Animal Husbandry Group (CAHG), MVM’s current majority shareholder who will retain a 24.9% interest in MVM upon completion of acquisition by a2 Milk.

a2 milk shares an old relation with CAHG which is a wholly owned subsidiary of China National Agriculture Development Group, the parent company of strategic partner of a2 Milk in China.

According to Chief Executive Officer, Geoff Babidge, the potential acquisition is in line with the company’s strategic goals. According to Mr. Babidge, the company earlier had shown intention to work on it manufacturing capacity and capability because of its increasing scale of infant nutrition business. The investment in MMV’s recently commissioned facility aligns with the strategic objective of the company and a part of building upon its current strategic relationships with Synlait Milk and Fonterra Co-operative Group, which remain in place.

Mr. Babidge also intends to invest additionally to develop blending and canning capacity at Mataura’s facility to make it a fully integrated manufacturing plant for infant nutrition.

(All currencies in NZD unless or otherwise stated)