Global sell-off continues to pull the Australian markets to lower levels consistent with the global markets in the wake of increasing coronavirus concerns that has hit across the globe and may dampen the global economic forecasts for the near-term.

As Italy braced for a sharp jump in the number of cases, the market mood was severely hit during the Monday trading session in Europe as well as in the western markets, including the USA and Canada.

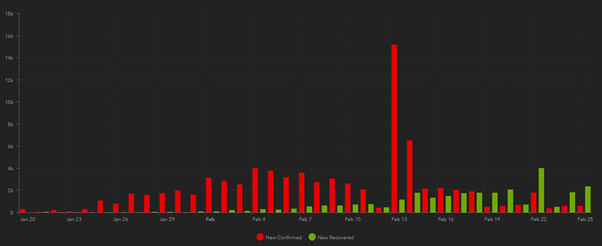

At around 1:53 PM AEDT, the coronavirus tracker by John Hopkins CSSE shows that 80,146 cases have been confirmed, of which 77,658 cases are in China. South Korea is witnessing confirmed cases at 893 with Italy having 229 cases.

Figure: New confirmed & new recovered cases

Source: John Hopkins CSSE

Around 27.5k recoveries are reported. On the brighter side, the data shows that the recovered cases are trending higher than confirmed cases since 19 February. WHO believes that the coronavirus crisis has not reached a pandemic level, however, it has the propensity to create a pandemic.

Economists are predicting that the coronavirus hit is likely to lower the Q1 GDP numbers for the Chinese economy. In the meantime, they also expect a rebound in the economic activity in the following periods.

In an extreme scenario where the virus becomes a global pandemic, Oxford Economics forecast that the global GDP growth for the first half of 2020 is likely to hover around zero, with an estimated growth of 1.3 per cent for the full-year.

Flight to safe haven assets

Safe haven assets, including government bonds, gold, precious metals, have risen in the value since yesterday as the investors derive implications of the stalled economic activity in the second largest economy of the world, and a spike in confirmed cases in Italy leaving the already-weak European region in potential jeopardy.

At the time of writing, Gold prices were trending around USD 1655, which touched USD 1680s overnight in the US. In the US, the yield on the 10-year US treasury bond fell steeply as the market opened on Monday.

US 10-year treasury yield ended at around 1.39 per cent, which is lower than prevailing CPI on all items at 2.5 per cent (y/y to January 2020). On Monday, the Dow Jones Industrial Average ended the session down by around 1,031 points at 27,960.8 points.

Caterpillar Inc led the losses in the 30-share index with 3.67 per cent or USD 5.04 lower at USD 132.17, Boeing Co ended down by 3.78 per cent at USD 317.90, Chevron Corp was down 3.94 per cent at USD 104.71.

Shares of Intel, Walt Disney and Microsoft, were down by 4.01 per cent, 4.29 per cent, and 4.31 per cent, respectively.

However, the losses were lowest in Verizon that ended the session down by 0.36 per cent, followed by Travelers Group, McDonald’s, and Merck, which shed 0.77 per cent, 1.09 per cent and 1.23 per cent, respectively.

Tesla Inc lost 7.46 per cent of its value or USD 67.21, closing at USD 833.93.

Australian markets ended in red for the second-day running

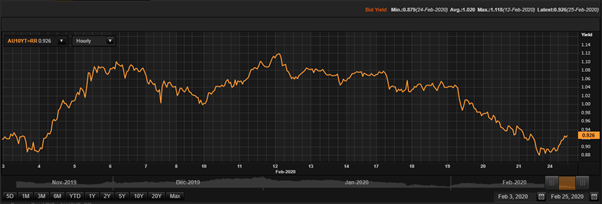

Australian 10-year bond has had a bumpy ride in the last two days, with hourly bid-yield touching 0.879 per cent on 24 February 2020. In February, the yields on the 10-year sovereign debt had trended above 1 per cent as well.

Today (i.e. 25 February 2020), the hourly yield on the 10-year Australian bond closed at 0.926 per cent. Interestingly, the traders/investors had helped to elevate the yield on the 10-year bond to higher levels as the closing time arrived.

Figure: AU 10-year bid yield (hourly)

Source: Thomson Reuters

Meanwhile, the domestic 10-year yield is likely to sustain above 1 per cent levels amid stable markets with lesser volatility, given the y/y CPI to December 2019 on all items was 1.8 per cent, and there is a strong fiscal position with a budget surplus.

Nonetheless, the stalled Chinese economy and possible weakness in its economic activity in 1Q, have additional downside risks to commodity-rich Australia, and its ever-growing trade partnerships with the red dragons, especially iron-ore and base metals.

Also, an elongated supply-chain disruption could prove to be an overall drag in the Australian given China is one of the largest trade partners of Australia Inc, with trade relationships ranging from beef to healthcare essentials.

In equity markets, the top 200 pack witnessed gains in Appen Limited (ASX:APX) up 6.5 per cent, PolyNovo Limited (ASX:PNV) up 4.86 per cent, New Hope Corporation (ASX:NHC) up 4.50 per cent, followed by oOh! Media Limited (ASX:OML) and Nearmap Ltd (ASX:NEA) with gains of 4.24 per cent and 3.31 per cent, respectively.

Meanwhile, the heaviest losses in the top 200 pack were noticed in St. Barbara (ASX:SBM) down 9.67 per cent, Saracen Mineral (ASX:SAR) down 7.33 per cent, Coca-Cola Amatil (ASX:CCL) down 6.9 per cent, Webjet Limited (ASX:WEB) down 6.54 per cent and Nufarm Limited (ASX:NUF) down 6.04 per cent.

Cash is the king

Investors with ample cash in pockets, like Warren Buffet, must be looking for some new good deals as the sell-off tide may have made their favourite stocks somewhat cheaper as against the recent past.

It would be quite premature to pump-in additional capital to risk-assets just because they provide a better margin of safety amid sell-off, as there is a possibility that the sell-off could be extended, owing to detrimental developments.

Investors are likely to hold off until there are some positive developments by the policymakers, including monetary as well as fiscal stimulus. But not limited to, positive news like increase in recoveries, drug development, and favourable containment efforts.